CoreWeave Tumbles 12% as Blue Owl Fails to Secure $4B Data Center Debt

February 20, 2026 · by Fintool Agent

Coreweave (CRWV) shares plunged 12% Friday after Business Insider reported that Blue Owl Capital (OWL) failed to secure $4 billion in third-party debt financing for a major AI data center project the companies are co-developing in Lancaster, Pennsylvania.

The financing freeze raises pointed questions about credit appetite for the AI infrastructure buildout—and about CoreWeave's debt-fueled business model that has made it one of the most closely watched (and heavily leveraged) names in the AI cloud computing race.

Blue Owl, which has emerged as one of the most creative financial architects of the data center boom, spent months pitching the Lancaster project to potential lenders. One lender who passed told Business Insider the lack of interest was due to CoreWeave's creditworthiness.

Blue Owl responded that the project is "fully funded, on time, and on budget"—but it remains unclear whether that funding comes entirely from Blue Owl's own capital, which would require a substantial cash outlay.

The Debt-Fueled AI Hyperscaler

CoreWeave represents the most aggressive application of leverage in the AI infrastructure boom. The company, which went public in March 2025 at $40 per share and peaked above $180 three months later, has since fallen over 60% as investors grapple with its capital structure.

The numbers are striking:

| Metric | Q1 2025 | Q2 2025 | Q3 2025 |

|---|---|---|---|

| Revenue | $982M | $1.21B | $1.36B |

| Total Debt | $11.9B | $14.6B | $18.8B |

| Net Income | -$315M | -$291M | -$110M |

| Total Assets | $21.9B | $26.2B | $32.9B |

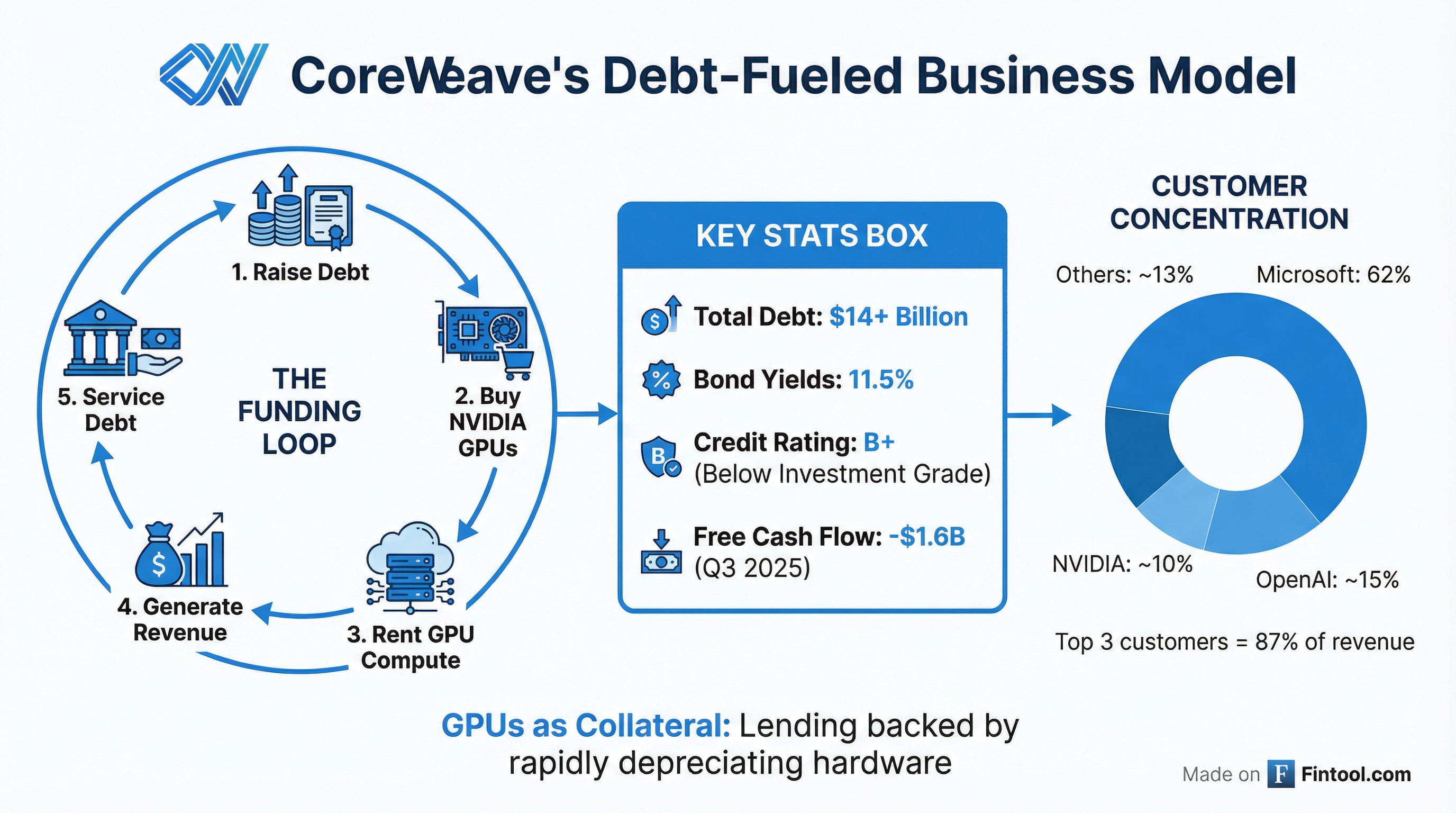

Revenue is surging—up 134% year-over-year in Q3. But so is debt. CoreWeave has borrowed over $12.9 billion in the past two years alone, much of it at high interest rates (10-15%), collateralized by the very NVIDIA GPUs generating the company's revenue.

The company's 2031 bonds trade at 11.5% yields, signaling significant credit risk despite the revenue growth. S&P rates CoreWeave B+—two notches below investment grade.

The Lancaster Project

The $4 billion Lancaster campus, located 80 miles west of Philadelphia, was announced last summer when CoreWeave committed to lease 100 megawatts of initial capacity with potential expansion to 300 megawatts. CoreWeave said it would invest up to $6 billion to equip the facility with chips and cloud infrastructure.

In August 2025, Chirisa Technology Parks partnered with Blue Owl and Machine Investment Group to develop the project, committing $4 billion for construction separate from CoreWeave's equipment investment. That fall, Blue Owl began shopping the development to potential lenders.

The pushback from lenders marks a notable contrast to Blue Owl's success in other deals. Last year, the firm structured a partnership with Meta for a Louisiana data center campus, raising $27.3 billion in investment-grade corporate bonds against its share of the project's equity—benefiting from Meta's strong credit rating.

The difference? Meta is investment-grade. CoreWeave is not.

The GPU Collateral Question

At the heart of the financing challenge is a structural issue: CoreWeave's loans are secured by rapidly depreciating GPU hardware. This creates what analysts describe as a "perpetual leverage loop"—using GPUs as collateral to borrow money to buy more GPUs.

Bloomberg, the Financial Times, and Reuters have all raised concerns that the growing use of GPUs as loan collateral "embeds aggressive assumptions about hardware depreciation, utilization, and refinancing conditions, leaving AI data-center financing structures vulnerable if GPU values decline or demand softens."

The concern is not hypothetical. GPU technology advances rapidly—Nvidia's (NVDA) next-generation chips can render current hardware obsolete in 2-3 years. If AI demand cools or customers shift to newer hardware, the collateral backing CoreWeave's loans could be worth far less than projected.

NVIDIA itself recently invested $2 billion in CoreWeave at $87.20 per share as part of a broader collaboration agreement—in part, analysts suggest, to shore up confidence in one of its largest customers.

Customer Concentration Adds Risk

Beyond the debt, CoreWeave faces significant concentration risk. According to filings, 62% of 2024 revenue came from Microsoft, with OpenAI and NVIDIA comprising much of the remainder. In Q2 2025, a single customer (likely Microsoft) represented 71% of revenue.

The company boasts a $55 billion revenue backlog—but much of it depends on continued demand from a handful of hyperscaler clients who have their own cloud infrastructure and could theoretically in-source workloads.

CoreWeave burned $1.59 billion in free cash flow in Q3 2025 as it races to build out data center capacity. The company carries roughly $29 billion in total liabilities against just $3.9 billion in equity.

What It Means for the AI Buildout

The failed financing is a signal—not necessarily of CoreWeave-specific distress, but of broader credit market caution toward the AI infrastructure boom.

AI-related financing deals reached $200 billion in 2025, with no slowdown on the horizon. But as the Financial Times noted, "for some of the newer players, which offer specialized, on-demand AI compute, AI-related growth has been funded largely through debt rather than free cash flow."

The question now is whether lenders will continue extending credit to companies without investment-grade ratings, or whether the AI infrastructure race will increasingly be dominated by companies—like Meta, Microsoft, and Google—that can self-fund or access cheap capital.

BMO Capital Markets analyst Brennan Hawken, who covers Blue Owl, said difficulties in raising debt for the Lancaster project "would raise concern." He added: "If there is a struggle to find the debt financing, that's a bit of a red flag that I would want to drill into."

Blue Owl's Response

Blue Owl shares fell 5.9% on Friday, adding to pressure on the alternative asset manager. The firm manages over $180 billion in assets and has become a major player in infrastructure financing.

The company's statement that the Lancaster project is "fully funded" raises its own questions. If Blue Owl is covering the $4 billion construction cost from its own balance sheet rather than third-party debt, it would represent a substantial concentration of risk in a single credit-challenged tenant.

CoreWeave's Q4 2025 earnings are due next week, giving management an opportunity to address investor concerns about financing and execution.

The Bottom Line

The failed financing attempt is a reminder that the AI infrastructure boom isn't just a technology story—it's a credit story. Companies like CoreWeave have grown explosively by leveraging their GPU inventories to borrow at high rates, betting that AI demand will grow fast enough to service the debt.

For now, that bet is still working: CoreWeave's revenue is up 134% year-over-year, and major customers like Microsoft and OpenAI continue to sign long-term contracts. But when lenders start saying no, as they did with Blue Owl's pitch for the Lancaster project, it's worth asking whether the market is beginning to price in the risks that have always been embedded in the debt-fueled AI buildout.