MERCADOLIBRE (MELI)·Q4 2025 Earnings Summary

MercadoLibre Q4 2025: Revenue Beats as LatAm E-Commerce Juggernaut Accelerates

February 24, 2026 · by Fintool AI Agent

MercadoLibre delivered a strong Q4 2025 with revenue of $8.76 billion, beating consensus by 3.5%, while EPS of $11.03 missed estimates by 3.5% as management prioritized aggressive investment over near-term profitability. The stock rose +3.1% on the results, with aftermarket trading pushing shares to $1,957, as investors embraced the growth-over-margins playbook that has fueled MELI's dominance across Latin America.

The quarter capped a transformational year: revenue grew 39% for full-year 2025, the credit portfolio more than quadrupled over three years to $12.5 billion, and the company completed its planned CEO transition with Ariel Szarfsztejn taking the helm.

Did MercadoLibre Beat Earnings?

Revenue significantly outpaced expectations, driven by:

- Brazil accelerating to +48% YoY revenue growth (+37% FX-neutral)

- Mexico surging +56% YoY (+41% FX-neutral)

- Fintech revenue growing +51% YoY as credit and acquiring scaled

The EPS miss was deliberate. Management estimated strategic investments in free shipping, cross-border trade, first-party sales, and credit cards cost 5-6 percentage points of operating margin in Q4. Excluding $99M of one-off Brazilian tax credits, operating income declined 4% YoY with margins at 9.0%.

How Did the Stock React?

MELI shares closed at $1,922.56, up +3.1% on the day, with aftermarket trading pushing the stock to $1,957 (+1.8% from close). The positive reaction despite the EPS miss suggests investors are prioritizing the accelerating top-line growth and market share gains over near-term profitability.

The stock had dropped -6.6% in the prior session, potentially pricing in some earnings risk after a run-up from the January lows. At $1,922, MELI trades at ~97x trailing earnings and ~35x forward NTM EPS, reflecting premium growth expectations.

What Changed From Last Quarter?

Key shifts from Q3 2025:

-

Brazil Reaccelerated: FX-neutral GMV growth jumped from 34% in Q3 to 35% in Q4, with sold items up 45% YoY and unique buyers growing 26%. The lower free shipping threshold (R$19) is driving clear behavioral changes in new cohorts.

-

Mexico Hit Record Fulfillment: Fulfillment penetration reached a record ~80%, supporting the best quarterly performance of the year with 35% FX-neutral GMV growth.

-

Argentina Stabilized: After volatility in Q3, demand stabilized in Q4 with 42% FX-neutral GMV growth and 36% items sold growth.

-

Credit Portfolio Inflection: Total credit portfolio grew 90% YoY to $12.5 billion, with credit card NPLs falling to a historic low of 4.4% (down 300bps over 3 years).

-

CEO Transition Completed: On January 1, 2026, Ariel Szarfsztejn became CEO while founder Marcos Galperin transitioned to Executive Chairman.

What Are the Key Performance Metrics?

The platform effects are compounding: unique buyers surpassed 80 million for the first time, with the year-on-year addition of almost 16 million being the highest ever. Higher frequency and engagement (9.0 items per buyer, up 15% YoY) is offsetting new cohort dilution.

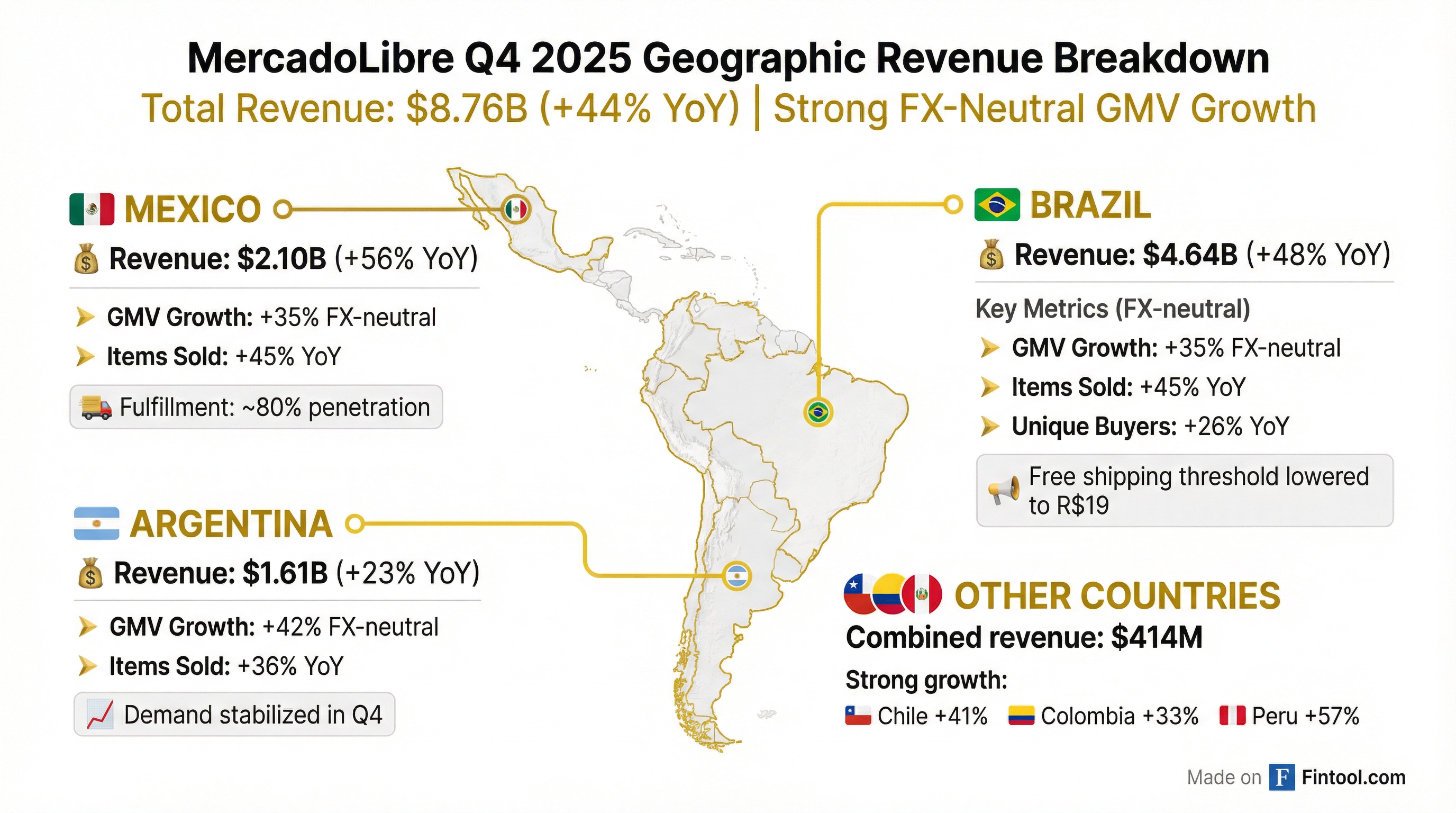

How Is Each Geography Performing?

Brazil (53% of Revenue)

- Revenue: $4.64B (+48% YoY, +37% FX-neutral)

- FX-neutral GMV: +35% YoY

- Unit shipping costs: -11% YoY in local currency

The lower free shipping threshold to R$19 is transforming user behavior. New cohorts purchase more items across more categories with higher retention. The ratio of monthly to quarterly buyers has increased, signaling improving frequency.

Mexico (24% of Revenue)

- Revenue: $2.10B (+56% YoY, +41% FX-neutral)

- FX-neutral GMV: +35% YoY

- Fulfillment penetration: ~80% (record high)

Mexico Acquiring TPV grew 50% FX-neutral YoY as SMB merchant onboarding accelerated. The installed base of active POS devices is approaching that of all incumbents combined.

Argentina (18% of Revenue)

- Revenue: $1.61B (+23% YoY, +77% FX-neutral)

- FX-neutral GMV: +42% YoY

- MELI+ launched May 2025 with early momentum

Growth moderated in USD terms as inflation decelerated, but underlying FX-neutral metrics remain strong.

What Is Management Investing In?

Management explicitly flagged 5-6 percentage points of operating margin impact from strategic investments:

1. Free Shipping Expansion

Extended free shipping to items starting from R$19 (previously R$79) in Brazil. While this compresses near-term margins, new buyer cohorts show better retention, higher frequency, and broader category adoption.

2. Cross-Border Trade (CBT)

CBT GMV grew 74% FX-neutral in Q4. MELI opened its first fulfillment center in China in December, enabling direct fulfillment to all five major markets. The China-LatAm corridor is expected to see incremental investment in 2026.

3. First-Party (1P) Sales

1P GMV grew 80% in 2025 to over $4 billion. Automation in ordering, pricing, and inventory management has improved assortment while reducing markdowns. 1P is critical for the Supermarket category strategic priority.

4. Credit Card Scaling

Issued ~3 million credit cards in Q4 alone by leveraging marketplace peak season. The credit card portfolio's 15-90 NPL has fallen to 4.4%, and approximately 75% of Brazilian cards have reached first NIMAL breakeven within 12-18 months.

How Is the Fintech Business Performing?

Fintech revenue grew 51% YoY and represented a growing share of the total business:

Mercado Pago achieved leading NPS among all players in Brazil, Mexico, Argentina, and Chile after years of patient investment. The strategy of paying attractive yields on deposits (AUM grew from $2B to ~$19B in three years) is disrupting incumbents and driving cross-sell opportunities.

Credit Portfolio Mix (Q4 2025):

The credit business is scaling with improving quality:

- NPLs declining: 15-90 day past dues fell to 16.8% (from 17.6% in Q3), while provision coverage rose to 150%

- NIMAL expanded to 23.3% (from 21.0% in Q3) driven by higher spreads in consumer and merchant loans

- AI Assistant launched in October handled 9M+ conversations with 90% resolution rate

What Is the AI Strategy?

MELI is embedding AI across both Commerce and Fintech:

Commerce:

- AI-enhanced search in Argentina uses individual buyer behavior to personalize results

- Interactive assistant refines broad searches through product attributes

- Seller Assistant accelerates onboarding, improves listing quality, and creates short-format videos from single photos

Fintech:

- Mercado Pago AI Assistant launched October 2025, handling 9M+ conversations

- Nearly 90% resolved without human intervention

- Capabilities expanding to proactive interactions

Sales & Operations:

- AI tools improving sales team effectiveness in identifying new customers

- Supporting higher TPV per merchant and shortened payback periods in Brazil

What Did Management Guide?

Management did not provide explicit quantitative guidance but signaled:

-

Investment continues in 2026: "Our investment plan for 2026 will be consistent with this bold and disciplined approach to investing behind long-term growth."

-

Confidence in long-term GMV multiple: "When we consider the strength of our position...we believe our GMV could be multiple times larger over the long term."

-

Profitability will mature as initiatives scale: Management is confident that free shipping, CBT, 1P, and credit card initiatives will improve profitability while reinforcing competitive advantages.

What Is the Balance Sheet Position?

The balance sheet remains strong with available cash nearly doubling YoY to $11.4 billion. Adjusted free cash flow of $1.5 billion for full-year 2025 demonstrates the business generates meaningful cash even while investing heavily in growth. Net debt increased to $4.7 billion primarily to fund credit portfolio expansion ($12.5B portfolio vs. ~$6.6B a year ago).

What Are the Key Risks?

-

Margin Pressure May Persist: The 5-6ppt margin investment drag may continue into 2026 as initiatives scale.

-

FX Exposure: Revenue is denominated in volatile LatAm currencies while costs are partially USD-denominated.

-

Credit Quality: While NPLs are at historic lows, rapid portfolio growth (90% YoY) during economic uncertainty bears watching.

-

Competitive Intensity: Amazon, Shopee, and local players continue investing in the region.

-

Argentina Macro: Currency and inflation dynamics remain unpredictable.

What's the Bottom Line?

MercadoLibre delivered exactly what long-term investors want: accelerating revenue growth, deepening competitive moats, and clear strategic priorities—even at the cost of near-term EPS. The company is investing through the cycle to capture what it calls "one of the biggest e-commerce growth opportunities in the world."

The Q4 results validate the playbook: Brazil reaccelerated after the free shipping extension, Mexico hit record fulfillment, fintech achieved leading NPS across major markets, and the credit portfolio scaled with improving quality. The CEO transition adds execution risk, but with founder Marcos Galperin remaining as Executive Chairman, strategic continuity appears assured.

At ~35x forward earnings, MELI remains a premium growth story. The market's positive reaction to an EPS miss suggests investors remain comfortable with the investment thesis: this is a company trading short-term margins for long-term dominance.