UNITED MICROELECTRONICS (UMC)·Q4 2025 Earnings Summary

UMC Surges 10% as 22nm Growth and EPS Beat Drive Strong Q4 Results

January 28, 2026 · by Fintool AI Agent

United Microelectronics Corporation (UMC) delivered a strong Q4 2025, beating both revenue and EPS estimates as its 22-nanometer platform hit record revenue. The stock surged over 10% during the session before giving back gains in after-hours trading. Management struck an optimistic tone, citing improving pricing dynamics and positioning advanced packaging and silicon photonics as key growth catalysts for 2026 and beyond.

Did UMC Beat Earnings?

Yes — UMC beat on both revenue and EPS.

*Values retrieved from S&P Global

Revenue grew 4.5% quarter-over-quarter to TWD 61.81 billion ($1.94B), supported by favorable foreign exchange movements and sequential growth in 22nm and 28nm segments.

The substantial EPS beat was driven by strong gross margin improvement to 30.7% (up from high 20s in prior quarters) and continued product mix optimization toward higher-margin specialty technologies.

Historical Beat/Miss Trend

*Values retrieved from S&P Global

UMC has delivered consecutive beats in the last three quarters, signaling improving execution as the semiconductor cycle recovers.

How Did the Stock React?

UMC shares surged +10.2% to $12.48 during the regular session on strong volume of 26.9 million shares. However, the stock retreated to $11.17 in after-hours trading, giving back a significant portion of the day's gains — potentially reflecting investor caution around Q1 guidance showing sequential margin compression.

The stock is now trading at its 52-week high of $12.68 (touched intraday), up substantially from the 52-week low of $5.66. Year-to-date, UMC is up over 50% as investors price in the mature foundry supply tightening narrative.

What Did Management Guide?

Q1 2026 Guidance:

Management's gross margin guidance of "high 20% range" implies sequential compression from Q4's 30.7%, attributed to higher depreciation expenses (expected to grow "low teens" YoY) and seasonal headwinds.

Full Year 2026 Outlook:

- CapEx budget: $1.5 billion (down from $1.6B in 2025)

- Capacity growth: +1.2% YoY

- Second half expected to outperform first half — deviating from traditional seasonality

- Addressable market expected to grow "low single-digit %" with UMC expected to outperform

What Changed From Last Quarter?

Pricing Environment Improving

This was the most significant development. President Jason Wang stated: "We anticipate a more favorable ASP environment in 2026 versus 2025. This outlook reflects our disciplined pricing strategy and the positive impact from product mix optimization, loading improvement, and reduced exposure to more commoditized market segments."

While some customers received one-time price adjustments downward to support their market share expansion, net-net the pricing environment is "more favorable now." When pressed on whether conditions had changed since initial negotiations, management confirmed: "The condition has started to change now... the pricing discussion will be more favorable now."

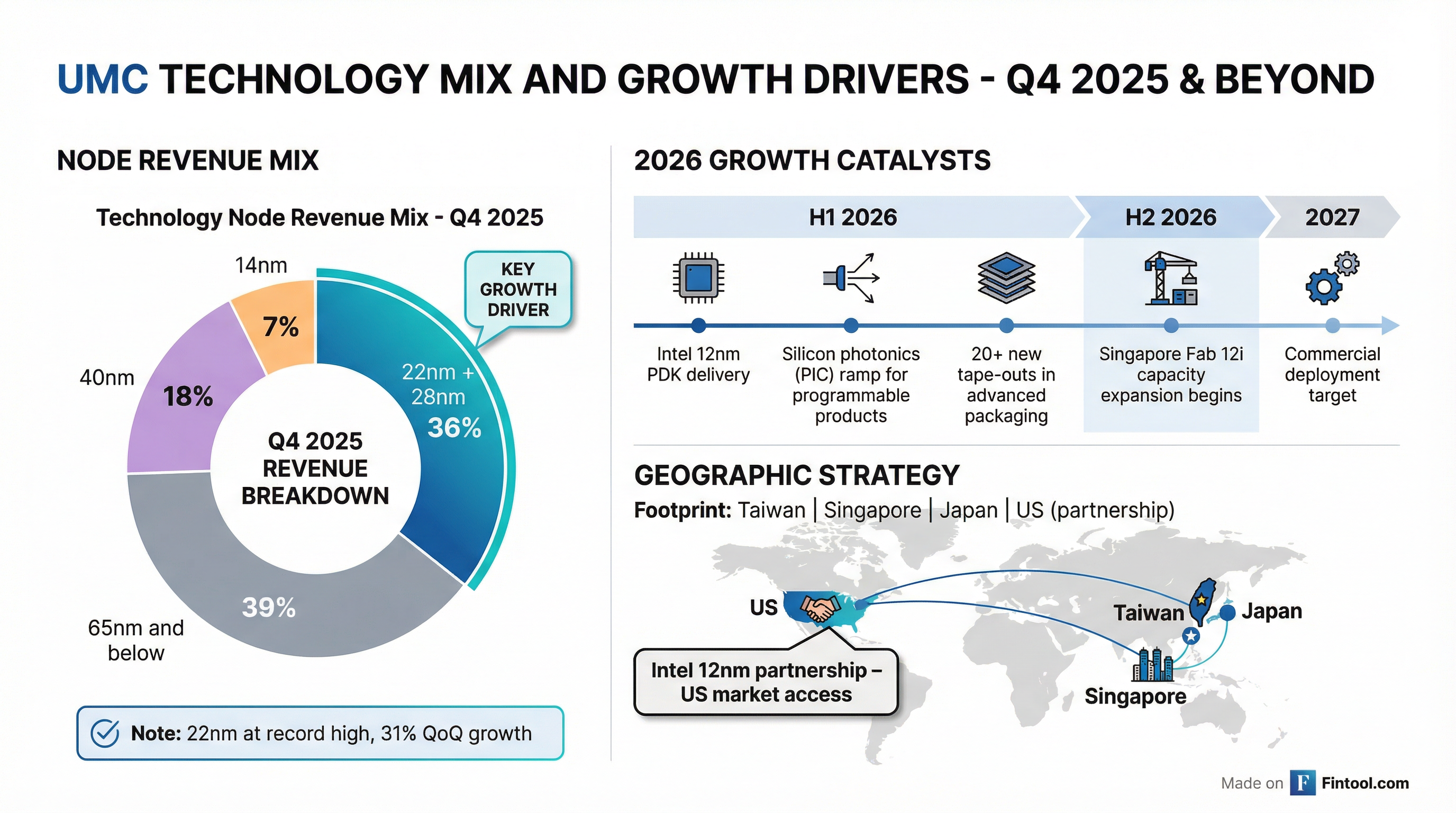

22nm Revenue at Record High

22-nanometer revenue increased 31% quarter-over-quarter to a record high, now accounting for over 13% of total Q4 revenue. Combined with 28nm, these advanced nodes now represent 36% of total revenue — up 3 percentage points year-over-year.

Structural Supply Tightening

Management described the current supply situation as potentially "more structural" than COVID-era shortages: "Building any mature facility is not justifiable... This situation could last longer compared to the COVID time." The AI demand ripple effect is causing capacity reallocation industry-wide, benefiting mature foundries like UMC.

Key Growth Catalysts for 2026-2027

Intel 12nm Partnership

The collaboration "continues to advance smoothly" with PDK and IP delivery to customers expected in 2026, and product tape-outs commencing in 2027. Applications include digital TV, Wi-Fi connectivity, and high-speed interface products.

When asked about expanding to 7nm, management stayed focused: "Our focus right now is on delivering the 12-nanometer platform... anything that makes sense from there on, there will be a discussion."

Advanced Packaging

UMC positioned advanced packaging as both an "enabler" and "tent expander":

- Enabler: 2.5D/3D packaging spreading beyond data center to mobile (already shipping RF-SOI with wafer-to-wafer hybrid bonding)

- Tent Expander: Addressing AI applications by stacking memory with logic, adding DTC, enabling total solutions

Key metrics: Working with 10+ customers, expecting 20+ new tape-outs in 2026, with 2027 revenue expected to be significant. When asked if that could mean 5-10% of revenue, CFO responded: "I'm expecting half more than that."

Silicon Photonics

UMC is developing solutions including PIC, OIO, OCS, and CPO through collaboration with imec. The strategy centers on 12-inch manufacturing (vs. competitors at 8-inch), with an industry-standard PDK expected in 2027. A programmable product is expected to ramp this year.

Segment Performance

By Application (Q4 2025)

By Geography (Q4 2025)

North America declined from 25% of revenue in 2024 to 21% in Q4 2025, while Asia and Europe gained share.

Specialty Technology

Specialty technologies (high voltage, non-volatile memory, BCD) represent approximately 50% of revenue, with high voltage alone at ~30%.

Memory Cost Inflation Impact

Analysts pressed on whether rising memory prices could hurt consumer electronics demand. Management's response was reassuring: "As of today, we have not observed any demand impact on our customer's forecast for the year... Our technology predominantly supports customers addressing the higher end of the market segment, where demand tends to be more resilient."

Capital Allocation & Margins

Depreciation Headwind

Depreciation is expected to grow "low teens" annually in 2026, with similar growth expected in 2027. The depreciation curve is expected to peak in 2026 or 2027.

EBITDA Stability

Despite gross margin pressure, management emphasized that EBITDA margin improved in 2025 vs 2024 and they're targeting stable EBITDA margins going forward through cost reduction and productivity efforts.

Xiamen Fab Strategy

Unlike some Taiwan peers exiting mainland China, UMC's Xiamen fab is running at full utilization and remains a core part of their geographic diversification strategy.

Q&A Highlights

On pricing flexibility: "The core of the pricing strategy is that it has to be consistent, and it has to anchor with the value that we deliver... If the condition has changed, yes, there will be some flexibility."

On advanced packaging timeline: "We are making deliberate choices, working with imec to invest and to scale them into a significant driver for our future."

On supply-demand dynamics: "We see that AI demand will continue driving the overall demand... and from an economic standpoint, building any mature facility is not justifiable."

What to Watch Going Forward

- Q1 2026 gross margin — Will it hold the high 20s or compress further?

- Pricing negotiations — Can UMC capitalize on tightening supply through 2026?

- Advanced packaging tape-outs — 20+ expected in 2026, revenue impact in 2027

- Intel 12nm milestones — 2027 tape-out remains on track

- Singapore expansion — H2 2026 ramp, continuing into 2027

- Memory pricing impact — Monitoring consumer segment demand

Analysis based on UMC Q4 2025 earnings call held January 28, 2026. View full transcript.