Clean Energy Fuels (CLNE)·Q4 2025 Earnings Summary

Clean Energy Beats on Revenue, Guides EBITDA Above Consensus

February 24, 2026 · by Fintool AI Agent

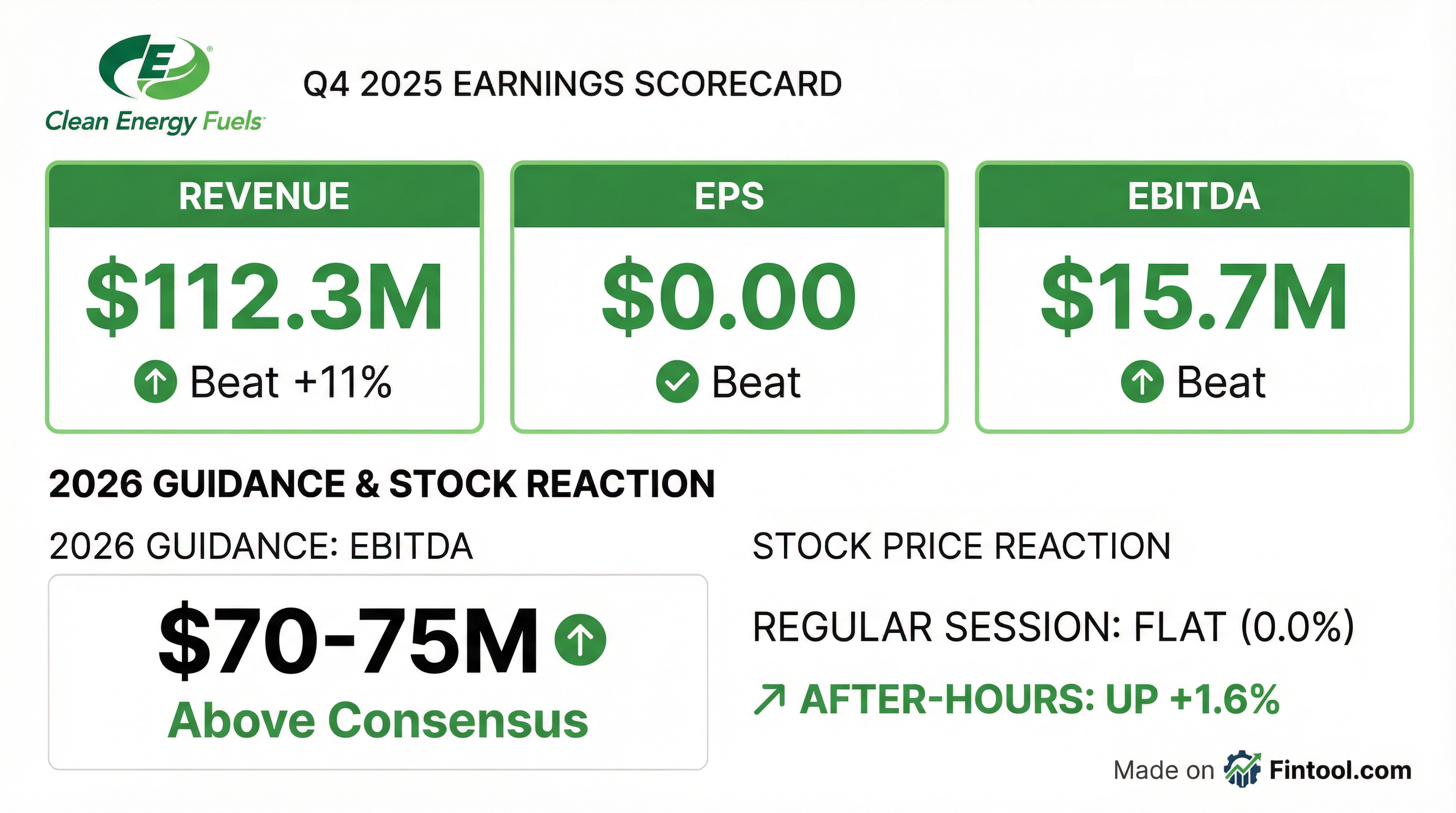

Clean Energy Fuels (NASDAQ: CLNE) delivered a solid Q4 2025, beating revenue and EPS estimates while guiding 2026 EBITDA above consensus expectations. The renewable natural gas provider reported revenue of $112.3 million versus the $101 million consensus (+11.2% beat) and Non-GAAP EPS of breakeven versus the -$0.04 estimate.

The stock closed flat at $2.54 (-0.78%) but rose 1.6% in after-hours trading to $2.58, suggesting investors are digesting the stronger-than-expected guidance.

Did Clean Energy Beat Earnings?

Yes — across all key metrics:

Revenue beat was driven by higher station construction sales ($10.7M vs $6.1M in Q4 2024), increased fuel sales, and continued growth in RNG volume.

The Non-GAAP EPS improvement came despite $24.8 million of incremental interest expense related to the company's $65 million debt paydown, of which $17.4 million was non-cash charges for unamortized debt issuance costs.

What Did Management Guide?

2026 guidance came in above consensus:

The guidance implies meaningful EBITDA improvement from FY 2025's $67.6 million, driven by continued RNG volume growth and the completed South Fork Dairy facility now online.

Management's 2026 outlook excludes acquisitions, divestitures, new joint ventures, and extraordinary events.

What Changed From Last Quarter?

Key operational developments:

-

South Fork Dairy RNG facility completed — One of the largest RNG production plants in the U.S. with 16,000 dairy cows capable of producing ~2.6 million gallons of low-carbon RNG annually

-

$65 million debt paydown — Company deleveraged balance sheet using available cash and investments, positioning for 2026

-

Expanded customer agreements — New RNG adoption deals across transit, freight, and municipal fleets reflecting "continued customer interest in near-term, scalable decarbonization solutions"

-

Freightliner demo program launched — Second heavy-duty truck demo featuring the 2026 Freightliner Cascadia Gen 5 with Cummins X15N natural gas engine

Key Management Commentary

CEO Andrew Littlefair struck an optimistic tone despite market volatility:

"Considering the rather volatile market, especially in the transportation sector, we are very pleased to end 2025 in a strong position with our operating results coming in slightly better than expected. This is a testament to Clean Energy's leadership position in the alternative fuel space and the product that we offer – RNG – being seen as the most viable, affordable, and ready-now clean fuel solution for fleets."

On competitive positioning:

"2025 saw significant retreats by other alternative solutions, but the number of transit buses, refuse trucks and heavy-duty trucks operating on RNG all grew throughout the year, resulting in the increase in our gallons sold."

Full Year 2025 Results

The wider GAAP loss was driven by $56.0 million of accelerated depreciation from LNG station equipment removal at 55 Pilot Flying J locations and a $64.3 million goodwill impairment charge.

Revenue Breakdown

The Alternative Fuel Tax Credit (AFTC) expired on December 31, 2024, creating a ~$6 million headwind. The company partially offset this through higher station construction revenue and improved fuel sales.

How Did the Stock React?

Muted initial reaction, aftermarket positive:

- Close: $2.54 (-0.78%)

- After-hours: $2.58 (+1.6% from close)

- 52-week range: $1.30 - $3.11

- Market cap: ~$557M

The stock has rallied ~16% from its early February lows of $2.20 heading into earnings, potentially pricing in some of the beat. The above-consensus 2026 guidance may provide support.

Balance Sheet Highlights

The $65 million debt paydown reduced long-term debt from $265M to $227M, strengthening the company's position heading into 2026. Cash and investments total $156.1 million (excluding restricted cash).

Forward Catalysts to Watch

- South Fork Dairy ramp — New facility should contribute incremental RNG volume throughout 2026

- Fleet adoption momentum — Track new customer wins in transit, refuse, and heavy-duty trucking

- LCFS/RIN credit prices — Lower credit values have pressured margins; any recovery would boost profitability

- Debt trajectory — Further deleveraging could improve financial flexibility

- Policy developments — Any reinstatement of AFTC or similar incentives would be a tailwind

Key Risks

- Commodity price exposure — RIN and LCFS credit prices remain volatile

- Policy uncertainty — AFTC expiration already impacting 2025 results

- Competition from EVs — Growing electric vehicle adoption in commercial trucking

- Capital intensity — RNG production facilities require significant upfront investment

- Amazon warrant dilution — $47M estimated non-cash charges in 2026

Conference call scheduled for 4:30 PM ET on February 24, 2026. Replay available at cleanenergyfuels.com.