RBC Bearings (RBC)·Q3 2026 Earnings Summary

RBC Bearings Beats EPS as Aerospace Surges 42%, Stock Rallies 6%

February 5, 2026 · by Fintool AI Agent

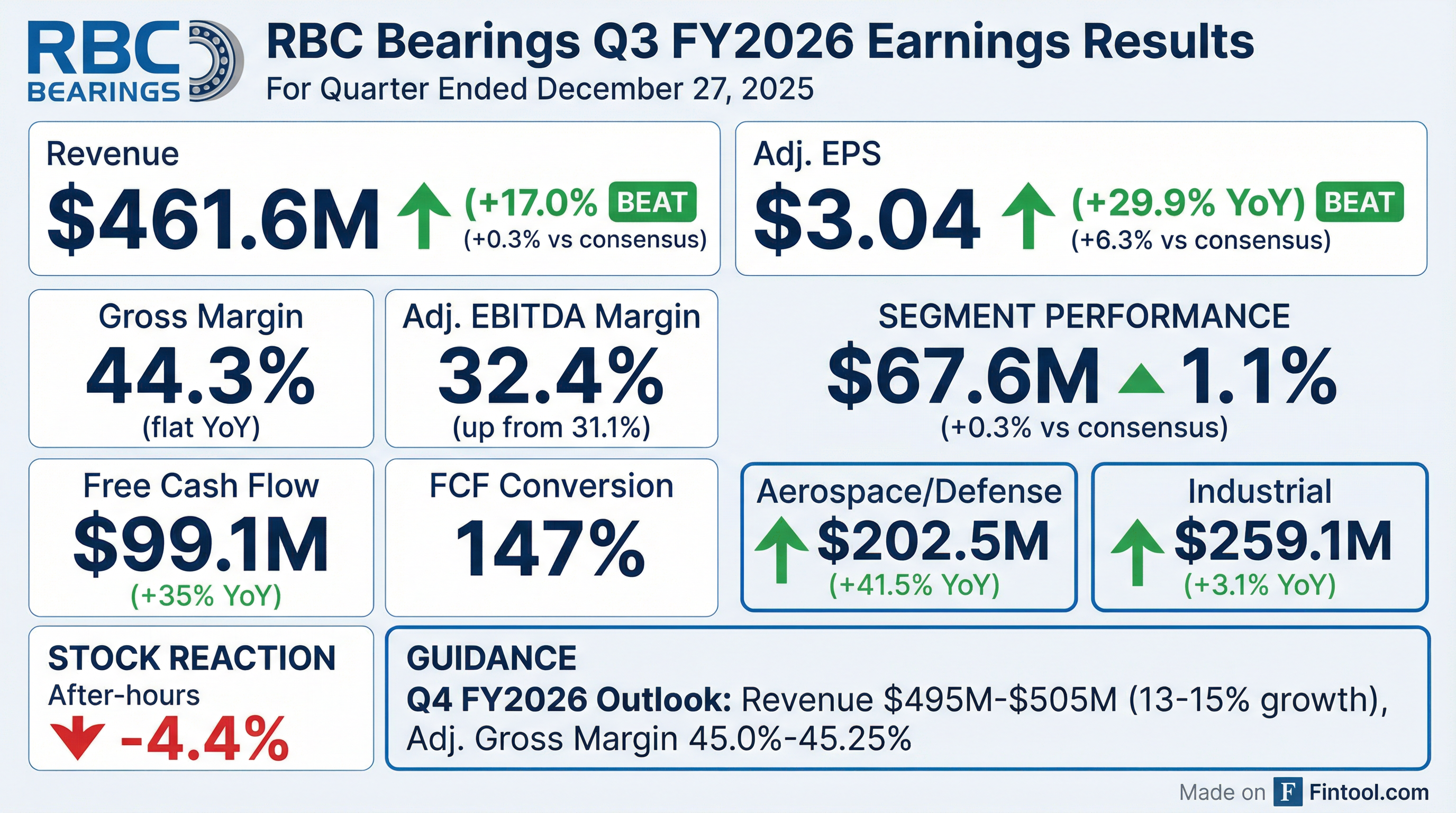

RBC Bearings (NYSE: RBC) posted a strong Q3 FY2026 with adjusted EPS of $3.04, beating consensus by 6.3%, while revenue of $461.6 million came in essentially in-line with the $460.4M estimate . The precision bearings manufacturer saw its Aerospace/Defense segment surge 41.5% YoY, driven by robust defense demand and the VACCO acquisition . Industrial grew a more modest 3.1% but management signaled improving trends into calendar 2026 . Shares rallied 6% to new highs on the earnings beat and bullish outlook.

Did RBC Bearings Beat Earnings?

Revenue and EPS estimates from S&P Global. Actuals from company filings .

RBC delivered its 9th consecutive quarter of EPS beats. The VACCO acquisition (closed July 2025) contributed $29.2 million to net sales this quarter .

What Is Driving the Aerospace/Defense Surge?

The standout story is A&D, which now represents 44% of revenue vs. 36% a year ago:

Source: Company filings

The A&D growth reflects:

- VACCO acquisition (July 2025): Added $29.2M in Q3 sales

- Organic A&D growth: ~20%+ excluding VACCO

- Defense contract wins: Driving backlog expansion

Backlog exploded to $2.1 billion as of December 27, 2025—up from $1.6B in September and just $0.9B a year ago, a 133% YoY increase .

What Did Management Guide?

*Source: Company outlook *

Excluding VACCO, organic revenue growth is guided at 6.4% to 8.7% for Q4 .

CEO Dr. Michael J. Hartnett commented:

"We are well-positioned for growth in calendar year 2026 and beyond, given our robust, growing backlog, which has continued to benefit from recent contract wins within the A&D space."

What Changed From Last Quarter?

The sequential improvement in free cash flow (+38% QoQ) and accelerating backlog (+31% QoQ) are notable. FCF conversion hit 147% vs. 127% a year ago .

How Did the Stock React?

Shares rallied on the earnings beat, touching intraday highs of $528.74. The positive reaction reflects:

- EPS beat: $3.04 vs. $2.86 expected (+6.3%)

- Record backlog: $2.1B with defense contract momentum

- Improving industrial outlook: Management bullish on calendar 2026

- Conservative guidance: Management signaled Q4 guide is conservative

Margins and Capital Allocation

*Source: Company filings *

Cash Flow & Balance Sheet:

Source: Company filings

The company is investing in capacity expansion while maintaining strong FCF. Debt reduction efforts lowered interest expense to $13M from $14.2M YoY .

Q&A Highlights: What Did Analysts Ask?

Defense Program Exposure:

Dr. Hartnett provided extensive color on defense end markets :

- Submarines: "Number one defense priority today" — 66 Virginia-class ships planned (25 commissioned), 12 Columbia-class ships planned

- Missiles: Exposure across HIMARS, JDAMs, and hypersonics; hypersonics will go on Columbia-class and Virginia-class submarines

- Europe: NATO's 5% GDP initiative driving demand from European ground warfare system builders

"Today, the strength and outlook on the A&D sector can only be described as extremely robust. Clearly, we are at a national inflection point in the commercial aircraft and defense industries."

Boeing/Airbus Production Rates:

Management detailed OEM production expectations :

- 737: At 38/month → 42 → 50, with objective of 60

- 787: 6/month → 8/month (significant for one RBC plant)

- 777X: "Coming into its own" but only a few ships/month in distant future

- Airbus: New contract adds ~20% content increase, starting this quarter

One smaller plant has Boeing working off inventory until July; all others are lockstep with Boeing production .

Industrial Outlook:

On FY2027 industrial expectations :

- Expecting "high single digits" growth vs. peers guiding "low single digits"

- Semiconductor came back "in a significant way" after being "dormant for a long period"

- Broad industrial demand strengthened "measurably in late December and continued throughout January"

- Opening new service center in Midwest to serve more customers

Space Opportunity:

VACCO has a satellite staples business with potential to "guide the industry" by stocking key components . Sargent Aerospace products are specifically for submarines, while VACCO has both submarine and space applications .

Margin Outlook:

A&D margins (42.2% adjusted in Q3) should continue to "chase up towards industrial margins" (47.4% adjusted), though management doesn't expect them to fully converge .

Key Risks and Concerns

- Industrial segment deceleration: Only +3.1% growth suggests macro softness in traditional industrial end markets

- Acquisition integration: VACCO adds revenue but also integration complexity

- Valuation: Trading near all-time highs with elevated multiples

- Defense budget dependency: Growing A&D concentration increases exposure to government spending

Forward Catalysts

- Q4 FY2026 earnings (expected late May 2026): Full-year results and FY2027 outlook

- VACCO integration milestones: Synergy realization updates

- Defense contract awards: Backlog momentum continuation

- Industrial recovery: OEM destocking completion could reaccelerate growth

Earnings call held February 5, 2026. View full transcript | View 8-K filing

Related: RBC Bearings Company Profile | Q2 FY2026 Earnings