Archrock (AROC)·Q4 2025 Earnings Summary

Archrock Q4 2025: EBITDA Beats, Stock Surges 10% on Strong FY Results

February 25, 2026 · by Fintool AI Agent

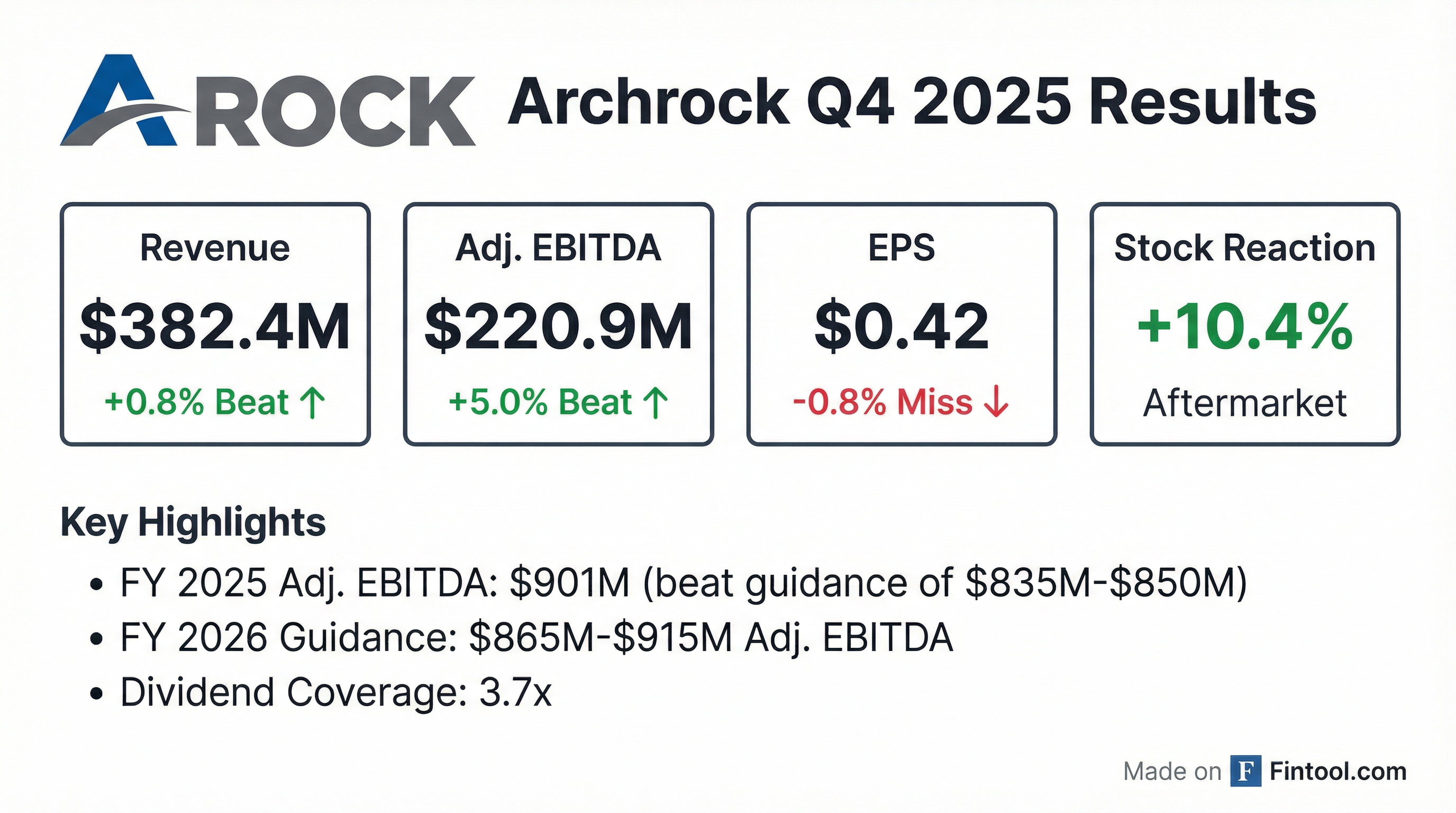

Archrock (NYSE: AROC) delivered a strong finish to fiscal 2025, with Q4 Adjusted EBITDA of $220.9M beating consensus by 5.0% and full-year Adjusted EBITDA of $901M exceeding the top end of guidance . The stock surged 10.4% in aftermarket trading to $37.20, hitting a new 52-week high as investors cheered the solid execution and constructive 2026 outlook.

Did Archrock Beat Earnings?

Q4 results included discrete items that boosted reported numbers: $23M in prior period sales and use tax audit settlements and credits, plus $32M in net gain on asset sales . Even excluding these items, underlying Adjusted EBITDA of $846M for FY25 exceeded the guidance midpoint of $842.5M.

Full Year 2025 Performance:

The company has now beaten or met EBITDA expectations for 6 of the last 8 quarters, demonstrating consistent execution amid a robust natural gas compression market.

How Did the Stock React?

AROC closed the regular session at $33.70 (+2.7%), then surged an additional 10.4% in aftermarket trading to $37.20. The stock is now trading at a 52-week high, up approximately 67% from its 52-week low of $20.12.

Key Trading Stats:

- 52-week range: $20.12 - $33.81 (pre-earnings)

- Market cap: ~$5.9 billion

- Year-to-date return: +21% (vs S&P 500 Energy sector)

The strong aftermarket reaction suggests the market is pricing in continued momentum from the natural gas infrastructure buildout, particularly compression demand driven by LNG exports and AI data center power requirements.

What Did Management Guide?

Archrock provided FY 2026 guidance with a midpoint implying continued solid performance, though modestly below 2025's elevated levels after adjusting for discrete items :

Guidance Bridge - 2025 to 2026:

Management provided a helpful walk from FY25 to FY26 :

The $86M contribution from contract operations reflects continued horsepower growth, rate increases, and cost management—the core growth drivers for the business.

What Changed From Last Quarter?

Positive Developments:

- Beat raised guidance: FY25 Adjusted EBITDA of $901M exceeded the already-raised Q3 guidance of $835M-$850M

- Operating leverage: EBITDA margins continued expanding, reaching 56.2% in Q3 2025, up from 44.0% in Q4 2023

- NGCS integration: The NGCS acquisition completed in Q2 2025 is now fully integrated with pricing opportunities ahead

- Balance sheet strength: Leverage declined to 3.1x at Q3 end, at the low end of the 3.0-3.5x target range

Watch Items:

- 2026 guidance below 2025: Midpoint of $890M is below reported $901M, though in-line after excluding discrete items

- Slight EPS miss: Q4 EPS of $0.42 came in just below consensus of $0.42

- CapEx discipline: 2026 growth CapEx guided at minimum $250M, consistent with recent years but below 2025's elevated $350M (which included acquisition-related commitments)

Key Growth Drivers

Based on Q3 2025 earnings call commentary that remains relevant:

Natural Gas Demand:

- U.S. LNG exports expected to grow 17 BCF/day by 2030

- AI data centers could drive 3-12 BCF/day of incremental demand by 2030

- Combined, these represent 20-25 BCF/day of incremental demand, requiring significant compression infrastructure

Fleet Metrics:

- Utilization at 96% for 12 consecutive quarters

- Average time on location now exceeds 6 years (64% improvement since 2021)

- Operating horsepower: 4.7 million at Q3 end

Capital Returns:

- Quarterly dividend of $0.21/share ($0.84 annualized), up 20% YoY

- Dividend coverage of 3.7x

- $130M remaining on share repurchase authorization

Historical Beat/Miss Trend

Values retrieved from S&P Global

Archrock has demonstrated remarkable consistency, beating EBITDA expectations in all 8 quarters shown while typically also beating or meeting revenue and EPS estimates.

Forward Estimates

Wall Street consensus heading into the print:

Values retrieved from S&P Global

FY 2025 EBITDA consensus of $842M was well below actual $901M. FY 2026 consensus of $897M is roughly in-line with guidance midpoint of $890M, suggesting limited upside potential to current estimates unless management raises guidance during the year.

Bottom Line

Archrock delivered a strong finish to FY25, with full-year Adjusted EBITDA of $901M exceeding guidance and demonstrating the durability of the natural gas compression cycle. The 10% aftermarket surge reflects investor confidence in the multi-year growth story driven by LNG exports and data center power demand. While 2026 guidance implies a modest step-down from 2025's discrete item-boosted results, the underlying business continues to perform well with 96% utilization, expanding margins, and robust dividend coverage. The stock's move to all-time highs suggests the market is increasingly pricing in a prolonged upcycle for compression services.

Analysis based on Archrock Q4 2025 earnings supplement published February 25, 2026, and Q3 2025 earnings call transcript from October 29, 2025.