Primoris Services (PRIM)·Q4 2025 Earnings Summary

Primoris Q4 Beat Overshadowed by Margin Pressure — Stock Falls 5% on Renewables Execution

February 24, 2026 · by Fintool AI Agent

Primoris Services Corporation (NYSE: PRIM) delivered a double beat in Q4 2025 but couldn't escape the scrutiny of margin compression. Revenue of $1.86 billion beat consensus by 2.3%, while Adjusted EPS of $1.08 topped estimates by 8.9%. Yet the stock fell 5.3% to $156.87 as investors focused on operating margin declining to 4.2% from 5.0% a year ago.

Full year 2025 was a record year: $7.6 billion in revenue (+19% YoY), $275 million in net income (+52% YoY), and Adjusted EBITDA of $531 million (+22% YoY). But Q4's execution issues in renewables and lower storm restoration work raised questions about 2026 margin sustainability.

Did Primoris Beat Earnings?

Yes — Primoris beat on both revenue and EPS in Q4 2025:

*Values retrieved from S&P Global

This marks 8 consecutive quarters of EPS beats for Primoris, continuing a streak of consistent outperformance against analyst expectations.

Are They Hitting Their Investor Day Targets?

Yes — Primoris exceeded every 2024-2026 target through 2025:

The company is running well ahead of the targets laid out at their 2024 Investor Day, now carrying a net cash position instead of the planned 1.5x leverage.

Meet the New CEO

Koti Vadlamudi took the helm as CEO in late 2025, and this Q4 call marked his first earnings conference call. His commentary emphasized culture, execution discipline, and growth ambitions:

"Primoris is a great company because it has great people that embody a great culture. I have spent much of my time learning from and engaging with our employees, whose efforts are essential to our past and future success."

On his strategic priorities:

"We are focused on the people, equipment, and expertise to help our customers succeed... We remain committed to improving margins, generating cash flow, and being the best allocators of capital in our industry."

Key focus areas under new leadership:

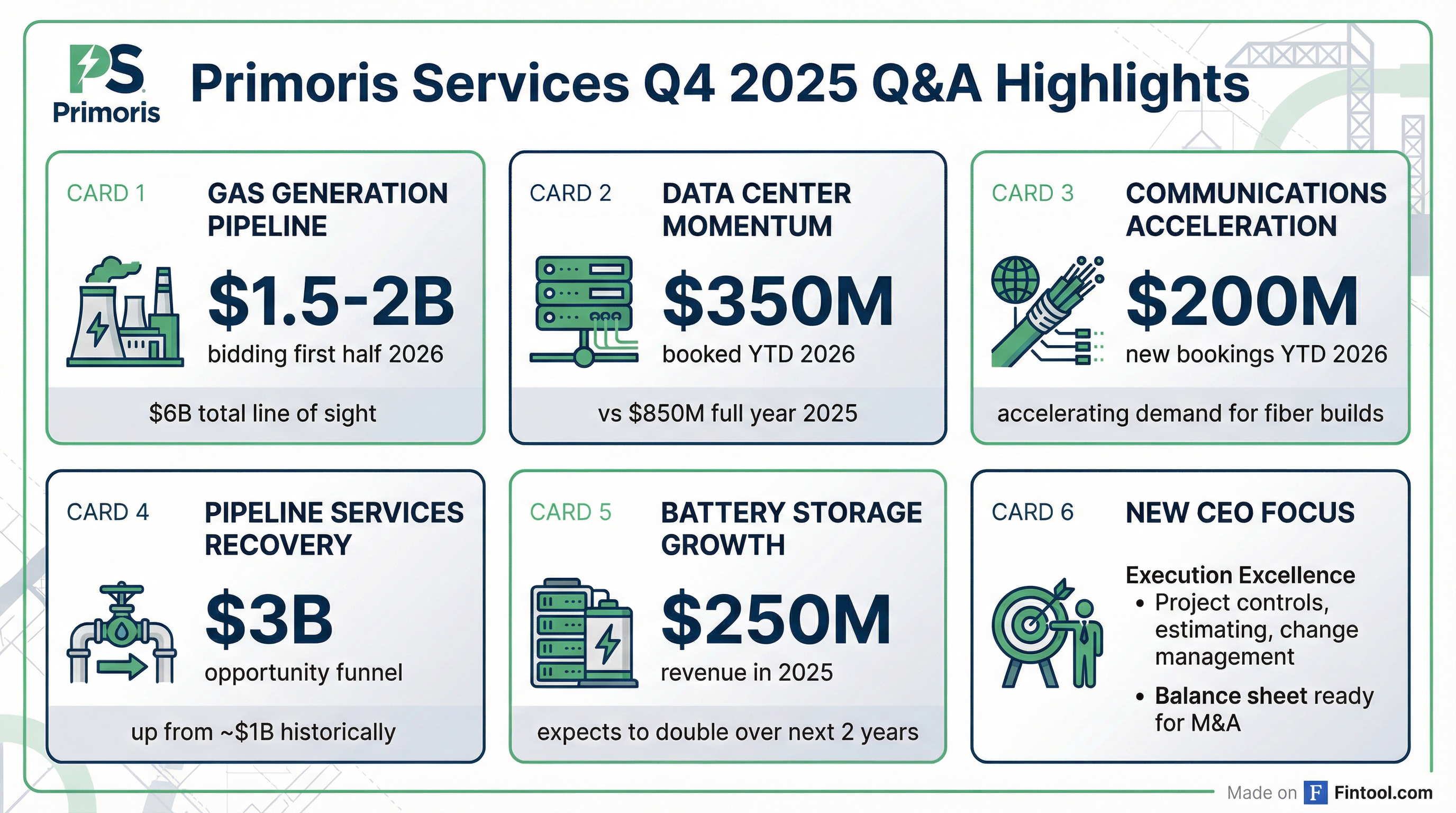

- Execution excellence: Better estimating, project controls, and change management

- Balance sheet deployment: M&A opportunities that align with high-growth, high-margin markets

- Labor investment: Creating "bench" capacity in gas generation and power delivery ahead of demand

What Did Management Say in Q&A?

The Q&A session revealed significant detail on growth opportunities and execution challenges:

Gas Generation Pipeline — $6B Line of Sight

Management disclosed a robust near-term opportunity set:

"The one and a half to $2 billion is notionally first half of the year and would have a meaningful burn in 2026. In the overall funnel, it's probably a little bit more weighted to back half of the year with line of sight to nearly $6 billion."

Projects are primarily simple-cycle gas turbines, with combined-cycle opportunities emerging (including a 1.6 GW plant in early phases). Average project size is "a few hundred million" in services revenue.

Data Center Infrastructure — Accelerating Fast

Data center-related work is ramping sharply:

"Last year, I think we narrated, what was it? $850 million in work related to mainly around enabling infrastructure for data center. Just in the short start of this year, we're at $350 million."

That's 41% of full-year 2025 already booked in early 2026.

Renewables Margin Issues — The Details

Management provided granular detail on the Q4 execution issues:

"A project in an environment where we underappreciated the geotech and soil conditions from an estimate standpoint, mitigation measures we took didn't prove efficacious, then that cascaded with equipment and labor escalation."

CFO Ken Dodgen clarified these were "2 sister projects out of 25 or 30 projects" — one in slight loss position, one still positive margin. The company expects issues "worked off by the end of Q1" with margins improving sequentially through 2026.

Pipeline Services — Funnel Up 3x

The pipeline services business appears poised for recovery:

"Our funnel of opportunities has increased dramatically over the past year to over $3 billion. In recent years, we have seen our funnel trend around one-third of this value."

Pipeline projects "tend to mobilize to the construction phase more quickly" and can complete within the calendar year, suggesting meaningful 2026 contribution if awards materialize.

Communications — $200M Booked YTD

The fiber/communications business is seeing accelerating demand:

"With respect to communications, we're seeing some really good indications at the start of this year with some new wins, $200 million in bookings... The favorable trend in this market appears to be accelerating."

Battery Storage — Doubling Ahead

The BESS business reached $250M+ in 2025 and is capacity-constrained:

"I think over the next couple of years, seeing that the business double in size, I think is within line of sight."

A new facility investment in 2026 will expand Premier PV capacity by Q4 2026, enabling further growth in 2027.

What Changed From Last Quarter?

Q4 2025 showed deceleration from a strong Q3:

*Values retrieved from S&P Global

Key drivers of Q4 weakness:

- Renewables cost overruns: Challenging soil conditions on certain renewables projects increased costs more than anticipated

- Storm work decline: Lower storm restoration activity in power delivery vs. prior year

- Seasonality: Q4 is typically a softer quarter, though still grew 6.7% YoY

What Did Management Say About Margins?

CEO Koti Vadlamudi addressed the Q4 execution issues directly in the Q&A:

"We highlighted the performance execution... in the renewable segment. There are some other areas that I would say would fall in the basket of efficiency gain in, through project execution, and that gets down to better estimating, better project controls, better change management. These are particular levers that will help drive a better growth, project growth margin and ultimately better predictable execution."

On the specific project issues:

"We literally ran into more rock than we've ever seen on any project we've ever executed. It's a very unusual situation. The sister projects, one is actually in a slight loss position, the other one is still positive margin." — CFO Ken Dodgen

2026 Margin Targets (from guidance):

- Utilities segment: 10-12% gross margin (Q1: 7-9% due to seasonality)

- Energy segment: 10-12% gross margin (Q1: bottom end as problem projects burn off)

- SG&A as % of revenue: Mid-to-high 5% range

What Did Management Guide?

FY 2026 Guidance:

Other 2026 Expectations:

- Interest expense: $23-$26 million (down from $28.7M in 2025)

- Effective tax rate: ~29%

- Capital expenditures: $120-$140 million

The guidance implies continued growth but at a more modest pace than 2025's exceptional performance.

How Did the Stock React?

PRIM fell 5.3% on Feb 24, 2026 despite the double beat:

The stock opened down sharply at $139.16 (-16% from prior close) before recovering throughout the day. The initial selloff likely reflected:

- Margin compression concerns — Operating margin down 80 bps YoY, gross margin down 120 bps

- Conservative guidance — Adjusted EPS growth of only 3-7% in 2026 after 46% growth in 2025

- Renewables execution questions — Project-level cost overruns on sister projects

The intraday recovery suggests investors digested the Q&A details positively, particularly the $6B gas generation pipeline and accelerating data center momentum. PRIM remains up 219% from its 52-week low, reflecting infrastructure buildout tailwinds.

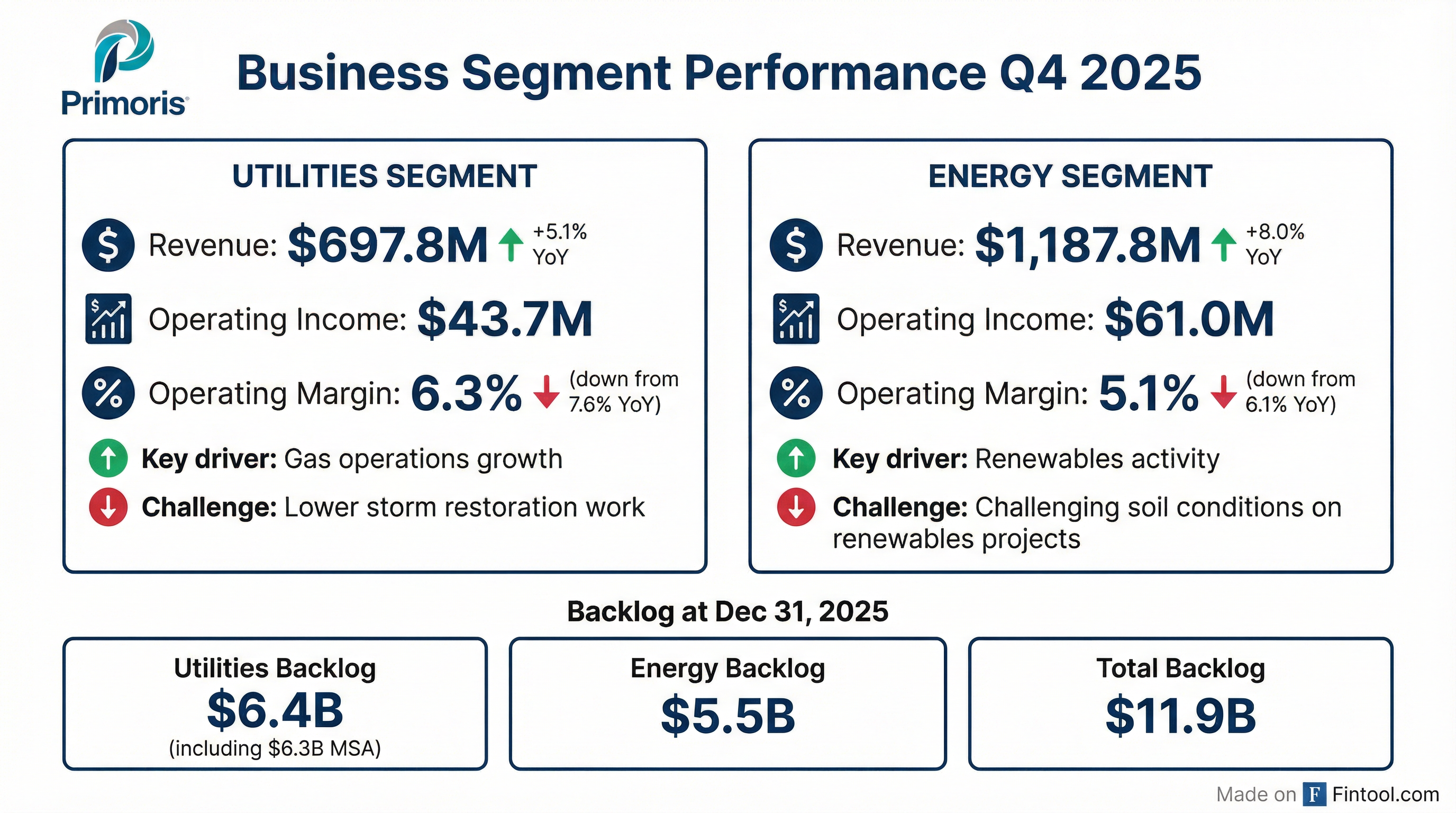

Segment Deep Dive

Utilities Segment

Full Year 2025: Revenue of $2.69B (+10.4% YoY), gross margin of 11.5% vs 10.6% prior year, operating margin improved to 6.8% from 5.7%

Key Drivers: Gas operations and power delivery growth, offset by lower storm restoration work in Q4

Energy Segment

Full Year 2025: Revenue of $5.02B (+24.5% YoY), gross margin of 10.1% vs 11.0% prior year, operating margin held at 6.8%

Key Drivers: Renewables activity grew, but soil condition challenges on certain projects increased costs

Notable: Renewables revenue exceeded $3 billion for full year 2025, including over $250 million from battery storage projects

MSA Revenue and Operating Leverage

Master Service Agreements (MSAs) drive revenue predictability:

Key insights:

- MSA revenue grew 71% from 2019-2025, now ~$7 billion in total MSA backlog

- SG&A efficiency improved 80 bps vs 2024, demonstrating operating leverage at scale

- 2026 guidance targets mid-to-high 5% SG&A

Balance Sheet & Capital Allocation

Strong liquidity position:

Capital Allocation:

- Dividend: $0.08/share quarterly (declared Feb 17, 2026)

- Share repurchases: $150M authorized, none executed in 2025

- Capex 2025: $129.9M ($75.8M equipment, $35.3M facilities)

Forward Catalysts

Upside Drivers:

- Gas generation awards — $1.5-2B bidding first half 2026, $6B total line of sight

- Data center infrastructure — $350M booked YTD vs $850M full year 2025, accelerating fast

- Pipeline services recovery — Funnel up 3x to $3B, quick book-to-burn profile

- Battery storage capacity expansion — New facility Q4 2026, expects business to double

- Communications acceleration — $200M booked YTD, "favorable trend accelerating"

Downside Risks:

- Renewables execution risk — Soil/geotech conditions can drive cost overruns on large projects

- Labor constraints — Certified journeymen linemen in tight supply

- Award timing lumpiness — Large projects can slip quarters, creating volatile book-to-bill

- Gas generation project size — Multi-hundred million dollar scope increases execution risk

- Storm work variability — Contributed ~$12M EBITDA in 2025, not included in 2026 guidance

Key Takeaways

- Double beat, margin concerns — Revenue +2.3% and EPS +8.9% vs consensus, but gross margin down 120 bps YoY to 9.4%

- New CEO, same playbook — Koti Vadlamudi emphasizing execution discipline, project controls, and cultural fit

- $6B gas generation pipeline — $1.5-2B near-term awards possible, meaningful burn in 2026

- Data center acceleration — $350M booked in early 2026 vs $850M full year 2025, Texas particularly active

- Renewables issues specific, not systemic — 2 sister projects out of 25-30, should clear by Q1

- Strong balance sheet, M&A ready — Net cash position, discipline on targets with "high sustainable growth trajectory"

Data sourced from Primoris Q4 2025 earnings release (8-K, Feb 23, 2026), earnings presentation slides (Feb 24, 2026), and Q4 2025 earnings call transcript (Feb 24, 2026).