PERPETUA RESOURCES (PPTA)·Q4 2025 Earnings Summary

Perpetua Resources Advances Stibnite Gold Project with $720M Cash War Chest

February 23, 2026 · by Fintool AI Agent

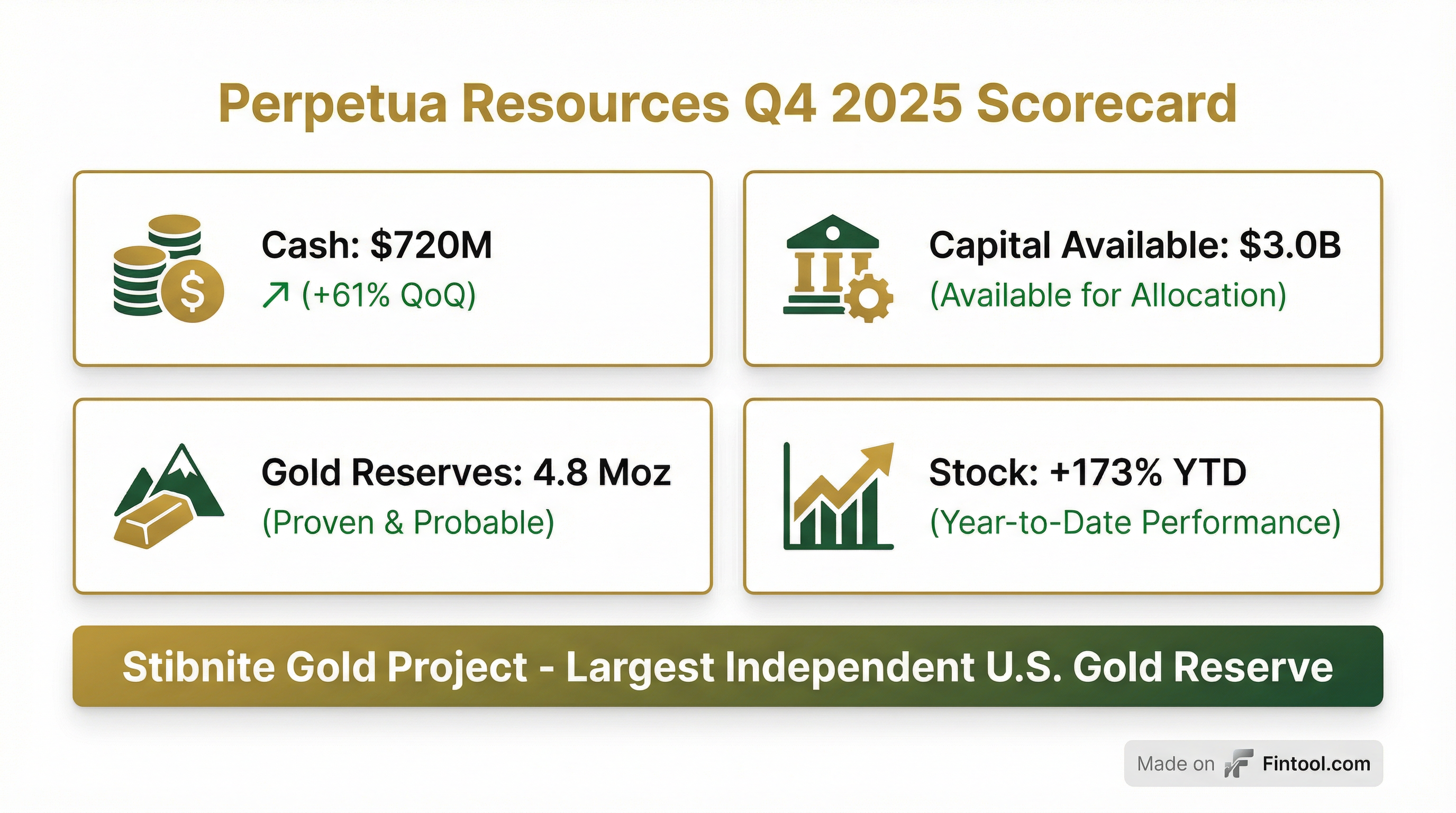

Perpetua Resources (NASDAQ: PPTA) filed an 8-K today with an updated investor presentation showing a cash balance of approximately $720 million as of December 31, 2025 . The pre-production gold miner continues advancing the Stibnite Gold Project in Idaho—the largest independent U.S. gold reserve—with up to $3.0 billion in capital now available for development .

The stock is up 173% year-to-date, trading at $30.18 with a market cap of $3.7 billion, as investors anticipate the company's transition from development to production by 2029.

How Strong is the Cash Position?

Perpetua's cash position has transformed dramatically over the past year:

The Q4 2025 cash increase of ~$274 million from Q3 reflects additional strategic equity investments and private placements, including transactions with Agnico Eagle and JPMorgan Chase totaling $317 million .

What Capital is Available for the Project?

Perpetua has outlined up to $3.0 billion in available capital from multiple sources :

The U.S. Export-Import Bank (EXIM) has issued a Preliminary Project Letter and indicative term sheet for up to $2 billion in financing . Final commitment remains subject to completing due diligence and underwriting requirements .

What Are the Stibnite Gold Project Economics?

The project economics remain compelling based on the 2020 Feasibility Study and 2024 Financial Update :

At spot prices of $2,900/oz gold and $21/lb antimony :

- After-Tax NPV (5%): $3.65 billion

- After-Tax IRR: 27.1%

- Payback Period: 2.2 years

The antimony by-product provides a meaningful cost offset of $220/oz gold over the life of mine, contributing to industry-leading AISC .

Why is the Antimony Reserve Strategic?

Perpetua holds the only U.S. reserve of antimony at 148 million pounds . This critical mineral is essential for:

- Military applications (ammunition, night vision)

- Clean energy (solar panels, battery technology)

- Industrial uses (flame retardants, semiconductors)

China and Russia control approximately 65% of global antimony production , and China implemented export controls in 2024. The U.S. government has recognized this strategic importance:

Perpetua has partnered with Idaho National Laboratory to develop a modular antimony pilot plant .

How Did the Stock React?

PPTA shares have surged from $11.05 at the start of 2025 to $30.18 as of February 20, 2026—a gain of 173%:

The stock pulled back 16% from its January peak but remains well above its 52-week low of $7.81 (February 2025).

What Milestones Were Achieved in 2025?

Perpetua achieved critical permitting and financing milestones :

Permitting:

- ✓ Final Record of Decision (January 2025)

- ✓ Final Federal Permit (May 2025)

- ✓ Groundbreaking at Stibnite site (October 2025)

Financing:

- ✓ $527M net equity financing (June & October 2025)

- ✓ EXIM Preliminary Project Letter received (September 2025)

- ✓ $317M strategic investments from Agnico Eagle and JPMorgan (October-December 2025)

Development:

- ✓ Completed basic engineering and 2024 Financial Update (February 2025)

- ✓ Selected Hatch as EPCM contractor (December 2025)

- ✓ Partnership with Idaho National Lab for antimony pilot plant (December 2025)

What's the Path to Production?

Remaining milestones for 2026 and beyond :

Who Owns the Stock?

The shareholder base includes major institutional support :

The capital structure as of February 10, 2026 :

- Issued & Outstanding: 124.5 million shares

- Share Units: 1.7 million

- Warrants: 4.8 million

- Fully Diluted: 131.0 million shares

What Are the Key Risks?

Investors should note several risk factors :

-

EXIM Financing Uncertainty: The LOI and preliminary term sheet are non-binding. Final commitment depends on completing due diligence .

-

Construction Execution: The $2.2B initial capital estimate includes 15% contingency. Cost overruns in mining projects are common .

-

Commodity Price Exposure: Project economics are sensitive to gold and antimony prices. A $100/oz change in gold price significantly impacts NPV .

-

Pre-Revenue Stage: The company continues to burn cash (~$26M in Q3 2025) with no revenue expected until 2029.

-

Permitting/Legal Risk: While major permits are secured, the project could face litigation or permitting challenges .

Key Takeaways

For Bulls:

- $720M cash position with up to $3B total capital available provides runway through construction

- Only U.S. antimony reserve positions the company as a strategic national asset

- All major federal permits secured; EPCM contractor selected

- Industry-leading AISC of $756/oz positions Stibnite as a top-tier gold project

- Strong institutional backing from Paulson, Agnico Eagle, and JPMorgan

For Bears:

- EXIM financing not yet committed; final terms could differ materially

- 3+ years until commercial production with continued cash burn

- Commodity price risk (gold and antimony) affects project economics

- Construction and execution risk on $2.2B capital project

- Stock down 16% from January highs may indicate profit-taking

This analysis is based on the company's 8-K filing dated February 23, 2026, which included an investor presentation with updated financial and project information.