COCA-COLA EUROPACIFIC PARTNERS (CCEP)·Q4 2025 Earnings Summary

CCEP Posts Record Year with 7% Profit Growth, Announces €1B Buyback

February 17, 2026 · by Fintool AI Agent

Coca-Cola Europacific Partners delivered a record FY2025, with revenue of €20.9 billion (+2.8% YoY), operating profit of €2.8 billion (+7.1%), and free cash flow exceeding €1.8 billion . The company announced a new €1 billion share buyback and guided to 3-4% revenue growth for 2026, with strong momentum in its zero portfolio and Monster Energy driving mix improvement .

Did CCEP Beat Earnings?

CCEP reported results essentially in-line with consensus, with FY2025 revenue of €20.9 billion compared to analyst expectations of €20.85 billion. The real story was profit delivery—operating profit grew 7.1% despite top-line growth of 2.8%, demonstrating pricing power and operational efficiency .

Key performance highlights for FY2025 :

- Revenue per case growth of 2.9%, with over a third from brand and pack mix

- Operating margin expanded ~50 basis points to 13.4%

- ROIC improved 70 basis points to 11.5%

- Returned €1.9 billion to shareholders (dividend + €1B buyback)

- Gross margin improvement contributed to profit beat

What Did Management Guide?

Management provided FY2026 guidance of 3-4% revenue growth and maintained its mid-term algorithm of 4% organic revenue growth and 7% operating profit growth .

2026 Guidance Summary

CEO Damian Gammell noted the revenue mix for 2026 should be "about a third from volume, a third from mix, and a third from price," emphasizing the strength of mix contribution from away-from-home recovery and premium packaging .

What Changed From Last Quarter?

Several notable developments emerged compared to Q3 2025:

Positives:

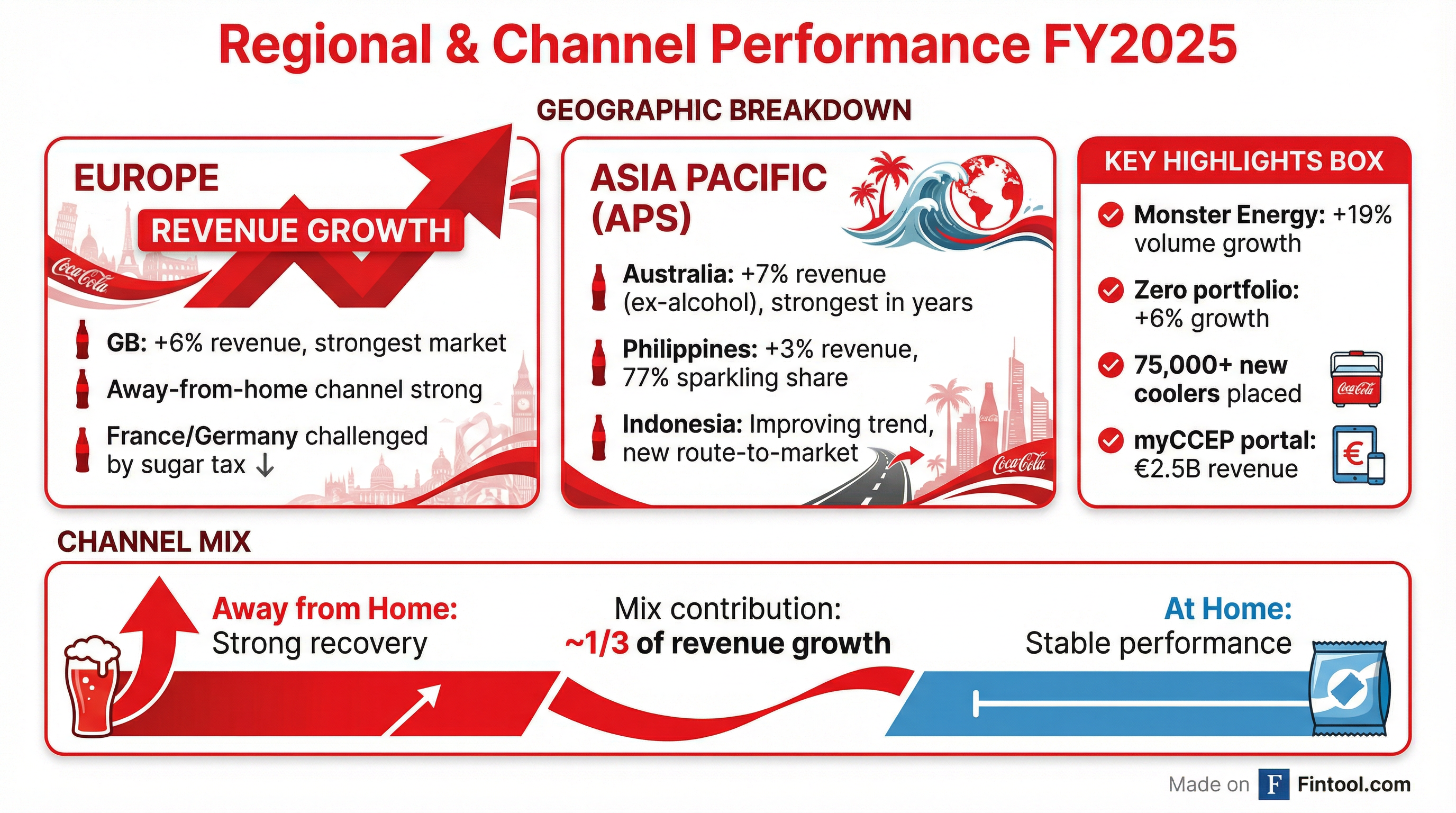

- Mix contribution strengthened: Brand and pack mix drove over a third of revenue per case growth, the strongest mix contribution in years

- Indonesia inflecting: After double-digit volume declines, Q4 showed improving trends with management expecting volume growth in 2026

- Away-from-home momentum: Channel outperformed, benefiting from new customer wins (Arsenal FC, Fullers, Jet2) and 75,000+ new cooler placements

- Monster strength: Energy volumes up nearly 20%, with Lando Norris becoming the #1 energy SKU in Europe

Challenges:

- Germany/France headwinds: Higher promo pricing and sugar tax increases pressured volumes in these key markets

- Suntory transition: Exit creating near-term revenue headwind of 0.5-1 percentage point, though strategically right decision

- Indonesia tea: Black tea remains under pressure, though flavored tea performing better

How Did the Stock React?

CCEP shares rose approximately 1.7% in after-hours trading to $101.18 following the earnings release, compared to the previous close of $99.51. The stock has gained 12.8% year-to-date and 14.7% over the trailing twelve months.

The modest positive reaction reflects:

- Results largely as expected, with profit execution impressing

- New €1B buyback provides support

- 2026 guidance slightly below mid-term algo (3-4% vs 4%) due to Suntory exit

- Indonesia turnaround still early days

Key Management Quotes

On mix strategy and revenue quality (CEO Damian Gammell):

"We've put a lot of effort into re-energizing away from home... more cooler placements. It was a record year for us in 2025, and it's great to see that coming through in the P&L through mix. A sustainable 4% will be a healthy mix of top-line volume, reasonable pricing, and brand and pack mix."

On Indonesia recovery (CEO Damian Gammell):

"Turnaround is a word I don't normally use about Indonesia, but I do see big improvements at the end of last year and starting this year... We expect Indonesia to grow this year, both in volume and revenue."

On energy category runway (CEO Damian Gammell):

"I expect that category to remain in its kind of 2- to 3-year cadence of mid-teens [growth]... we still have a job of work to do as a bottler in terms of distribution and bringing those brands to more locations. Will it be another year of 20+%? Who knows? It certainly has the potential."

On promotional effectiveness (CEO Damian Gammell):

"We are fully funded from a promo investment perspective... from now on, it's really more about promo effectiveness rather than quantity. And it's just finding ways to use those euros and dollars smarter to get a better return."

Segment Performance Deep Dive

Europe

- GB (largest single revenue market): +6% revenue growth, strongest performer

- New customer wins: Arsenal FC, Fullers, Jet2

- Monster and Dr. Pepper drove share gains

- Diet Coke benefited from "This Is My Taste" campaign with Jamie Dornan

- Germany: Challenging first half due to higher promo pricing, improved in H2

- France: Sugar tax impact on Coke Classic volumes, but brand performed stronger than expected

Asia-Pacific & Southeast Asia (APS)

- Australia: +7% revenue growth (excluding alcohol), strongest in many years

- Share gains in sparkling, energy, and sports

- Grinders coffee brand growing well

- Philippines: +3% revenue growth, record 77% sparkling value share

- EBIT margins expanded ~150 bps, on track to 10% target

- New Tarlac plant construction underway

- Indonesia: Volumes down double digits but improving trend

- New distributor-led route-to-market: 182 partners, 300 distribution points

- Sparkling performing better than tea

- Ramadan execution going well in Q1 2026

Capital Allocation & Balance Sheet

CCEP's capital allocation priorities remain unchanged :

Balance sheet highlights :

- Net debt/EBITDA at 2.7x, within 2.5-3x target range

- Weighted average cost of debt: 2.5%

- Investment grade rating maintained

- M&A optionality preserved, though no near-term opportunities identified

Forward Catalysts

Near-term (2026):

- FIFA World Cup activation starting now through July

- English Premier League sponsorship driving GB momentum

- Indonesia Ramadan execution (Q1 2026)

- New product launches: Sprite lemon mint, Fanta sour cherry, BODYARMOR in Spain/NZ

- Bacardi Spice Rum and Coke launch

Medium-term:

- Digital/AI transformation for promo optimization and demand forecasting

- Agentic AI applications for sales force enhancement

- Continued zero portfolio expansion (currently +6% growth)

- Manila shared service center scaling (100+ employees)

- Philippines plant completion in Tarlac

Risks & Concerns

Investor concerns raised on the call:

- Free cash flow guidance: €1.7B guide vs €1.8B delivered appears conservative—management noted higher CapEx investment needs

- Germany promotional strategy: Higher promo pricing backfired in H1 2025, though management addressed and improved in H2

- Indonesia sustainability: Early days on turnaround—management cautious about upside in guidance

- Sugar tax headwinds: France tax impacting Coke Classic volumes; GB DRS launch next year adds cost

What management avoided discussing:

- Specific margin guidance by region

- Detailed Indonesia profit contribution

- Quantified impact of AI investments on productivity

Historical Financial Trends

*Values in USD per S&P Global. Company reports in EUR.

The Bottom Line

CCEP delivered exactly what management promised—consistent execution on a record year across revenue, profit, and cash flow. The investment thesis remains intact: a defensive compounder in growing beverage categories with meaningful operating leverage and disciplined capital return. The 3-4% revenue guide for 2026 reflects known headwinds (Suntory exit) rather than fundamental weakness, and management's confidence in the mid-term algorithm (4% revenue, 7% EBIT) appears justified given mix improvement and Indonesia inflection.

Bull case: Mix tailwinds continue as away-from-home recovers, Monster maintains momentum, Indonesia turns profitable contributor, and AI/digital investments unlock productivity.

Bear case: Consumer weakness in Europe intensifies, Indonesia turnaround stalls, sugar taxes spread, and promotional environment compresses margins.

The new €1B buyback and growing dividend (€2.04/share) provide shareholder support, while the 2.7x leverage leaves M&A optionality intact. With shares trading at ~22x trailing earnings and the stock up 15% over the past year, the market appears fairly pricing CCEP's defensive growth profile.

Data sources: Company Q4 2025 earnings call transcript, S&P Global Capital IQ. Stock price data as of February 17, 2026.

View Full Earnings Transcript | CCEP Company Profile | Prior Earnings: Q3 2025