GALAPAGOS (GLPG)·Q4 2025 Earnings Summary

Galapagos Closes Transformative Year With €3B War Chest, Stock Pops 4%

February 24, 2026 · by Fintool AI Agent

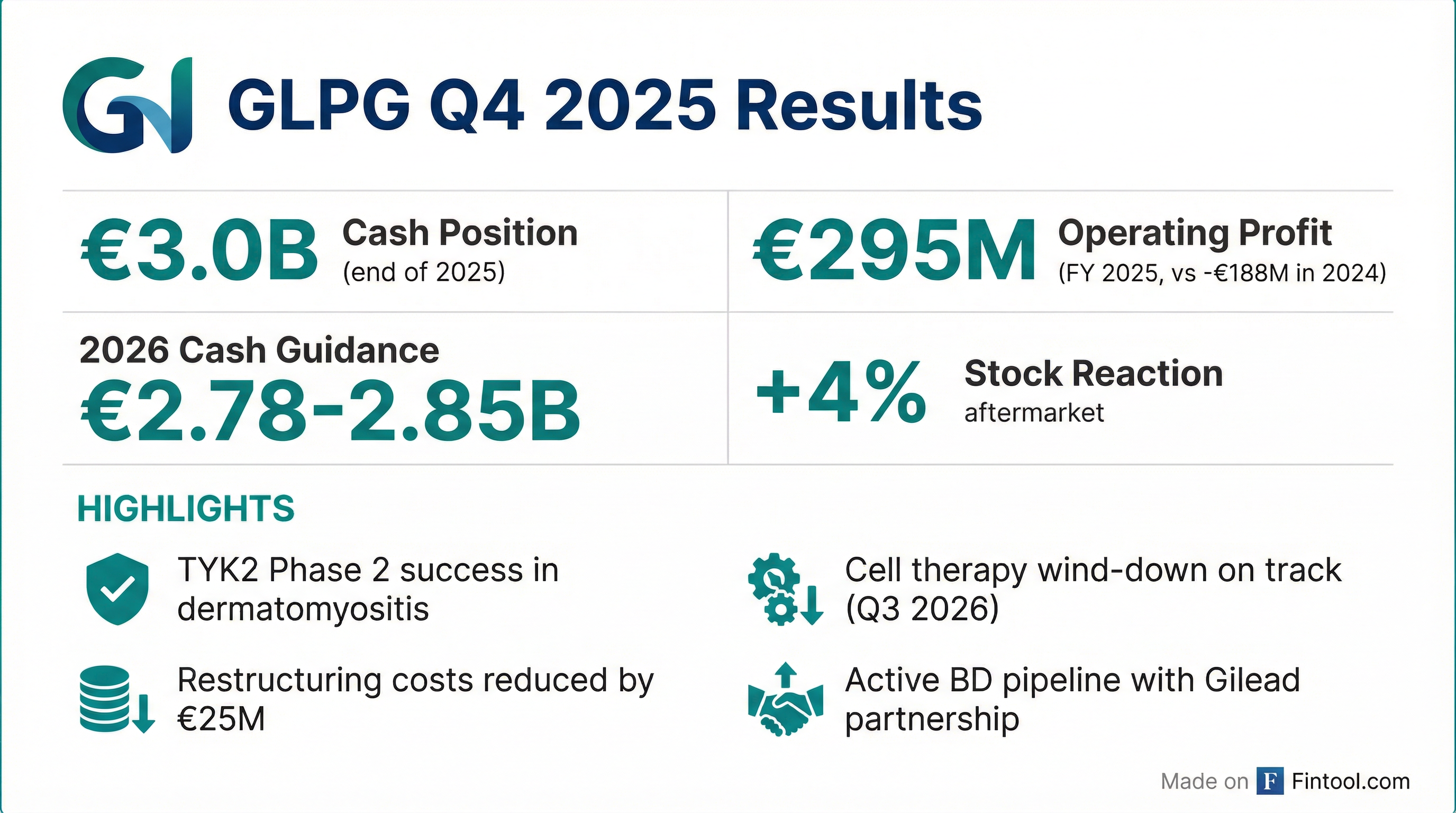

Galapagos (NASDAQ: GLPG) reported Q4 2025 results this morning, marking the conclusion of a pivotal transformation year that saw the Belgian biotech exit cell therapy, assemble a new management team, and position itself as a deal-driven platform with nearly €3 billion in deployable capital. Shares rose 4% in aftermarket trading to $35.24, reflecting investor optimism around the company's BD pipeline and strategic flexibility.

Did Galapagos Beat Earnings?

Traditional beat/miss analysis doesn't capture the Galapagos story this quarter. The company reported operating profit of €295.1 million for FY 2025 compared to an operating loss of €188.3 million in 2024—a €483 million swing driven primarily by non-cash accounting.

The headline number: Galapagos recognized €1.069 billion in deferred income from Gilead following the OLCA amendments and cell therapy wind-down. This represented the release of remaining contract liability from the 2019 Gilead agreement, which had been amortized over a 10-year term.

Values retrieved from S&P Global

The real story isn't profitability—it's capital preservation. Despite absorbing €275 million in cell therapy impairments, €124.8 million in restructuring costs, and ongoing R&D spend, Galapagos maintained a fortress balance sheet.

What Is Galapagos's Cash Position?

This is where it gets interesting for value investors. Galapagos ended 2025 with €2,998 million in cash, cash equivalents, and financial investments.

The company has been actively converting euros to dollars—now holding 72% of cash in USD versus 73% in EUR at year-end 2024. Management cited two reasons: anticipated U.S.-focused BD activity and higher yields on dollar deposits (4% vs 2% for euros).

"Our shares remain at a significant discount to the cash figures Aaron just reviewed. We will be focused on closing the gap through execution on our business development plan, thoughtful capital allocation, and engagement with shareholders to rebuild trust and confidence." — CEO Henry Gosebruch

What Did Management Guide for 2026?

Galapagos provided detailed cash guidance, signaling confidence in capital preservation despite ongoing restructuring:

Management expects to be cash flow neutral to positive by year-end 2026—a notable milestone given the ongoing restructuring. The restructuring cost estimate was reduced by €25 million from prior guidance of €150M–€200M, suggesting better-than-expected execution on the wind-down.

What Changed This Quarter?

TYK2 Success in Dermatomyositis

The headline clinical update: GLPG3667 (TYK2 inhibitor) met its primary endpoint in the Phase 2 dermatomyositis study, demonstrating statistically significant clinical benefit versus placebo with meaningful improvements on secondary measures.

The company is actively evaluating strategic options including potential partnerships with I&I specialists to accelerate Phase 3 development. Management acknowledged they don't have the internal infrastructure for late-stage development, making partnering the likely path forward.

"Given that we don't have the full infrastructure required to really take this into phase three, it makes sense to see where some of the players are that have that and maybe in working with a partner, we can do more, do it faster, do it more capital efficient and ultimately create more value." — CEO Henry Gosebruch

New Leadership Team in Place

Galapagos has assembled what management describes as a "world-class business development" team with collective experience across hundreds of life sciences transactions. Five new board directors have been added with deep transaction, capital allocation, and operating experience.

Cell Therapy Exit Nearly Complete

The wind-down of cell therapy activities, announced last fall, is now on track for substantial completion by end of Q3 2026, following completion of works council processes in January.

How Did the Stock React?

GLPG shares closed the regular session at $33.87, up 0.3% on the day. In aftermarket trading following the earnings release, shares jumped to $35.24, up 4.0%.

The stock has recovered significantly from its September 2025 lows near $23 when the cell therapy wind-down was announced, rallying on the TYK2 data in December and BD optimism.

What's the Gilead Angle?

The Gilead collaboration remains Galapagos's "key strategic advantage and potential competitive differentiation."

Key dynamics:

- OLCA still in force but expires in ~3 years

- Active dialogue with Gilead on potential transactions

- Gilead openness to contribute both upfront consideration and development spend on deals

- Combined firepower exceeds Galapagos's €3B alone

"In working with Gilead, we can go beyond the €3 billion we have. I think that's one of the features we think is very attractive in working with Gilead." — CEO Henry Gosebruch

If no deal materializes before OLCA expiration, the company would proceed independently, though management is clearly focused on leveraging the partnership.

Q&A Highlights

On deal timelines: Management declined to set a specific deadline, emphasizing "it's more important to do the right deal than to do a deal by a certain period of time." The OLCA expiration in ~3 years provides an outer boundary.

On TYK2 internal development: High bar for any asset, internal or external. Full Phase 2 data still coming in; partnering makes sense given lack of late-stage infrastructure.

On operating breakeven: Company expects cash flow neutral to positive by year-end 2026, with restructuring costs "chunky" throughout the year.

Investment Implications

Bull Case:

- Trading at ~30% discount to cash with €3B war chest

- Clean slate: cell therapy exit removes legacy drag

- TYK2 asset has de-risked with Phase 2 success

- Gilead partnership provides deal firepower beyond balance sheet

- New BD-focused team with transaction experience

Bear Case:

- No revenue-generating products; pure cash-burn story

- BD execution risk: need to deploy capital wisely

- OLCA expiration creates timeline pressure

- TYK2 likely to be partnered (limited upside capture)

- Biotech M&A market can be unpredictable

Forward Catalysts

This analysis was generated by Fintool AI Agent based on the Galapagos Q4 2025 earnings call transcript and supplementary financial data.

Related Links: