Agnico Eagle CEO Unveils Path to 4M Oz Production at BMO Conference as Gold Tops $5,000

February 23, 2026 · by Fintool Agent

Agnico Eagle Mines CEO Ammar Al-Joundi took the stage at BMO's 35th Global Metals, Mining & Critical Minerals Conference in Hollywood, Florida on Sunday with a message for investors: the world's second-largest gold producer is just getting started.

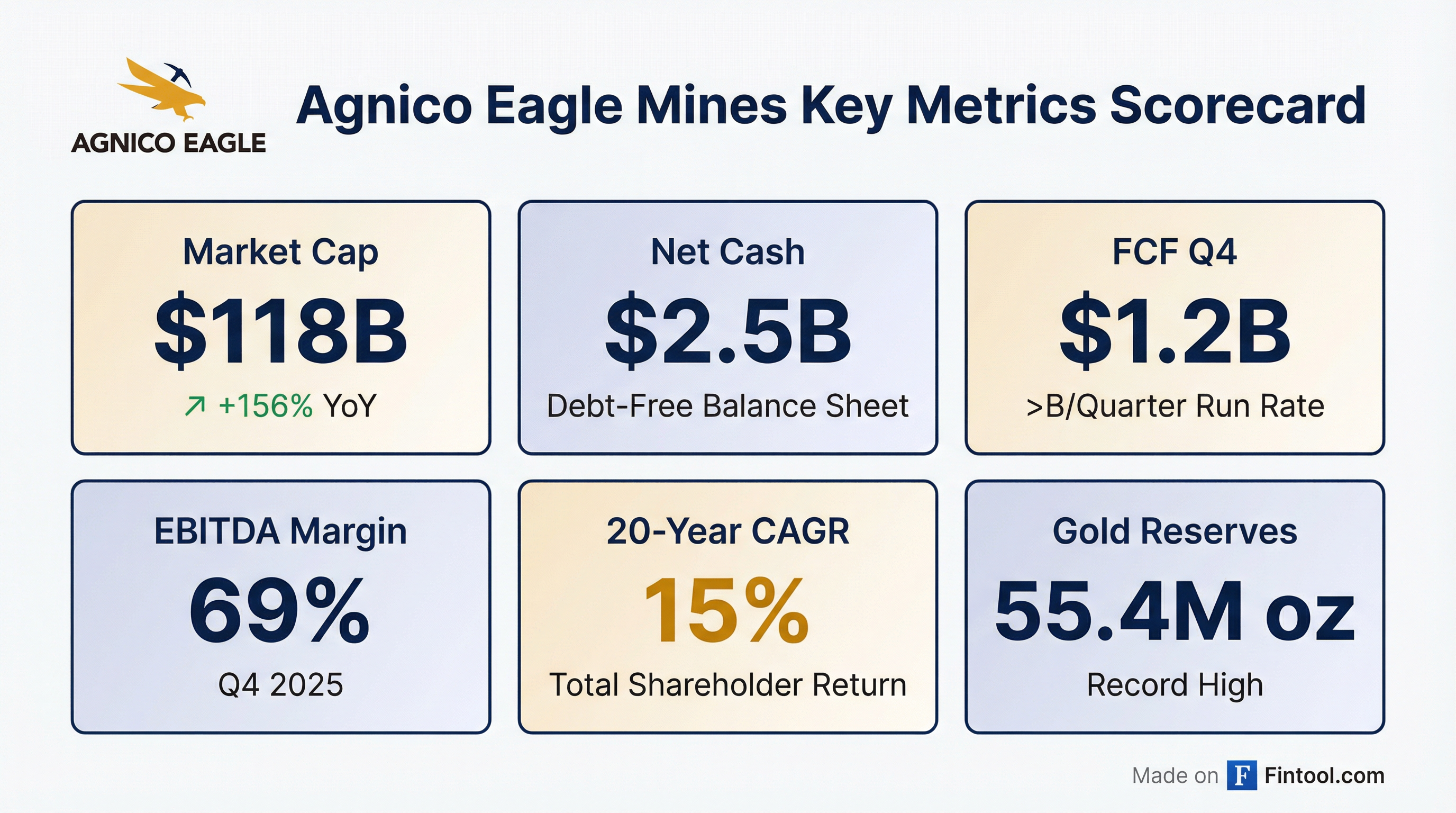

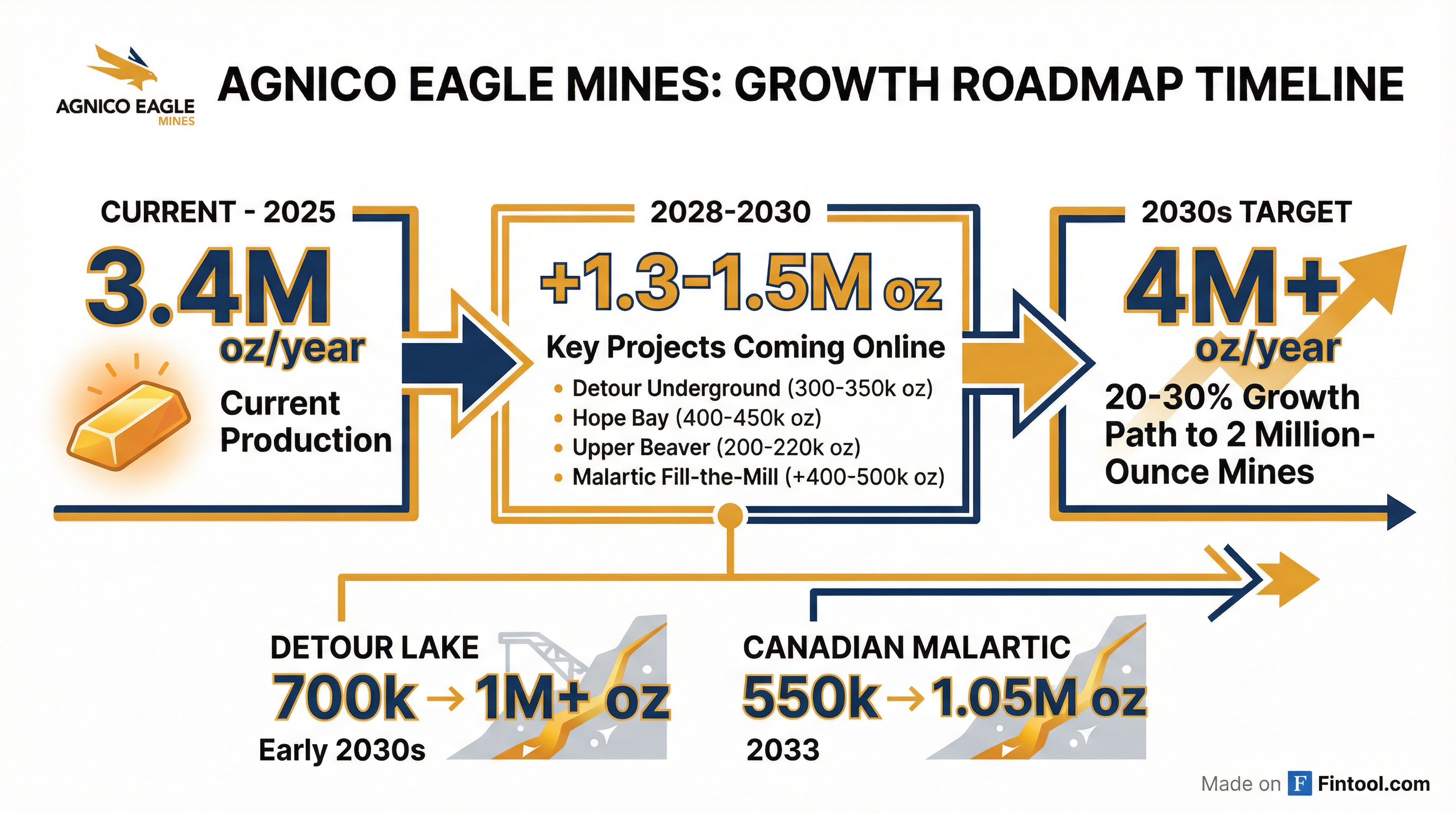

With gold trading above $5,000 per ounce—a price level unthinkable just two years ago—and Agnico's stock hitting all-time highs, Al-Joundi outlined a decade-long growth plan that would see annual production rise 20-30% to over 4 million ounces by the early 2030s . The company's flagship mines at Detour Lake and Canadian Malartic are each on track to become million-ounce producers, joining an elite club of just six such mines globally—and only three in the Western world .

Agnico shares surged 3.5% to $236.27 on the session, hitting a new 52-week high of $238.73. The stock has more than doubled over the past year, rising 156% from its 52-week low of $92.11 .

"The Best Job in Canada"

Al-Joundi, who described his role as "the best job in Canada," opened his presentation with characteristic confidence—and a touch of Canadian hockey humor following the men's team's loss to the United States .

But the message was serious: Agnico's regional strategy, which the company has followed for 70 years, has delivered a 15% compounded annual return over the past two decades, outperforming both the S&P 500 and the gold index .

"We do not consider ourselves a global gold mining company. We consider ourselves a regional gold mining company," Al-Joundi explained. "When you have 15,000 people in your company, what makes you a better miner than the next person? In the areas we operate, where we've been operating for decades, we literally know every single junior... we have third-generation workers at our mines."

The strategy has paid off handsomely. In the last 20 years, Agnico has grown production by a factor of 14, and more importantly for shareholders, production per share by nearly 3x .

The Growth Pipeline: Five Projects, $5-6 Billion

The real excitement, according to Al-Joundi, lies in Agnico's growth pipeline. The company is advancing five major projects that together could add 1.3-1.5 million ounces of annual production :

Detour Lake: Canada's Biggest Gold Mine Gets Bigger

Detour Lake, already Canada's largest gold mine, is set to grow from approximately 700,000 ounces per year to over 1 million ounces by the early 2030s . The transformation involves adding an underground operation that will displace lower-grade open pit ore with 2.5 gram per ton underground material.

In the past five years, Agnico has added 27 million ounces at Detour—"a net increase of 27 million ounces in the largest mine in Canada, that's already built, already has a workforce, has green electricity," Al-Joundi noted .

The company is tripling its investment at Detour Underground from $100 million to $300 million as it accelerates toward a go-ahead decision in mid-2027 .

Canadian Malartic: The Fill-the-Mill Strategy

The second-largest gold mine in Canada will grow from 550,000 ounces to over 1.05 million ounces per year by 2033 . The "fill-the-mill" strategy involves transitioning the 60,000 ton-per-day mill from depleting open pit ore to higher-grade underground production from East Gouldie, plus additional feed from the Marban open pit and Wasamac underground operations.

Agnico has added 22 million ounces at Malartic over the past 7-8 years, with the ramp and first shaft ahead of schedule .

Hope Bay: The May Decision

Perhaps the most anticipated catalyst is the Hope Bay project in Nunavut, where Agnico is targeting a go-ahead announcement in May 2026 . The project is expected to produce 400-450,000 ounces per year with approximately $2 billion in capital expenditure .

"We're gonna announce a go-ahead in May," Al-Joundi confirmed. "When we announce Hope Bay, Dominic and his team will already have over 50% engineering done... It's not our first barbecue in Nunavut."

If approved, Agnico expects to deploy an additional $300 million in capital beyond current 2026 guidance .

Upper Beaver: Ahead of Schedule

The Upper Beaver project in the Kirkland Lake camp is expected to produce 200-220,000 ounces per year . The ramp and shaft development are running ahead of schedule, and the company is increasing investment from $200 million to $300 million to bring production forward to 2030 .

Financial Firepower: From Cash Burn to Cash Machine

The transformation in Agnico's cash generation has been remarkable. As Al-Joundi noted during the Q&A session with BMO's Matt Murphy, the company has gone "from generating under $1 billion a year in free cash flow to generating well over $1 billion per quarter" .

The balance sheet reflects this shift:

| Metric | Q1 2024 | Q4 2025 | Change |

|---|---|---|---|

| Revenue | $1.83B | $3.56B | +95% |

| EBITDA | $0.89B | $2.47B | +177% |

| EBITDA Margin | 48.6% | 69.2% | +21 pts |

| Free Cash Flow | $0.40B | $1.19B | +198% |

| Net Debt/(Cash) | $1.46B | ($2.55B) | - |

Source: S&P Global

In 2025 alone, Agnico repaid nearly $1 billion in debt, built up nearly $3 billion in cash, and returned over $1.4 billion to shareholders through dividends and buybacks .

Gold Leverage: 95% Pass-Through

Perhaps most impressive is Agnico's ability to capture gold's upside. While the gold price rose $1,700 per ounce year-over-year in 2025, Agnico's cash costs increased just $76 per ounce .

"This means we delivered over 95% of this gold price increase to the benefit of our shareholders," Al-Joundi emphasized.

Looking ahead to 2026, the company's cost guidance midpoint is $1,070/oz for cash costs and $1,475/oz for all-in sustaining costs. Approximately 60% of the cost increase reflects higher royalties from elevated gold prices and a stronger Canadian dollar—factors that actually benefit shareholders on a net basis .

The M&A Question

On M&A, Al-Joundi maintained Agnico's disciplined approach: "Our M&A strategy is not based on growth, it's based on get to know what the upside is. Nothing's cheap in this world. You have to have a view on the upside."

He pointed to the company's track record—the Kirkland Lake merger that unlocked Detour's potential, and the Yamana acquisition that delivered Malartic—as examples of deals where Agnico's deep regional knowledge provided conviction on upside others couldn't see .

When asked about potential acquisition of Teck Resources' 50% stake in the San Nicolás copper-gold project, Al-Joundi was direct: "If it made money for our owners on a per share basis, absolutely, we would consider it."

Forward Estimates: Street Expects Continued Growth

Analysts are pricing in substantial earnings growth as production ramps and gold prices remain elevated:

| Metric | FY 2025A | FY 2026E | FY 2027E |

|---|---|---|---|

| Revenue | $11.9B | $16.5B | $15.8B |

| EBITDA | $8.2B | $12.1B | $11.5B |

| EPS | $8.31 | $13.92 | $13.25 |

| Consensus Target | - | $240.87 | - |

Source: S&P Global

With the stock trading at $236.27, it sits just below the consensus target, suggesting limited near-term upside based on current estimates. However, the Hope Bay approval in May and continued exploration success at Detour and Malartic could provide catalysts for further target revisions.

What to Watch

May 2026: Hope Bay project decision—$2 billion CapEx for 400-450k oz/year operation

Mid-2027: Detour Underground bulk sample completion and final investment decision

2028: Potential first underground production at Detour Lake

2030: Upper Beaver first production target; step-change in group production per share begins

2033: Canadian Malartic reaches 1.05 million oz annual production; Detour Lake hits 1 million oz milestone

For gold bulls betting on a prolonged commodity supercycle, Agnico Eagle offers what few miners can: a clear, funded path to growth in top-tier jurisdictions, led by a management team with a 20-year track record of per-share value creation.

As Al-Joundi put it: "Not only have we done this for 20 years, but there's a clean path to continuing to grow gold production per share over the next decade. That's not an easy thing to do."