Coeur Mining Eyes $20B Precious Metals Empire as New Gold Deal Nears Close

February 24, 2026 · by Fintool Agent

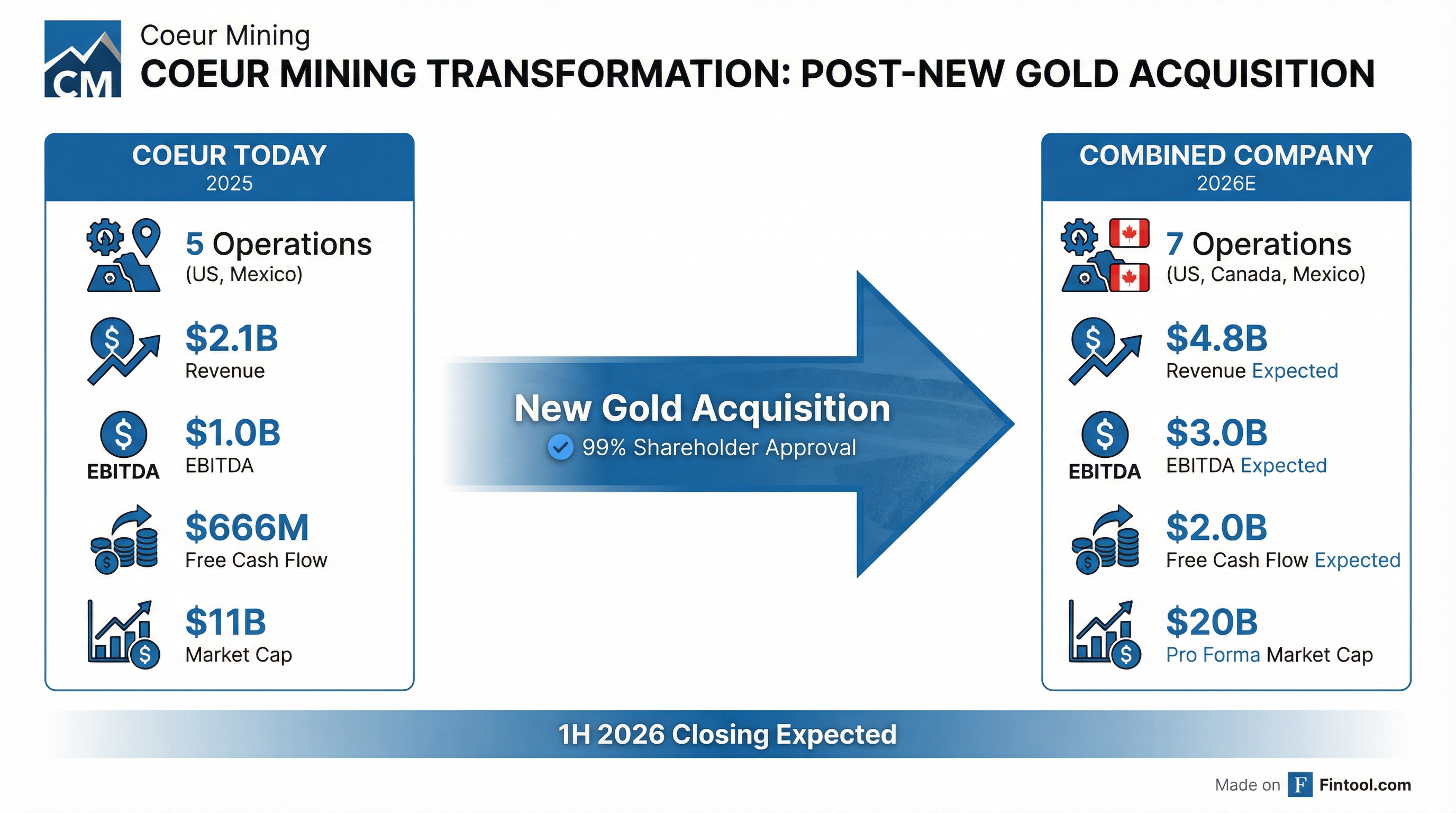

Coeur Mining used the BMO Capital Markets Global Metals, Mining & Critical Minerals Conference in February 2026 to outline what the company called a "step-change" in its financial profile—record quarterly and full-year free cash flow, a net-cash balance sheet, and a transformative acquisition that will create the largest U.S.-based precious metals producer in two decades.

The Chicago-based miner reported 2025 revenue nearly doubled to $2.07 billion with net income surging to $586 million—a tenfold increase from the prior year. Cash ballooned from $55 million to $554 million while total debt fell from $590 million to $341 million, flipping Coeur into a net-cash position for the first time in years.

"Just two years ago, Coeur's full-year EBITDA totaled $142 million and its free cash flow was negative $297 million," the company noted in its presentation. "Even comparing to our expected approximate $1 billion of EBITDA and $550 million of free cash flow in 2025 highlights the extent to which this transaction helps accelerate Coeur's ongoing repositioning."

The New Gold Deal: Creating a North American Powerhouse

The acquisition of New Gold, announced November 3, 2025, received overwhelming shareholder support with 99.22% voting in favor on January 27, 2026. The Supreme Court of British Columbia granted final approval on January 30, 2026, clearing the last major hurdle before regulatory sign-off from Canada's Investment Canada Act.

The combined company will command approximately $20 billion in market capitalization with seven high-quality North American operations expected to produce 900,000 ounces of gold, 20 million ounces of silver, and 100 million pounds of copper in 2026. Management projects $3.0 billion in EBITDA and $2.0 billion in free cash flow for the combined entity—nearly triple Coeur's standalone 2025 performance.

| Combined Company Metrics (2026E) | Value |

|---|---|

| Pro Forma Market Cap | $20 billion |

| Combined EBITDA | $3.0 billion |

| Combined Free Cash Flow | $2.0 billion |

| Gold Production | 900,000 oz |

| Silver Production | 20 million oz |

| Copper Production | 100 million lbs |

| Operating Mines | 7 |

New Gold CEO Patrick Godin and director Marilyn Schonberner have been conditionally appointed to Coeur's board, effective upon deal closing.

Record 2025 Results: A Year of Transformation

The BMO presentation showcased Coeur's dramatic financial turnaround. Q4 2025 alone generated $675 million in revenue, $215 million in net income, and $313 million in free cash flow.

| Metric | FY 2024 | FY 2025 | YoY Change |

|---|---|---|---|

| Revenue | $1,054M | $2,070M | +96% |

| Net Income | $59M | $586M | +895% |

| Adj. EBITDA | $339M | $1,026M | +202% |

| Free Cash Flow | -$9M | $666M | NM |

| Cash Balance | $55M | $554M | +906% |

The February 2025 acquisition of SilverCrest and its high-grade Las Chispas silver-gold mine in Mexico was a major catalyst, contributing to record production of 422,031 gold ounces and 17.9 million silver ounces in 2025.

Rochester, Coeur's flagship Nevada operation and America's largest source of domestically produced silver, delivered a breakout fourth quarter with record crushing rates and $77.8 million in free cash flow. Management expects silver production to increase 16% and gold production to rise 8% at Rochester in 2026.

Portfolio Expansion: Seven Mines Across Three Countries

The combined company will operate entirely within North America's most stable mining jurisdictions—a key selling point given increasing investor focus on geopolitical risk.

Coeur's Current Operations:

- Rochester (Nevada): Silver-gold, ~15-year mine life

- Las Chispas (Sonora, Mexico): Silver-gold, ~7-year mine life

- Palmarejo (Chihuahua, Mexico): Gold-silver, ~11-year mine life

- Kensington (Alaska): Gold, ~5-year mine life

- Wharf (South Dakota): Gold, ~12-year mine life

New Gold's Canadian Assets:

- New Afton (British Columbia): Gold-copper, mine life through 2031

- Rainy River (Ontario): Gold, mine life through 2033

New Afton's C-Zone ramp-up and K-Zone exploration upside were highlighted as key growth drivers. Recent drilling intersected C-Zone grade copper-gold mineralization 1,800 feet east of the current K-Zone footprint, with East Extension added to mineral reserves.

2026 Guidance: Positioning for Record Results

Management issued 2026 production guidance calling for 390,000-460,000 ounces of gold and 18.2-21.3 million ounces of silver from Coeur's standalone operations—before adding New Gold's contribution.

| Asset | 2026E Gold (Koz) | 2026E Silver (Koz) |

|---|---|---|

| Las Chispas | 55-65 | 5,500-6,300 |

| Palmarejo | 95-105 | 6,250-7,000 |

| Rochester | 70-90 | 6,400-7,800 |

| Kensington | 98-110 | - |

| Wharf | 72-90 | 50-200 |

| Total | 390-460 | 18,200-21,300 |

Guidance assumes gold at $4,550/oz and silver at $77.50/oz—prices that have proven conservative given gold recently touched $5,594/oz and silver trades above $80/oz.

Capital expenditures are projected at $304-$364 million, with exploration investment increasing 47% to $120-$136 million as Coeur targets resource expansion at Palmarejo, Las Chispas, and Silvertip.

The Gold Tailwind: Record Prices Drive Margins

Coeur's timing has been impeccable. Gold prices have surged past $5,000/oz—up roughly 110% from 2024 Paris Olympics levels—driven by tariff uncertainty, inflation concerns, and central bank accumulation. Silver has tripled over the past 18 months to above $81/oz.

Goldman Sachs forecasts gold reaching $5,400 by year-end 2026, while J.P. Morgan sees potential for $6,300. Central bank purchases remain a structural tailwind, with JPMorgan estimating approximately 755 tonnes of sovereign gold buying in 2026—50-90% above pre-2022 averages.

At current spot prices well above guidance assumptions, Coeur's margins have significant upside. The company projects a 63% EBITDA margin in Q4 2025 alone, up from 32% in 2024.

Stock Performance: A Five-Bagger in Two Years

Coeur shares have rewarded patient investors handsomely. From a 52-week low of $4.58, the stock has surged to $24.43—a gain of approximately 434%. The 50-day moving average of $20.66 and 200-day average of $14.81 both slope sharply upward.

Analyst sentiment remains constructive. The consensus price target of $27.14 implies ~11% upside from current levels.* TD Securities, RBC Capital Markets, and Raymond James all cover the name, with most analysts rating it a Buy.

*Values retrieved from S&P Global

What to Watch

Near-Term Catalysts:

- New Gold closing (expected 1H 2026): Investment Canada Act approval is the final regulatory hurdle

- Updated combined guidance: Management will issue consolidated production and cost targets post-close

- Capital return framework: Company plans to provide updated shareholder return policies after integration

Key Risks:

- Precious metals price volatility: Guidance assumes $4,550 gold and $77.50 silver; downside exposure if prices correct

- Integration execution: Merging two mining companies with different cultures and systems

- Regulatory/political: Canadian foreign investment review, potential tariff impacts on cross-border operations

- Shareholder lawsuits: Two New York cases seek to block the deal, alleging inadequate disclosure

Return on invested capital tells the story of Coeur's transformation. The company projects 44.5% ROIC in 2026, peer-leading among both gold and silver producers. After years of heavy capital investment in Rochester's expansion and strategic acquisitions, Coeur is entering what management calls a "harvest phase" of strong free cash flow generation.

Related Companies: Coeur Mining · New Gold