KKR Real Estate Finance Trust (KREF)·Q4 2025 Earnings Summary

KREF Q4 2025: Management Pivots to Aggressive Asset Resolution, Dividend Under Review

February 4, 2026 · by Fintool AI Agent

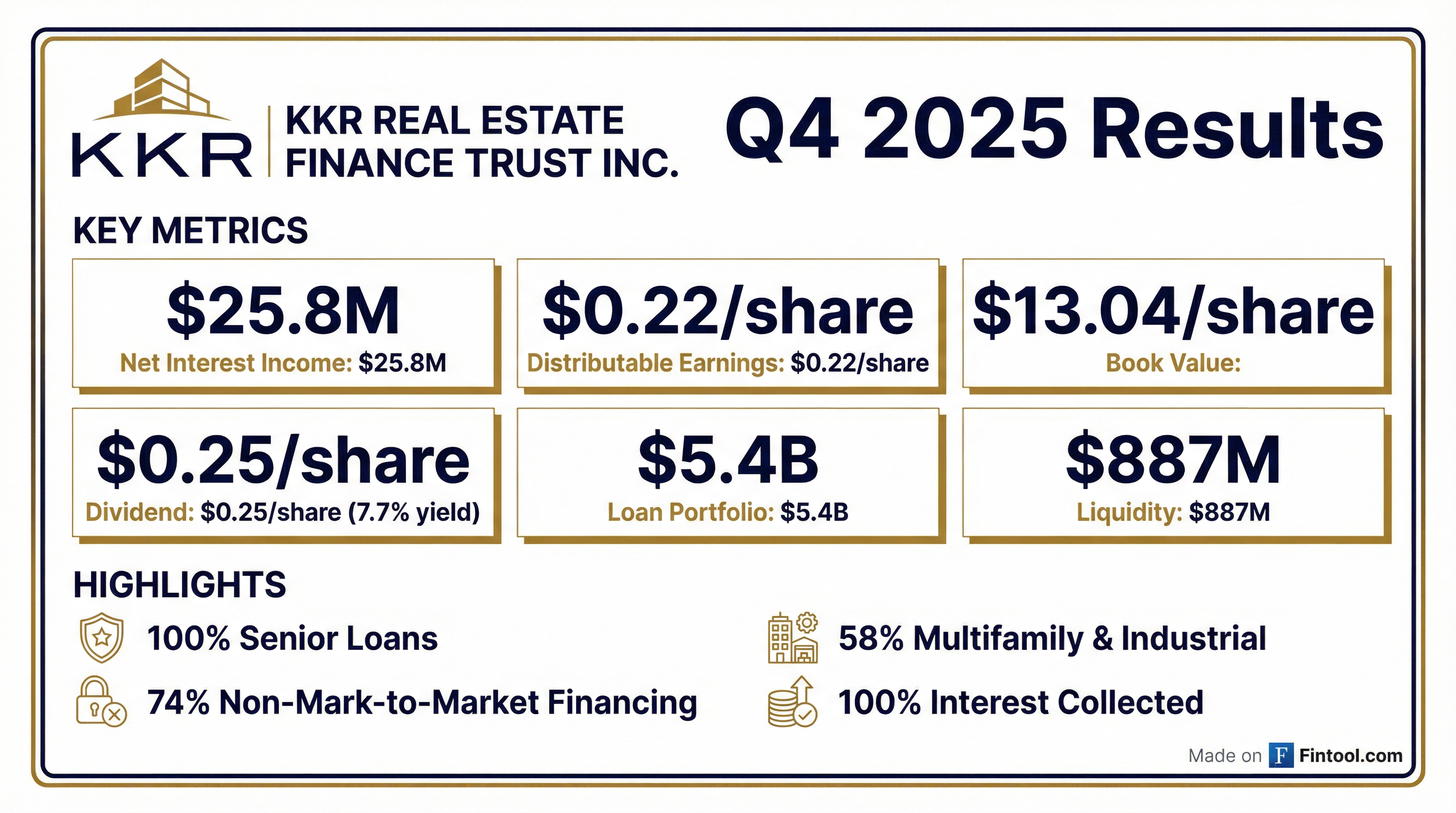

KKR Real Estate Finance Trust (NYSE: KREF) reported Q4 2025 results that brought the most significant strategic shift in the company's recent history. While distributable earnings rebounded to $0.22 per share and book value declined to $13.04, the real story from the earnings call was management's announcement of an "aggressive resolution strategy" for 2026 aimed at compressing the persistent discount to book value. CEO Matt Salem flagged that the dividend is now under active board review as the company navigates what he called a "transitional year."

Did KREF Cover Its Dividend?

The key question for mortgage REIT investors: barely. KREF maintained its $0.25 quarterly dividend, but Q4 distributable earnings of $0.22 covered only 88% of the payout.

For full year 2025, distributable earnings totaled just $0.39 per share against $1.00 in dividends paid—a 39% coverage ratio that signals the dividend may be at risk if credit losses persist.

What Is KREF's 2026 Strategy?

The most important development from the Q4 call was management's pivot to an aggressive portfolio resolution strategy. CEO Matt Salem outlined a multi-pronged approach to compress the stock's 37% discount to book value:

REO Asset Disposition Timeline:

Key Management Quote on Mountain View:

"Everything we're seeing today would suggest that I think we've got significant value in that asset above where we're carrying it today... The market continues to improve meaningfully, and we remain engaged with tenants." — CEO Matt Salem

Management quantified the embedded upside: approximately $0.13 per share is locked in REO assets that can be unlocked by converting them back to performing loans.

Watchlist Resolution Goals:

Salem stated the goal is to "monetize or liquidate the vast majority" of the watchlist by year-end, particularly office and multifamily loans. For life science assets, management will evaluate market liquidity before committing to aggressive timelines.

"The overall goal is to compress the discount of our stock price to book value and more quickly unlock approximately $0.13 per share embedded in our REO assets. However, this strategy will also put additional pressure on earnings until we're able to fully execute the plan." — CEO Matt Salem

Is the Dividend at Risk?

This was the elephant in the room. Salem was unusually direct about the board's deliberations:

"The dividend is something the board is actively evaluating as part of a broader capital allocation discussion, particularly as we work through a transitional year for the portfolio. Our priority is to make disciplined decisions that balance near-term earnings visibility and long-term shareholder value."

When pressed by analysts on whether to interpret this empirically rather than as market signaling, Salem agreed: "That's a fair articulation of how we're thinking about it now."

Translation: If 2026 resolution activities create near-term earnings pressure (as management explicitly warned), the $0.25/share quarterly dividend may be cut. The market is already pricing this risk—the 12%+ yield on stock price suggests investors see the current payout as unsustainable.

What Drove the CECL Provision?

The $44 million Q4 provision ($0.67 per share) was driven by two rating downgrades:

Watch List Expanded to 5 Loans ($572M):

The cumulative CECL allowance now stands at $204 million, representing 381 basis points of loan principal—up from 302 bps last quarter.

Important Warning: Management noted they expect to downgrade the Boston Life Science loan in Q1 2026. However, COO Patrick Mattson clarified on the call that "that asset is paying its contractual interest. We expect in the near term that it will continue to pay contractual interest." The modification discussions are ongoing.

What Does the Portfolio Look Like?

KREF's $5.4 billion loan portfolio remains 100% senior secured, with multifamily and industrial representing 58% of exposure:

Key Portfolio Metrics:

- Weighted Average LTV: 66%

- Weighted Average Risk Rating: 3.2 (up from 3.1)

- Weighted Average Unlevered Yield: 7.3%

- 100% Interest Collected in Q4

How Did Originations Perform?

Q4 was active on the origination front with $424 million in new loans, including KREF's first-ever European investments — a milestone CEO Salem highlighted as "an important step" in geographic diversification:

Full year 2025 originations totaled $1.1 billion with $1.0 billion funded across 12 floating-rate senior loans.

Is the Balance Sheet Defensible?

KREF emphasized its conservative liability structure:

Liquidity Position: $887 Million

- Cash: $85 million

- Undrawn Corporate Revolver: $700 million

- Loan Repayments Held by Servicer: $74 million

- Available Borrowings: $28 million

Financing Highlights:

- 74% of secured financing is fully non-mark-to-market

- No final facility maturities until 2027

- No corporate debt due until 2030

- Total financing capacity of $8.2 billion with $3.5 billion undrawn

The non-MTM structure is critical—it means KREF won't face margin calls if property values decline further, unlike some peers with mark-to-market facilities.

What About Share Buybacks?

Management has been active buying back stock at discounts to book value:

At the current $8.18 stock price vs. $13.04 book value, buybacks are accretive—but they also consume cash that could otherwise support the dividend or build credit reserves.

How Did the Stock React?

KREF closed at $8.18 on February 3, down 1.2% on the day the earnings slides were released. The stock trades at:

- 37% discount to book value ($8.18 vs. $13.04)

- 12.2% dividend yield on stock price (annualized $1.00 dividend)

- 52-week range: $7.55 - $11.53

The persistent discount reflects investor concerns about:

- Office and life science credit deterioration

- Dividend sustainability given coverage below 100%

- Potential for additional CECL provisions in 2026

What Should Investors Watch?

Near-Term Catalysts:

- Q1 2026 Dividend Decision — Board is actively evaluating; expect announcement in coming months

- Mountain View Lease Announcement — Management is "engaged with tenants" in an improving market; lease could unlock significant value

- REO Liquidation Progress — Short-term assets (West Hollywood, Portland, Raleigh, Philadelphia) targeted for 2026 sales

- Boston Life Science Downgrade — Q1 2026 CECL impact uncertain, but loan still paying contractual interest

- 2026 Repayment Activity — Over $1.5B expected, above prior two years, providing reinvestment flexibility

Full Year 2025 Summary:

What Did Analysts Ask About?

The Q&A session revealed investor focus on strategic alternatives and life science risk:

On the ARI Transaction (Apollo's strategic shift): When asked if KREF would consider a similar business revamp if the discount persists, Salem pushed back:

"I don't want to draw any direct correlation to KREF. I think we've got our business plan. We've got our strategy, and we're really focused on implementing that... My expectation is if we show up with a clean portfolio, a newer portfolio, that the market will price it. I think the market's efficient."

On Life Science Outlook: Analyst Jade Rahmani cited Alexandria's 5+ year timeline for life science recovery. Salem's response was notably more optimistic:

"I remember when we foreclosed on Mountain View, everybody in the market, including the most sophisticated brokers, told us it was going to be five years before we could get anything done there. I'll take the under on that by a few years, and I'll take the over on the value creation that we make there."

On AI's impact on life science demand: "I'm not convinced that's a negative for the life science sector. I think it could be actually quite a positive in terms of the development and need for development of new drugs and need for new lab space."

On Office Lending Strategy: Management is selectively originating new office loans, focusing on:

- Newer, high-quality Class A assets

- Stabilized cash flows with long-term leases already in place

- Top-tier markets with strong leasing velocity

- Low repositioning risk

On Market Sentiment (KKR Perspective): Salem provided valuable color on institutional capital flows:

"We are seeing increased allocation to both real estate credit as well as real estate equity... A lot of institutional allocators of capital are looking at their overall portfolio and thinking about where those values have gone over the course of the last five years and seeing that real estate's been relatively stagnant. And so you're starting to see a shift back into that sector."

He noted there's "not a lack of buyers in the market—there's a lack of sellers at a price."

Key Takeaways

- Aggressive 2026 Resolution Strategy — Management will accelerate REO and watchlist dispositions to compress the discount to book value, with $0.13/share embedded in REO assets

- Dividend Under Active Review — Board is evaluating the payout as part of capital allocation during this "transitional year"

- Mountain View Upside — Management believes "significant value" above carrying exists, with improving market and active tenant engagement

- Distributable Earnings Rebounded to $0.22/share from losses in Q2/Q3, but GAAP loss was ($0.49) due to $44M CECL charge

- 2026 Repayments Expected to Exceed $1.5B — Higher than prior two years, providing reinvestment capacity

- European Expansion Milestone — Closed first KREF loan in Europe, positioning for geographic diversification

- Balance Sheet Defensive — 74% non-MTM financing, $887M liquidity, no maturities until 2027

Data sourced from KREF Q4 2025 earnings call transcript and supplemental information dated February 4, 2026.