WESTLAKE (WLK)·Q4 2025 Earnings Summary

Westlake Q4 2025: Stock Surges 12% as $600M Self-Help Plan Wins Over Investors

February 24, 2026 · by Fintool AI Agent

Westlake Corporation (WLK) stock surged 11.8% to $104.02 following Q4 2025 results, despite reporting a net loss of $0.25 per share and adjusted EBITDA of $196M — down 53% year-over-year . The rally reflects investor confidence in management's three-pillar $600M EBITDA improvement plan for 2026 , early signs of demand recovery with January ISM hitting 53 (first expansion in a year) , and China's removal of VAT export rebates lifting global PVC prices . CFO Steve Bender also announced his retirement after 21 years .

Did Westlake Beat Earnings?

No — Westlake missed across all key metrics in Q4 2025.

Full-year 2025 results were equally weak:

- FY25 Revenue: $11.17B, down 8% YoY

- FY25 EBITDA: $1.14B, down 50% YoY

- FY25 EPS (adj.): -$0.90 vs $5.22 in FY24

What Drove the Miss?

Global overcapacity and price declines were the primary culprits :

- Lower average selling prices: Down 3.3% QoQ and 3.6% YoY across the company

- Volume declines: Down 7.5% QoQ and 7.3% YoY

- Higher feedstock/energy costs: Contributed to margin compression, particularly in PEM

- Planned turnarounds and unplanned outages: Elevated level in FY25 not expected to recur

How Did Each Segment Perform?

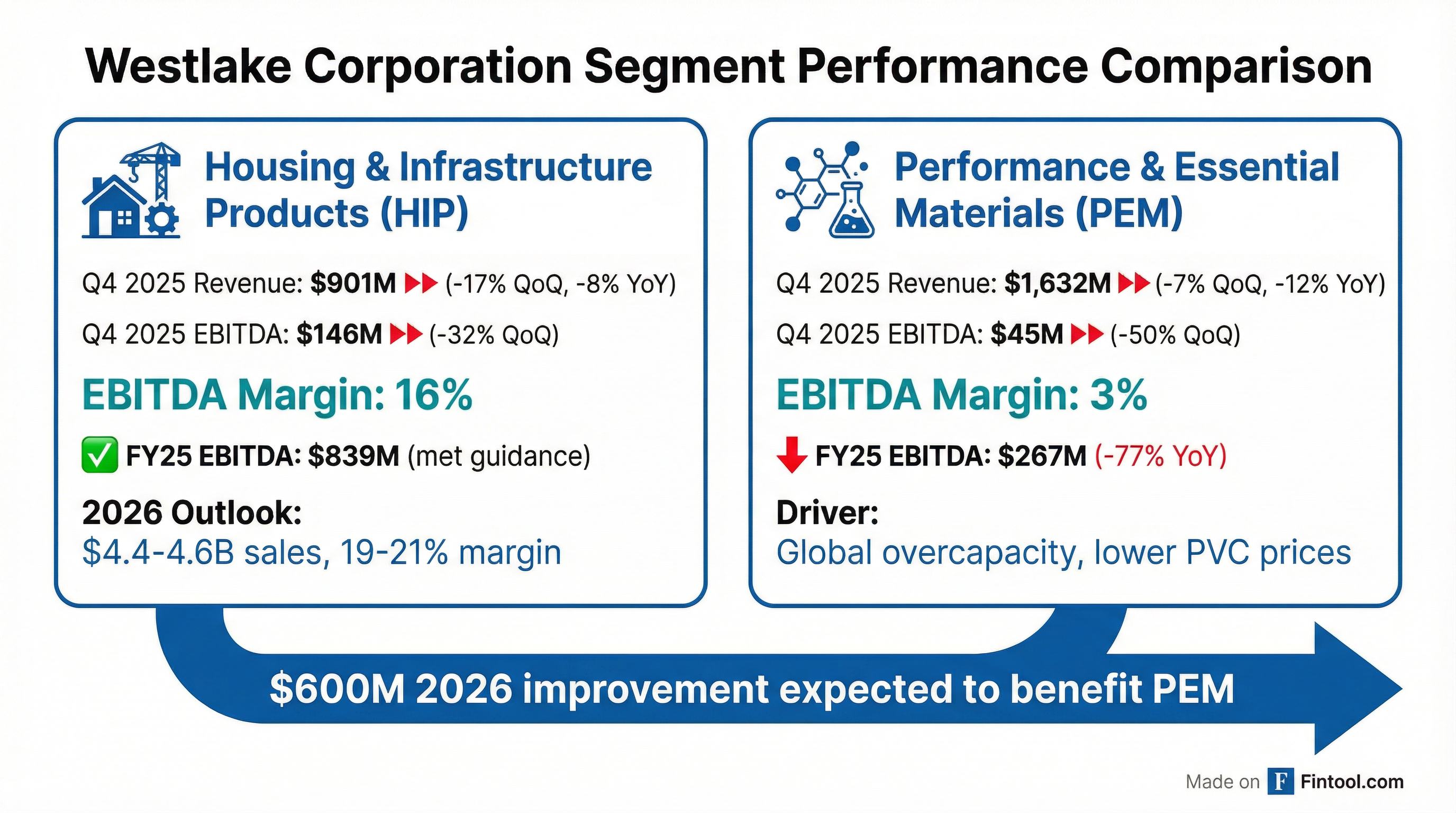

Housing and Infrastructure Products (HIP)

The more resilient segment, though still pressured by softer residential construction:

FY25 HIP EBITDA of $839M met guidance , driven by continued strong demand for pipe and fittings from North America infrastructure spending. Management expects FY26 HIP sales of $4.4-4.6B with 19-21% EBITDA margins .

Performance and Essential Materials (PEM)

The struggling segment bore the brunt of global chemical overcapacity:

Lower PVC resin and polyethylene prices drove the margin collapse . Management noted the vast majority of the $600M 2026 improvement is expected to benefit PEM .

What Is the $600M Profitability Improvement Plan?

Management outlined a three-pillar approach expected to deliver approximately $600M in EBITDA improvement in 2026 :

This is purely "self-help" — not dependent on pricing improvement or demand recovery .

How Did the Stock React?

WLK surged 11.8% to $104.02 on the earnings call — one of the strongest post-earnings moves in the materials sector. The stock has nearly doubled from its 52-week low of $56.33, signaling investors are pricing in a 2026 turnaround.

Key context:

- Stock up 24.8% vs 50-day moving average ($83.37)

- Up 31.9% vs 200-day moving average ($78.86)

- Down 9% from 52-week high of $114.75

- Market cap: $13.3B

What Changed From Last Quarter?

The Q4 decline reflects typical seasonal weakness in building products combined with continued pricing pressure in chemicals. The company did achieve its raised $170M cost savings target for FY25 .

What's the Balance Sheet Position?

Westlake maintains a solid financial position:

- Cash and securities: $2.9B

- Investment-grade credit rating maintained

- Free cash flow: -$16M in Q4, -$530M FY25 (vs +$306M FY24)

The negative free cash flow reflects elevated capex for growth projects including a new PVCO pipe plant to support infrastructure demand .

What Did Management Guide For 2026?

Explicit guidance provided:

Additional 2026 guidance details:

- Effective tax rate: ~17% (benefit from NOLs generated in 2025)

- Cash interest expense: ~$215M

- CapEx: ~$900M, down $100M YoY (aligned with depreciation)

Q&A Highlights

Key themes from the analyst Q&A session:

Pricing Outlook

PVC: Management noted restocking activity driving price traction, with price increases announced for January and February. However, they cautioned visibility remains limited to "several months" .

Caustic Soda: Two price increases announced totaling $140/ton ($75 in December + $65 in January). Management expects "some traction" on these increases as industrial/manufacturing demand improves .

Polyethylene: $0.05 price increase realized in January, offsetting December's reset. Additional $0.05 increase announced for February .

China VAT Rebate Removal

A major tailwind discussed: China is removing its 13% VAT export rebate effective April 1st . Management noted:

"Export prices in PVC have already begun to rise because of the expectation that the duty drawback will not be available... I think it's an indication by the authorities there in China that they really need to find actions to rationalize some of those exports that are being disruptive to the market." — CFO Steve Bender

$600M Plan Timing

Asked how the $600M improvement flows through quarters, management indicated benefits will accrue ratably through 2026 :

- Footprint optimization: Full benefit starting in 2026 (plants shuttered in late 2025)

- Cost savings: Building on $170M achieved in 2025

- Reliability: Fewer planned turnarounds vs elevated 2024-2025 levels

Free Cash Flow

When asked directly about FCF expectations, CFO Bender declined to give explicit guidance but emphasized: "Generating free cash flow is critically important to our stakeholders, and that is always a strong objective."

ACI Acquisition

The ACI acquisition closed in January 2026 and will contribute for the full year. It expands Westlake's compound portfolio into silicone and cross-linked polyethylene beyond just PVC .

Portfolio Strategy

Asked whether Westlake might divest polyethylene given persistent oversupply, management pushed back:

"Our focus remains very much value-oriented... If that takes us into PEM or into HIP, and we see that opportunity, that's where the funds will be deployed. Given where we are in the various business cycles, I would say the predominance of the opportunities near term would probably be in HIP." — CFO Steve Bender

CFO Retirement Announcement

Steve Bender, who has served as CFO since 2005, announced plans to retire later in 2026 . CEO Jean-Marc Gilson praised his contributions:

"We are tremendously grateful for the countless contributions that Steve has made to the company over the years. He joined Westlake in 2005, not long after the company's 2004 initial public offering, and he has been instrumental to the significant growth the company has enjoyed since then."

Bender will remain through the transition to a new CFO. The search is underway.

What Are the Key Risks?

Management acknowledged several risks in forward-looking statements :

- Cyclical industry exposure — Chemical and building products demand tied to economic cycles

- Global overcapacity — Continued pressure on PVC and polyethylene prices

- Raw material/energy volatility — Feedstock cost fluctuations impact margins

- Execution risk — $600M improvement plan requires successful facility shutdowns and cost reductions

- Housing market dependence — Residential construction slowdown impacts HIP segment

Key Takeaways

- Stock surging on forward outlook — 11.8% rally reflects confidence in $600M self-help plan, not Q4 results

- China VAT rebate removal is a tailwind — 13% export rebate ending April 1st already lifting global PVC prices

- Pricing momentum building — $140/ton in caustic soda increases, PE price hikes being realized

- ISM expansion first time in a year — January reading of 53 signals potential manufacturing recovery

- CFO transition underway — Steve Bender retiring after 21 years; search for replacement ongoing

- HIP guidance intact — $4.4-4.6B revenue, 19-21% margins expected in 2026