EAGLE MATERIALS (EXP)·Q3 2026 Earnings Summary

Eagle Materials Beats Revenue But Misses on EPS as Wallboard Weakness Offsets Cement Strength

January 29, 2026 · by Fintool AI Agent

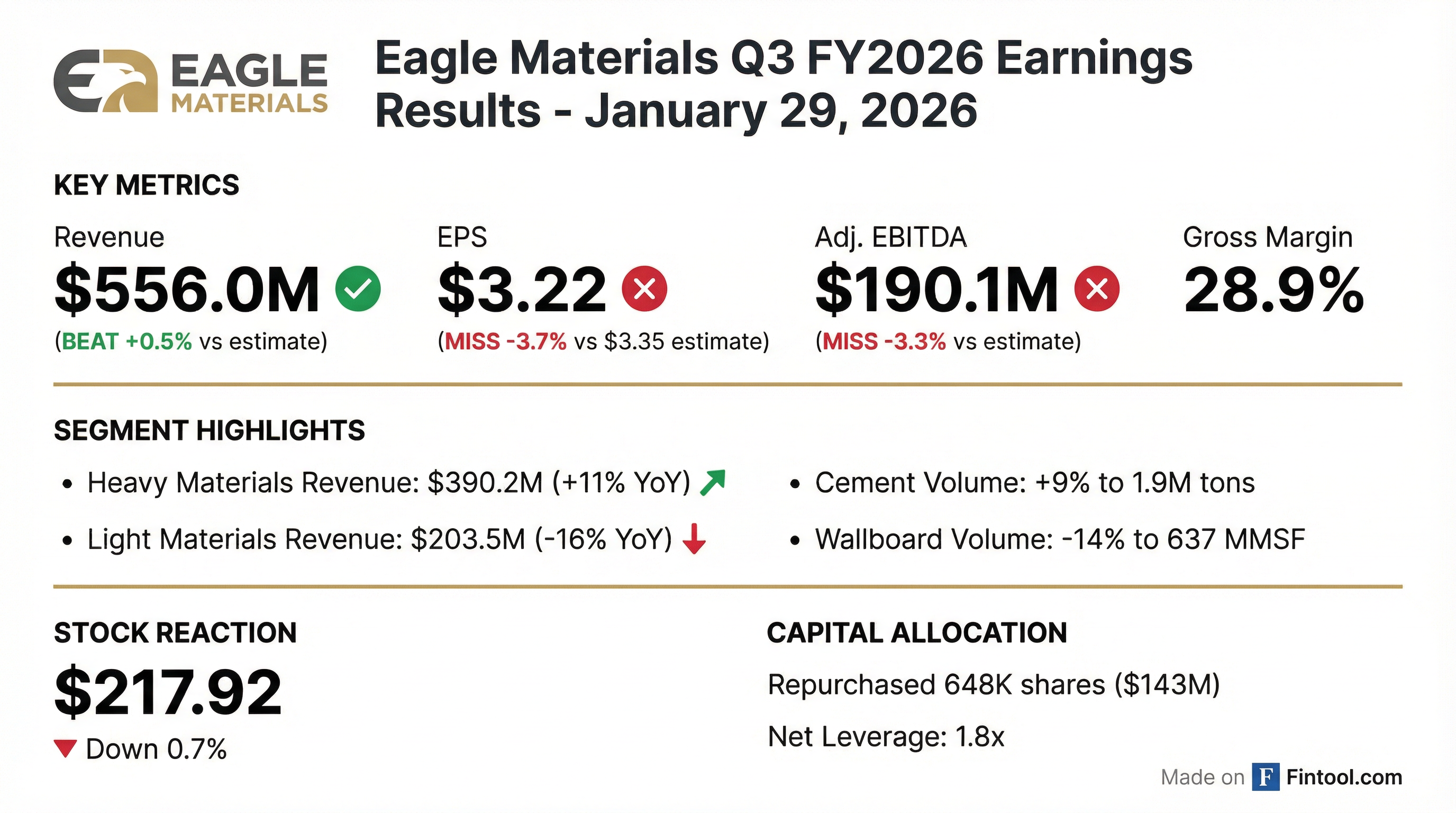

Eagle Materials (NYSE: EXP) reported Q3 fiscal 2026 results this morning with a modest revenue beat but missed on earnings, as strength in the Heavy Materials segment was offset by continued weakness in residential construction-exposed wallboard operations. The stock is trading down ~0.7% following the release.

Did Eagle Materials Beat Earnings?

Mixed results: Revenue exceeded expectations while both EPS and EBITDA came in below consensus.

This marks Eagle's fifth EPS miss in the last eight quarters, though the magnitude of misses has generally been modest. The company has demonstrated an ability to navigate challenging demand environments while maintaining healthy cash generation.

What Changed From Last Quarter?

The bifurcation between segments widened this quarter:

Key segment dynamics:

Heavy Materials (Cement, Concrete, Aggregates) — Operating earnings up 9% to $92.7M

- Cement volume +9% to 1.9M tons, though pricing slipped 1%

- Organic aggregates volume surged +34%, plus $7.6M contribution from recently acquired Pennsylvania business

- Infrastructure spending remains the key driver — "federal, state, and local spending on public infrastructure projects and private non-residential construction remained elevated"

Light Materials (Wallboard, Paperboard) — Operating earnings down 25% to $72.6M

- Wallboard volume -14% to 637 MMSF, pricing -5% to $225.19/MSF

- Paperboard volume -10% to 81K tons with pricing down 6%

- Residential construction headwinds persist due to affordability challenges

What Did Management Say?

CEO Michael Haack struck a cautiously optimistic tone despite the mixed environment:

"In our third quarter of fiscal 2026, despite the mixed construction environment, our businesses continued to perform well. We generated $556 million in revenue, our earnings per share were $3.22, and we delivered a gross profit margin of 28.9%."

On navigating cycles and operational strategy:

"At Eagle, we don't operate in a way that is overly focused on short-term demand cycles. Our primary products are essential commodities, meaning demand will fluctuate... Our low-cost producer position gives us opportunities and advantages for managing cost."

On the housing market outlook:

"Recent housing policy announcements, combined with more accommodative monetary and fiscal policy, recognize the fundamental need for new home construction in the U.S., so we are monitoring these developments closely."

Management highlighted ongoing investments in plant modernization at Laramie, Wyoming (cement) — commissioning expected late calendar 2026 — and Duke, Oklahoma (wallboard) — commissioning expected H2 calendar 2027.

Capital Allocation: Aggressive Buybacks Continue

Eagle continues to return significant capital to shareholders despite the challenging wallboard environment:

On the accelerated buyback pace, CFO Kesler noted: "Some of that's also relative to the stock price. So we still see value in the shares." Through nine months of FY26, the company has repurchased ~1.4 million shares (4% of outstanding).

How Did the Stock React?

EXP shares are trading down ~0.7% to $217.92 following the mixed results. The stock remains below its 52-week high of $262.81 reached in late November 2024.

The muted reaction suggests the miss was largely expected given ongoing wallboard weakness, while the strong cement/aggregates performance provided some offset.

Q&A Highlights: What Did Analysts Ask?

Texas cement market under pressure. CFO Craig Kesler acknowledged Texas is their most challenged market due to both import competition and structural changes from recent ownership changes: "Every time there are changes in it, people operate their plants a little bit differently and look at markets a little bit differently." This led to pricing adjustments.

Price increases announced for 2026. Management confirmed cement price increases of ~$8/ton in most markets excluding Texas and the West, with timing spread between January and April. "We have the volume momentum, and that's a good sign."

Natural gas hedging in place. With recent nat gas spikes from winter storms, CFO noted they are "a little more than 50% hedged here through the winter" for wallboard production costs. "There's not something that's structurally changed in the natural gas markets."

Repair & remodel provides stability. R&R represents approximately one-third of wallboard demand and "has been growing over the last many, many years" with "low single-digit type of growth" expected.

CapEx guidance lowered. Full-year fiscal 2026 CapEx now expected at $430-450M, down from prior guidance of ~$500M. "It's just timing" on the Mountain Cement and Duke projects, plus disciplined sustaining capital prioritization.

Wallboard pricing outlook. Despite the soft environment, management expects pricing to remain "range-bound" given structural industry changes: "I don't see anything changing from that perspective. I do think there's upside on pricing as we get housing to recover."

What's the Outlook?

Near-term headwinds:

- Residential construction remains pressured by affordability challenges

- Wallboard pricing continues to soften (-5% YoY)

- Seasonally weak Q4 (fiscal year ends March 31)

- Texas cement market facing competitive pressures from ownership changes and imports

Positive catalysts:

- Infrastructure spending continues to flow through — IIJA dollars still ramping

- Laramie cement plant modernization on track for late calendar 2026

- Duke wallboard modernization to start up H2 calendar 2027

- Aggregates acquisitions providing incremental growth

- Cement price increases announced for Q1 2026 in most markets

*Values retrieved from S&P Global

The key question for investors: When will residential construction recover? Management has maintained that housing affordability improvements are a matter of "when, not if" — and Eagle's low-cost position in wallboard provides operating leverage when volume returns.