Global Business Travel Group (GBTG)·Q4 2025 Earnings Summary

Amex GBT Beats Q4, Doubles Buyback to $600M — Stock Hits 52-Week Low

February 17, 2026 · by Fintool AI Agent

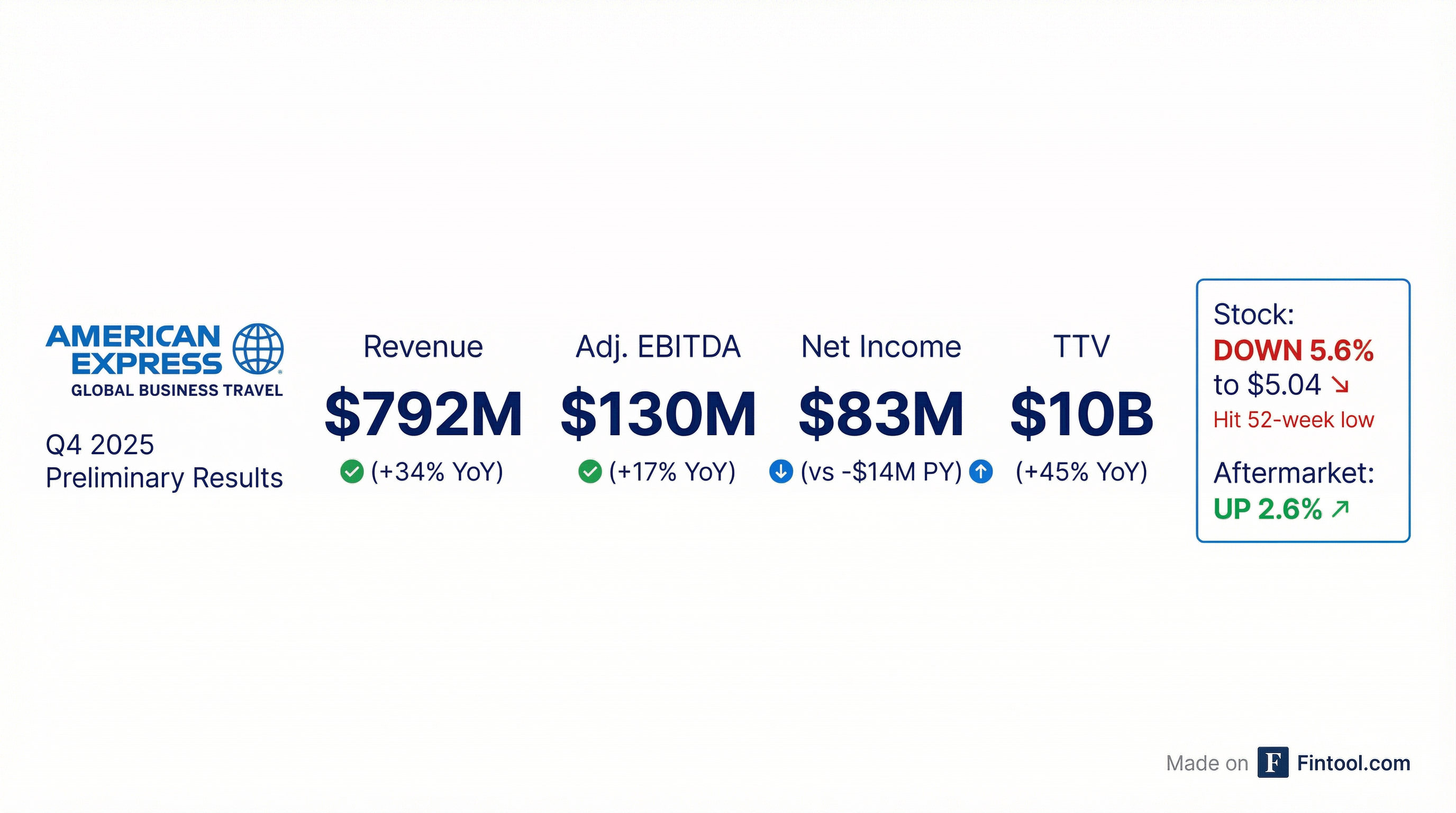

American Express Global Business Travel (NYSE: GBTG) reported preliminary Q4 2025 results that beat consensus estimates on both revenue and EBITDA, but shares fell 5.6% to $5.04 — a 52-week low — as the company reiterated rather than raised FY2026 guidance. The disconnect between solid operating results and poor stock performance reflects investor skepticism about valuation and organic growth trajectory.

Did Amex GBT Beat Earnings?

Yes, on both revenue and EBITDA — but barely.

*Values retrieved from S&P Global

The 34% revenue growth and 45% TTV growth were largely driven by the CWT acquisition, which closed September 2, 2025. Excluding CWT, organic growth was more modest.

Full-Year 2025 Results (Preliminary):

What Did Management Guide?

Guidance reiterated — not raised. This may have disappointed investors expecting an increase after strong Q4 results.

The guidance was first introduced in Q3 2025 as "preliminary expectations" and has now been confirmed without any adjustment. Management cited strong growth drivers including:

- CWT synergies: $155M net cost synergies over 3 years, with $55M already identified and actioned

- SAP Concur partnership: New flagship Complete T&E product launching Q1 2026

- AI-driven automation: Agentic AI capabilities in development

How Did the Stock React?

Stock cratered despite the beat. GBTG fell 5.6% to $5.04, hitting its 52-week low of $5.03 intraday before recovering slightly in after-hours trading to $5.17 (+2.6%).

The sell-off is part of a broader decline — GBTG has fallen ~44% from its 52-week high of $9.00. Possible explanations for the weak reaction:

- Guidance not raised despite strong Q4 results

- Preliminary/unaudited results create uncertainty

- Organic growth remains tepid — most growth is acquisition-driven

- Free cash flow decline — FCF dropped 37% YoY to $104M for FY2025

What's Different This Quarter?

The big capital allocation pivot. Management doubled down on buybacks, signaling confidence in the stock's undervaluation:

- Share repurchase authorization increased to $600M (up $300M from prior $500M)

- Year-to-date through November 2025, the company returned $54M to shareholders

Revenue and EBITDA Trend

Q4 2025 represents a step-change driven by CWT, breaking out of the $590M-$680M quarterly range the company had been operating in.

Key Catalysts Ahead

- Investor Day (March 2026): Management will provide more detail on the long-term opportunity

- Final Q4/FY2025 Results (March 9, 2026): Audited numbers may differ from these preliminary results

- SAP Concur Launch (Q1 2026): Next-gen Egencia T&E solution with AI-powered booking

- CWT Synergy Realization: $100M of remaining synergies to be captured over next 2-3 years

Risks and Concerns

- Government business exposure: CWT has government contracts impacted by U.S. government shutdowns

- Integration execution: CWT integration costs masked underlying profitability

- Business travel macro: Demand remains below pre-pandemic levels despite recent improvements

- Leverage: Total debt stood at $1.53B as of Q3 2025

The Bottom Line

Amex GBT delivered a clean beat on preliminary Q4 results with strong growth driven by the CWT acquisition. The doubling of the share repurchase program signals management confidence at current valuations. However, the lack of a guidance raise and continued stock weakness suggest investors want to see organic growth inflect higher before re-rating the stock. The March Investor Day will be the next major catalyst to watch.

Note: Q4 2025 and FY 2025 results are preliminary and unaudited. Final results will be released March 9, 2026.