KILROY REALTY (KRC)·Q4 2025 Earnings Summary

Kilroy Realty Q4 2025: FFO Misses as 2026 Guidance Signals Occupancy Headwinds

February 9, 2026 · by Fintool AI Agent

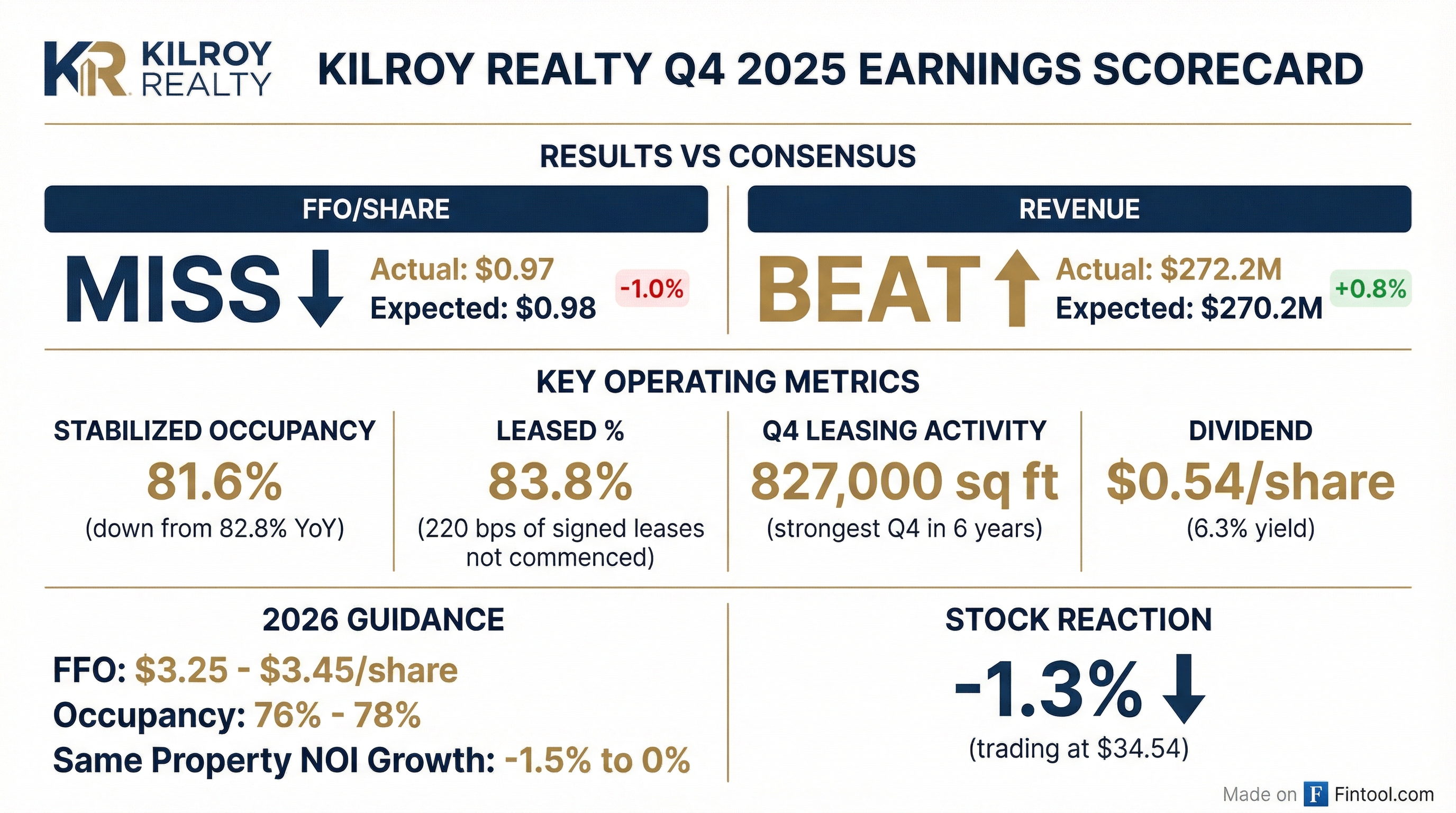

Kilroy Realty (NYSE: KRC) reported Q4 2025 results that painted a tale of two narratives: record leasing activity that capped an "exceptional year of execution," but a 2026 outlook signaling continued pressure on the West Coast office landlord. FFO of $0.97 per share missed consensus by a penny, while revenue of $272.2 million edged past estimates.

The stock slipped 1.3% to $34.54 in after-hours trading as investors focused on the soft 2026 guidance: FFO of $3.25-$3.45 per share represents an 18-23% decline from 2025's $4.20.

Did Kilroy Realty Beat Earnings?

The slight FFO miss comes after a string of beats through most of 2024-2025. Q4 2025 FFO of $0.97 was down 19% from $1.20 in Q4 2024, reflecting the ongoing challenges in West Coast office markets.

What Did Management Guide?

Kilroy's 2026 outlook reveals the bumpy path ahead:

Key assumptions embedded in 2026 guidance :

- Average occupancy excluding KOP 2: 80.0%-81.5%

- G&A and leasing costs: $89-91 million

- Gross interest expense: $212-214 million

- Total development spending: $150-200 million

The guidance implies continued dilution from the company's development pipeline, particularly the Kilroy Oyster Point Phase 2 life science project.

What Changed From Last Quarter?

Leasing momentum accelerated dramatically. Q4 2025 saw 827,000 square feet of leases signed—the strongest fourth quarter in six years. For the full year, Kilroy signed 2.05 million square feet, the highest annual volume since 2019.

But rent spreads remained deeply negative. GAAP rents on new leases fell 16.8% and cash rents dropped 27.1% from prior levels. Management attributed part of this to a tenant bankruptcy and a single-tenant renewal; excluding those, GAAP spreads would have been +16.2%.

Occupancy ticked up slightly. Stabilized portfolio occupancy improved to 81.6% from 81.0% sequentially, though still below 82.8% a year ago. Importantly, 220 basis points of signed leases haven't yet commenced, suggesting occupancy should improve in coming quarters.

How Did the Stock React?

KRC shares fell 1.3% to $34.54 in the session following earnings, extending the stock's decline from its 52-week high of $45.03. The stock now trades at a 6.3% dividend yield based on the $2.16 annual dividend.

The muted reaction suggests the weak 2026 outlook was partially priced in, given broader challenges facing West Coast office landlords.

Key Highlights: KOP 2 Leasing Breakthrough

The star of the quarter was Kilroy Oyster Point Phase 2, the company's 871,738-square-foot life science development in South San Francisco:

- UCSF signed a full-building lease spanning ~280,000 square feet, expected to commence in Q4 2027

- Acadia Pharmaceuticals signed ~16,000 square feet, commencing Q2 2026

- New genomic sequencing company took ~20,000 square feet in a spec suite and commenced immediately

KOP 2 is now 44% leased, up from 3% occupied, crushing management's prior goal of 100,000 square feet of lease executions for the year. The project was added to the stabilized portfolio in January 2026.

Capital Recycling Activity

Kilroy continued portfolio optimization through active capital recycling:

2025 Dispositions (Total: $466M)

Acquisitions

Pipeline Under Contract (~$290M expected)

- Kilroy Sabre Springs sale closed in January for $124.5M

- Santa Fe Summit land parcels under contract for $124M total

- 1633 26th Street under contract for $41M

Balance Sheet Position

Kilroy ended Q4 with solid liquidity despite the challenging environment:

The company refinanced $400M of notes in August 2025, issuing 5.875% senior notes due 2035 to redeem 4.375% notes that were maturing.

CEO Commentary

Angela Aman, CEO, struck an optimistic tone despite the challenging numbers:

"Our strong performance in the fourth quarter capped off an exceptional year of execution by the entire Kilroy Team. We captured growing tenant demand for high quality, well-amenitized office and life science projects across virtually all of our submarkets."

"As we look ahead to 2026, we are encouraged by the continued momentum we are experiencing across our platform and believe we are well positioned for continued growth and evolution."

Regional Occupancy Breakdown

San Francisco and San Diego showed improvement, while Los Angeles continued to struggle.

Lease Expiration Schedule

Kilroy's near-term lease expiration profile appears manageable:

The largest exposure comes in 2031 when 18.5% of leased space expires with $154.8M of annualized base rent.

What to Watch

-

KOP 2 lease-up: Can Kilroy find tenants for the remaining 56% of the 872,000 sq ft project? The UCSF deal was a major win, but more is needed.

-

Rent spreads: Will the -27% cash rent spread normalize, or is this the new reality for West Coast office?

-

Occupancy trajectory: The 76-78% guidance implies continued decline before stabilization. Watch for inflection signs.

-

Capital recycling execution: ~$300M of targeted dispositions in 2026 plus the pending land sales.

-

Interest rate sensitivity: With $4.6B of debt at an average rate approaching 6%, any refinancing will pressure FFO.

Conference Call Details

Management will discuss Q4 results on the earnings call scheduled for February 10, 2026 at 10:00 AM PT.

Data sourced from Kilroy Realty Q4 2025 Supplemental Financial Report and S&P Global.