ARCH CAPITAL GROUP (ACGL)·Q4 2025 Earnings Summary

Arch Capital Delivers 38% EPS Growth But Stock Slides 4.5% on Premium Decline

February 9, 2026 · by Fintool AI Agent

Arch Capital Group reported Q4 2025 results that showcased exceptional underwriting performance, with GAAP EPS of $3.35 (up 38% YoY) and a combined ratio of 80.6% . Yet the stock dropped 4.5% as investors focused on the 4.5% decline in net premiums written, raising questions about growth sustainability in a potentially softening P&C market.

CEO Nicolas Papadopoulo struck an optimistic tone: "Our 2025 financial performance was outstanding, once again demonstrating the value of our diversified platform and our ability to effectively execute our cycle management strategy."

Did Arch Capital Beat Earnings?

Yes — Arch beat convincingly on earnings. The company delivered operating EPS of $2.98 vs. consensus expectations around $2.25, a 32% beat driven by:

- Lower catastrophe losses: 3.9% of combined ratio vs. 9.5% in Q4 2024

- Favorable reserve development: $118M release from prior year reserves

- Strong investment income: $434M pre-tax, up 7.2% YoY

The 80.6% combined ratio is exceptional for a diversified insurer/reinsurer and reflects Arch's disciplined underwriting across all three segments .

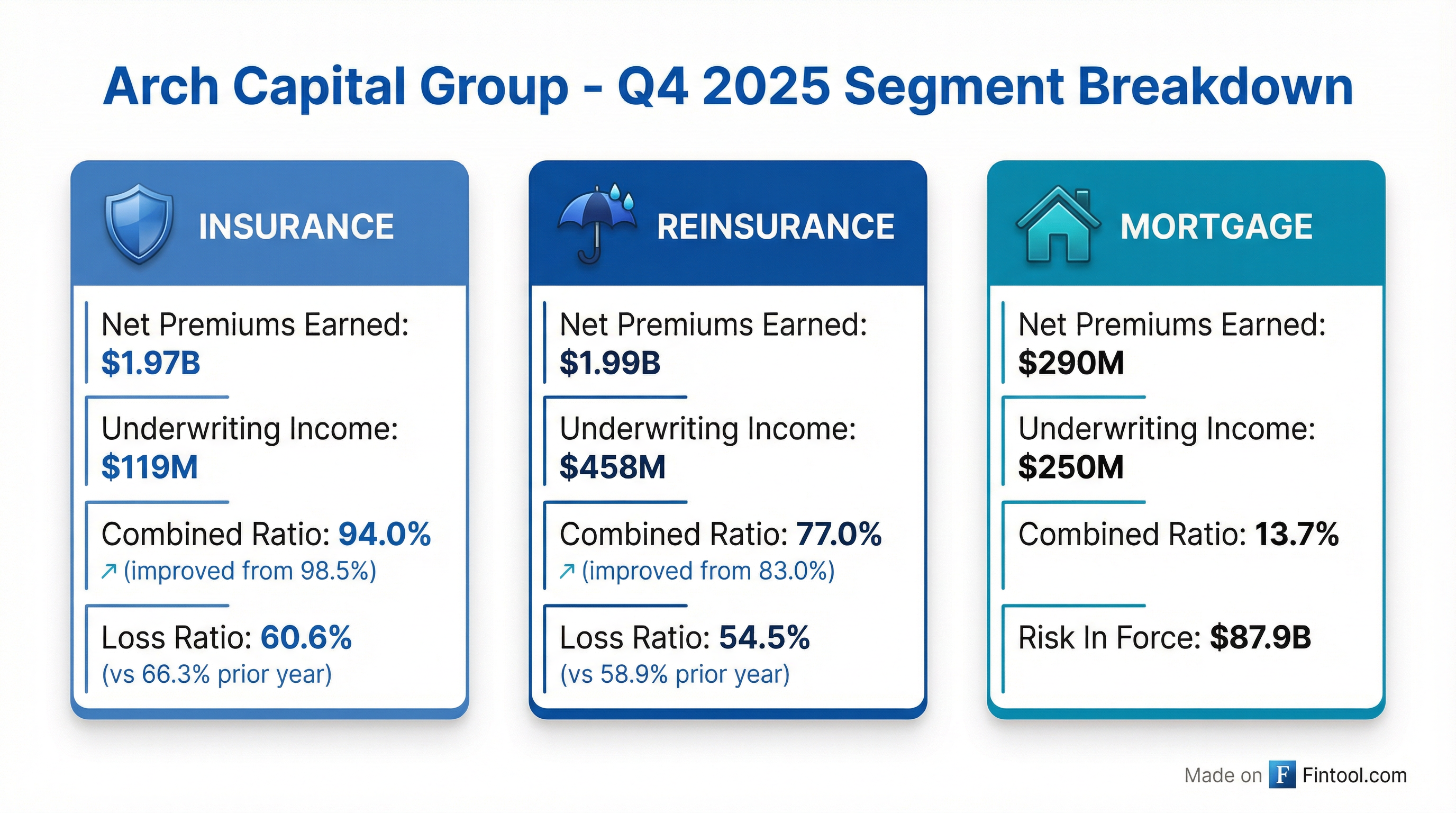

How Did Each Segment Perform?

All three segments showed YoY improvement in combined ratios, though growth varied:

Insurance Segment

The insurance segment showed the most dramatic turnaround, with combined ratio improving 450 bps to 94.0% :

The loss ratio improvement was driven by only 3.3% catastrophic activity vs. 8.3% in Q4 2024 . North America grew in long-tail casualty lines while scaling back property exposure .

Reinsurance Segment

Reinsurance delivered the strongest absolute performance with a 77.0% combined ratio :

Catastrophic activity was 5.0% vs. 12.2% in Q4 2024. The underwriting expense ratio also declined due to Bermuda tax credit benefits .

Mortgage Segment

The mortgage segment remains a cash cow with a 13.7% combined ratio :

The negative loss ratio (-0.8%) reflects continued favorable reserve development from better-than-expected cure rates . U.S. primary mortgage NIW was $14.3B with 79% FICO scores above 740 .

Why Did the Stock Drop Despite the Beat?

Net premiums written declined 4.5% YoY to $3.65B, the first decline in several quarters . This signals Arch is prioritizing profitability over growth in a competitive market:

The divergence between gross (up 1.1%) and net (down 4.5%) reflects increased ceded premiums, suggesting Arch is buying more reinsurance protection . This conservatism may be prudent given potential market softening but concerns growth-focused investors.

What Did Management Say About the Outlook?

CEO Papadopoulo expressed confidence entering 2026: "We enter 2026 with optimism in our ability to continue delivering superior results for our shareholders."

Key themes from the release:

-

Cycle management: Arch is emphasizing disciplined underwriting over premium growth, consistent with their historical playbook

-

Capital deployment: $798M in share repurchases during Q4, with $1.9B total for 2025 — management sees value in buying back stock

-

Bermuda tax impact: New corporate income tax increased effective tax rate to 14.5% from 6.6% in Q4 2024

-

Investment portfolio: Total investable assets reached $47.4B with average duration of 3.34 years and AA-/Aa3 average credit rating

What Changed From Last Quarter?

Operating EPS actually improved sequentially as catastrophe losses remained low (3.9% vs. 1.7% in Q3) . The slight increase in combined ratio reflects normal seasonal patterns and business mix changes.

Full Year 2025 Summary

For the full year, Arch delivered record profitability:

The 22.6% book value growth is particularly notable, driven by strong earnings, share repurchases, and a recovery in the fixed income portfolio's unrealized gains .

Capital Position and Shareholder Returns

Arch's capital position remains robust:

- Total capital: $26.9B at December 31, 2025

- Debt/capital ratio: 10.1%, down from 11.6% a year ago

- Share repurchases: $1.92B in 2025 ($7.78B cumulative)

- Remaining authorization: $1.1B

Management has been aggressive with buybacks, repurchasing 8.9M shares in Q4 alone at an average price of $90.04 .

Key Risks to Watch

-

Premium growth deceleration: Net premiums written down 4.5% YoY raises sustainability concerns

-

Bermuda tax changes: Higher effective tax rate (14.5% vs. 6.6%) will pressure future earnings

-

Catastrophe exposure: While Q4 was benign, Arch remains exposed to hurricane and earthquake risk

-

Mortgage segment normalization: The exceptional combined ratios may not persist as housing market conditions evolve

-

Investment portfolio duration: At 3.34 years, the portfolio is positioned for rate cuts but vulnerable to rate increases

The Bottom Line

Arch Capital delivered exceptional Q4 underwriting results with a 80.6% combined ratio and 38% EPS growth. The stock's 4.5% decline reflects investor concern about the 4.5% drop in net premiums written and the shift from growth to capital return. For long-term shareholders, the 22.6% book value growth and consistent beat track record suggest the business remains on solid footing — the question is whether premium growth can reaccelerate in 2026.

Conference Call: February 10, 2026 at 10:00 AM ET. Webcast available at archgroup.com/investors .

Data sources: Arch Capital Group Q4 2025 8-K filing (February 9, 2026), S&P Global Market Intelligence. Values retrieved from S&P Global where citations not provided.