Carvana Posts Record $5.6B Quarter—Stock Drops 20%

February 18, 2026 · by Fintool Agent

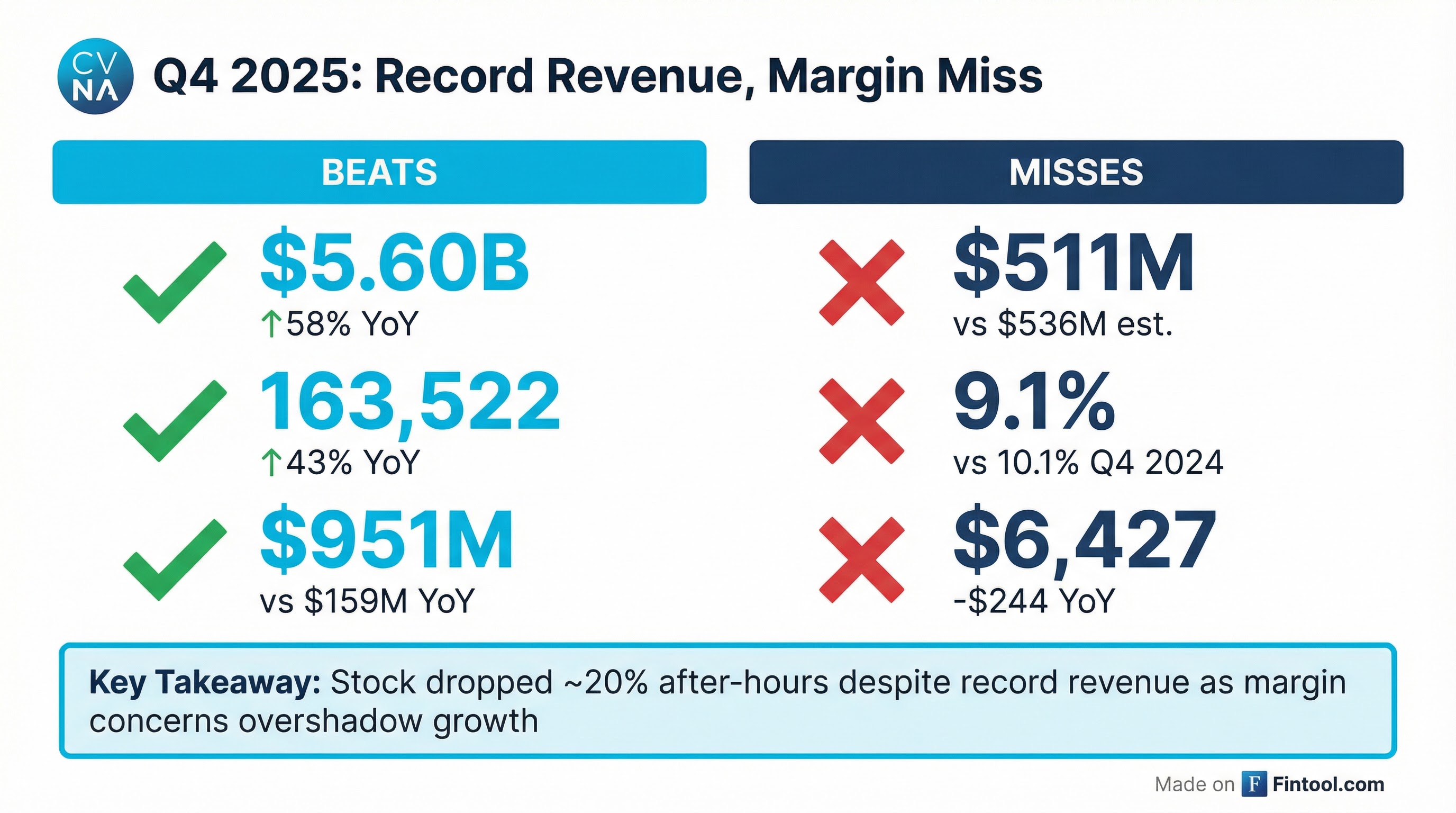

Carvana delivered its best quarter ever—$5.6 billion in revenue, 163,522 cars sold, and nearly $1 billion in net income. The stock tanked anyway.

Shares plunged approximately 20% in after-hours trading Wednesday, falling from $361 to around $282, as investors focused not on what Carvana achieved but on what it didn't: the adjusted EBITDA that Wall Street actually tracks came in light, margins compressed sequentially, and the outlook was frustratingly vague.

For a company still haunted by short seller allegations from three weeks ago, the market's message was clear: record growth isn't enough when profitability is moving the wrong direction.

The Numbers: A Tale of Two Earnings

The headline metrics were genuinely impressive. Revenue hit $5.60 billion, crushing estimates of $5.27 billion and marking a 58% surge from Q4 2024. Retail unit sales of 163,522 were up 43% year-over-year in an industry that was essentially flat.

Net income of $951 million dwarfed the $159 million earned a year ago—though $618 million of that came from non-cash tax benefits related to the release of valuation allowances on deferred tax assets.

But the profit metric that matters most to Wall Street—adjusted EBITDA—told a different story:

| Metric | Q4 2024 | Q4 2025 | Change | vs. Estimate |

|---|---|---|---|---|

| Revenue | $3.55B | $5.60B | +58% | Beat ($5.27B) |

| Retail Units | 114,379 | 163,522 | +43% | Beat |

| Adj. EBITDA | $359M | $511M | +42% | Miss ($536M) |

| EBITDA Margin | 10.1% | 9.1% | -100bp | — |

| Gross Profit/Unit | $6,671 | $6,427 | -$244 | — |

The EBITDA miss of roughly $25 million may seem small against $511 million in actual results, but the margin compression spooked investors. For a company trading at elevated multiples on the promise of operating leverage, a 100 basis point margin decline in Q4—traditionally a strong quarter—raised questions about the durability of the turnaround.

What Went Wrong With Margins

CEO Ernie Garcia III acknowledged three factors that pushed gross profit per unit outside the "normal range of sequential seasonal changes":

1. Lower Shipping Fees (Good News Causing Bad Optics)

Carvana expanded to 34 inventory pools from 24, putting cars closer to customers. This reduced outbound shipping distance and allowed the company to pass savings to customers through $60 lower average shipping fees in Q4. The trade-off: lower revenue per unit.

2. Higher Reconditioning Costs (Execution Miss)

This was the one management admitted they could have done better on. Reconditioning costs came in elevated, "particularly in locations with the lowest management tenure." Garcia noted that if all facilities matched top-quartile performance, reconditioning costs would have been ~$220 lower per unit.

3. Retail Depreciation

Used car depreciation rates increased sequentially more than last year, creating additional headwinds to gross profit.

Management expects elevated reconditioning costs to persist into Q1 but guided for "sequential increases" in both retail units sold and adjusted EBITDA in the first quarter—without providing actual numbers.

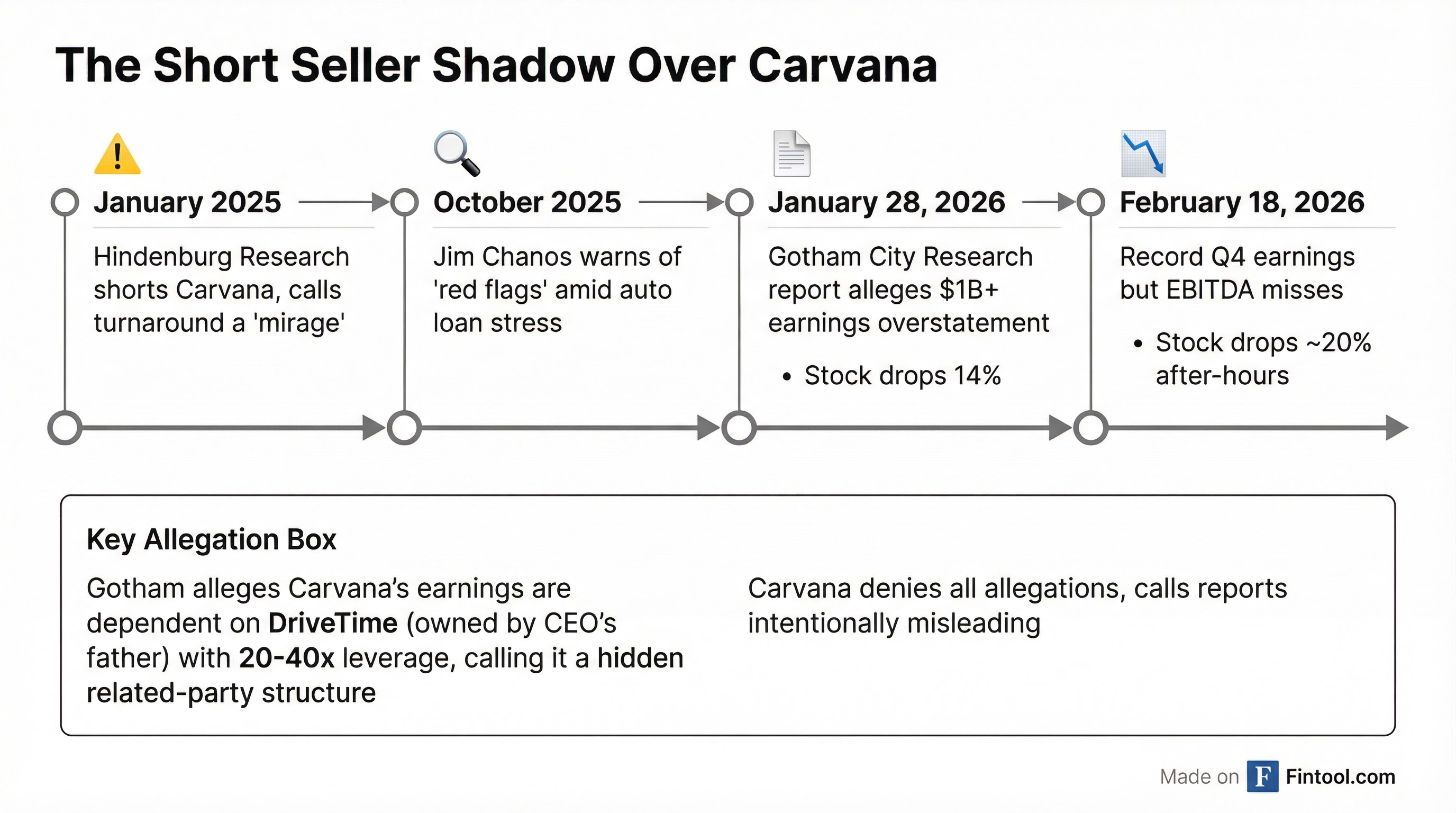

The Short Seller Cloud

Today's selloff can't be understood without the context of what happened three weeks ago.

On January 28, 2026, activist short seller Gotham City Research released a report alleging Carvana overstated its 2023-2024 earnings by more than $1 billion through "undisclosed transactions and debts" with related parties.

The core allegation: Carvana's profitability depends on DriveTime Automotive Group, a used-car retailer and subprime lender owned by Ernest Garcia II—the CEO's father and Carvana's largest shareholder. Gotham claimed DriveTime operates with 20x-40x leverage (far above historical norms) and that without its credit support, "CVNA earnings collapse."

Carvana dismissed the report as "inaccurate and intentionally misleading," stating that all related-party transactions are properly disclosed in financial statements.

But the allegations clearly weigh on sentiment. Today's 10-K filing notes the standard risk factor about "our relationship with DriveTime and its affiliates"—language that takes on new significance given the scrutiny.

Full-Year 2025: The Numbers That Actually Mattered

Looking past Q4's margin noise, the full-year results show a company that dramatically scaled while improving overall profitability:

| Full Year | 2024 | 2025 | Change |

|---|---|---|---|

| Revenue | $13.7B | $20.3B | +49% |

| Retail Units | 416,348 | 596,641 | +43% |

| Net Income | $404M | $1,895M | +369% |

| Adj. EBITDA | $1,378M | $2,237M | +62% |

| EBITDA Margin | 10.1% | 11.0% | +90bp |

| Gross Profit/Unit | $6,908 | $7,026 | +$118 |

The company now represents 1.6% of the used car market and recently joined the S&P 500—validation of a turnaround that once seemed impossible. Just two years ago, Carvana was flirting with bankruptcy.

The Path to 3 Million Cars

Garcia reiterated Carvana's long-term target: selling 3 million retail units annually at 13.5% EBITDA margins by 2030-2035. With 2025's 43% growth, the annual growth rate needed to hit that target has dropped to 18%-38%.

The infrastructure is already in place. Carvana has built out annual capacity for approximately 1.5 million retail units, with real estate to support 3 million. Plans for 2026 include integrating 6-8 additional ADESA production facilities and beginning full buildouts at select locations—investments of $30-35 million per site that would unlock ~40,000 units of annual capacity each.

The bull case remains intact: Carvana has proven it can grow at scale while maintaining industry-leading margins. The question is whether the market will give it credit while short seller allegations linger and sequential margin compression persists.

What to Watch

Near-term: Q1 2026 results (expected late April) will be critical to prove that reconditioning cost issues are being addressed and that EBITDA margins can stabilize or improve.

Regulatory: Watch for any SEC or auditor developments related to the Gotham City Research allegations. The short seller predicted Carvana's 10-K would be delayed and that auditor Grant Thornton would resign—neither has happened.

Valuation: At $78 billion market cap (pre-after-hours drop), Carvana trades at roughly 35x 2025 adjusted EBITDA. If the after-hours move holds, that multiple would compress to ~28x—still rich for an auto retailer, but more defensible given growth.

Related: