Coronado CEO Douglas Thompson Resigns After Stock Falls 69% During Three-Year Tenure

February 23, 2026 · by Fintool Agent

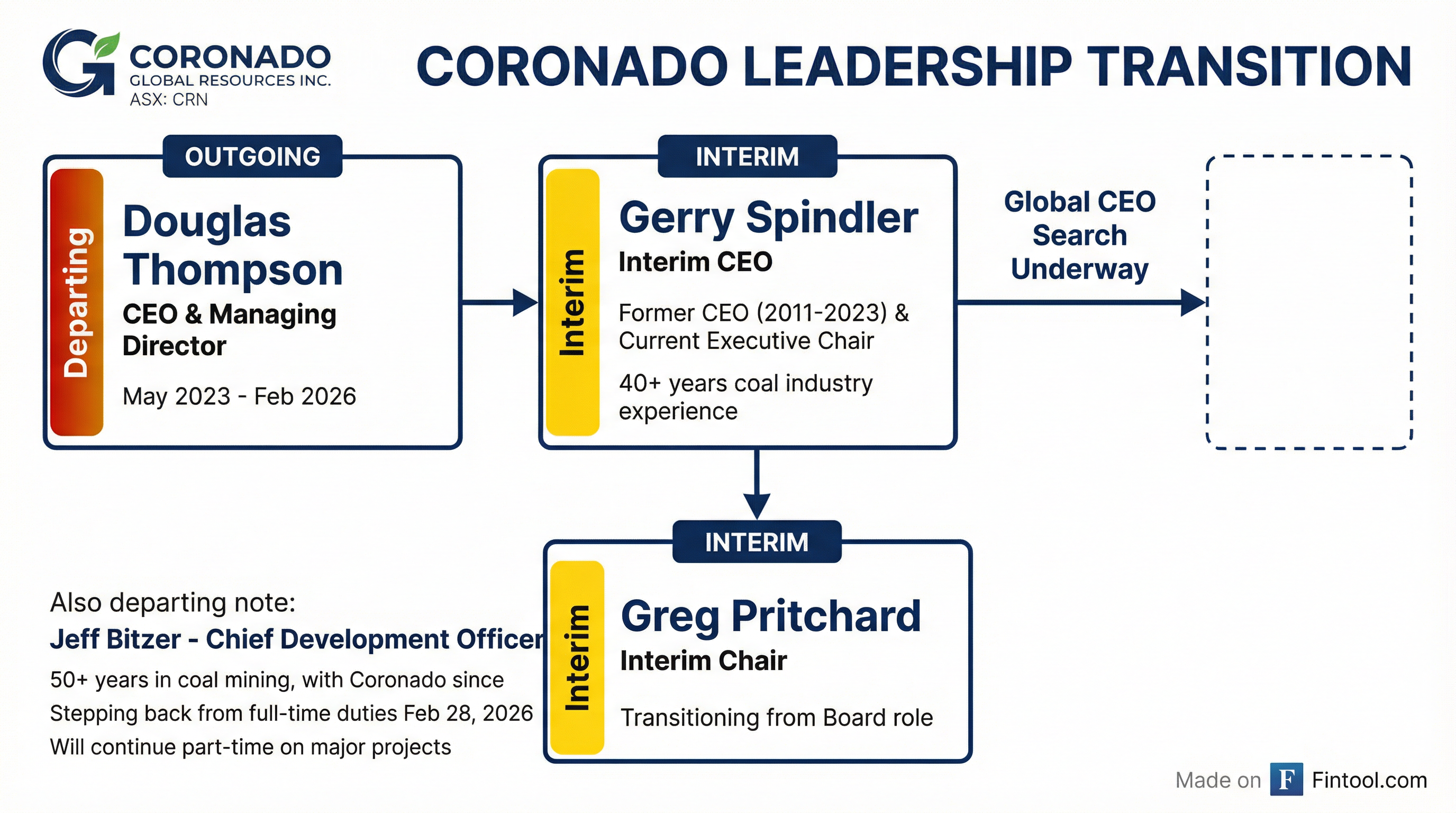

Coronado Global Resources (ASX: CRN, OTC: CODQL) announced the resignation of CEO Douglas Thompson on Sunday, sending shares tumbling 7-9% in early Australian trading. Thompson is departing after completing his three-year operational turnaround plan, but leaves behind a stock that has declined 69% during his tenure amid a brutal metallurgical coal downturn and mounting balance sheet pressures.

The timing of the exit raises questions. While Coronado framed the departure as Thompson having "successfully fulfilled all commitments," the CEO is leaving just months after the company warned of potential debt covenant breaches, received credit rating downgrades, and posted a $109 million loss in fiscal 2024.

The Three-Year Plan: Mission Accomplished?

Thompson took the helm in May 2023 with a clear mandate: transform Coronado's cost structure, unlock organic growth from existing assets, and navigate the cyclical coal market. By most operational metrics, he delivered.

Key achievements during Thompson's tenure:

- Mammoth Underground — Coronado's first Australian underground mine opened in December 2025 at the Curragh complex, expected to reach 1.5-2 million tons annually at significantly lower costs than surface operations

- Buchanan Expansion — The US operation was expanded with new development sections in the northern and southern districts

- Cost Reduction — Group mining costs fell 10% from $107/ton to $97/ton through fleet reductions and productivity improvements

- Curragh Restructuring — The Australian flagship was divided into three distinct complexes with improved dragline productivity

But the Market Didn't Care

Despite operational progress, Coronado's stock cratered from A$0.90 when Thompson became CEO to A$0.28 at his departure — a 69% decline.

The culprit: metallurgical coal prices collapsed. The PLV hard coking coal benchmark, Coronado's primary revenue driver, spent much of 2024-2025 in the $160-200/ton range — well below the $300+ levels seen in 2022 when the company was generating $772 million in annual profit and paying out nearly 50% dividend yields.

| Metric | FY 2023 | FY 2024 |

|---|---|---|

| Revenue | $2.83B | $2.44B |

| Net Income | $156M | -$109M |

| Cash from Operations | $268M | $74M |

| EBITDA | $303M* | $80M* |

*Values retrieved from S&P Global

The $265 million swing from profit to loss forced Coronado into survival mode. By November 2025, the company was warning of potential debt covenant breaches and receiving credit rating downgrades.

Double Departure: CDO Also Leaving

Thompson isn't the only veteran heading for the exit. Chief Development Officer Jeff Bitzer, who has spent 50 years in coal mining and has been with Coronado since its inception, is stepping back from full-time duties effective February 28, 2026.

Bitzer will continue on a part-time basis focusing on major projects that benefit from his technical expertise — a signal that critical development work remains.

The Old Guard Returns

Filling the CEO void will be Gerry Spindler, Coronado's Executive Chair and former CEO who led the company from 2011 until Thompson's appointment in 2023. Spindler, 77, has over 40 years in the coal industry including stints as CEO of UK Coal, Amax Coal Company, and Pittston Coal Company.

Greg Pritchard will transition to Interim Chair of the Board, subject to board approval. The company has commenced a global search for a permanent CEO.

Spindler's return represents continuity — he built Coronado into its current form and knows its assets intimately. But at 77, he's clearly a placeholder, and the interim structure introduces uncertainty at a challenging time.

The Real Question: Why Now?

Coronado's official line is that Thompson is leaving after "successfully fulfilling all commitments" in the three-year plan to "pursue new opportunities."

But the timing is curious:

-

The hard part starts now — With Mammoth and Buchanan expansions complete, 2026 was supposed to be the year where benefits materialized. Why leave before collecting the reward?

-

Balance sheet stress — The company secured a new $265 million ABL facility to shore up liquidity, but debt covenant concerns remain fresh.

-

The Stanwell overhang — A burdensome supply contract with Stanwell won't reset until late 2026, continuing to drag on margins. Thompson called it "a contract that we inherited" and "very burdensome on the business."

-

No disclosed succession plan — A planned exit typically includes an orderly handoff, not a global CEO search starting from scratch.

The resignation, combined with Bitzer's departure, suggests either exhaustion with the job's demands, disagreement on strategy going forward, or simply better opportunities elsewhere in a recovering mining market.

What's Next for Coronado

For investors, the immediate question is whether the leadership vacuum disrupts the recovery story that was finally coming together:

Near-term catalysts:

- Q4 2025 / FY 2025 results (released February 2026) showed production up 4% to 16 million tons and mining costs down 10% to $97/ton

- Stanwell contract reset expected in late 2026, removing ~$15/ton cost headwind at Curragh

- Mammoth Underground ramping toward 2 million ton annual run rate

- Met coal prices recovering, with PLV index rising to $218/ton

Key risks:

- Leadership uncertainty during critical execution phase

- Debt levels remain elevated (~A$645M total debt vs. A$172M cash)

- Continued met coal price volatility

- Regulatory overhang from recent mine safety incidents

Analysts currently rate the stock a "Neutral" with an average price target of A$0.39, implying modest upside from current levels. UBS upgraded to "Buy" in January with a A$0.53 target.

The Bottom Line

Douglas Thompson delivered operationally — costs are down, production is up, and major capital projects are complete. But the stock tells a different story: down 69% as metallurgical coal markets collapsed and balance sheet stress mounted.

The departure of both the CEO and CDO simultaneously, combined with an interim management structure, adds uncertainty at precisely the moment investors were hoping to see the payoff from years of heavy investment. Incoming Interim CEO Gerry Spindler knows the company well, but at 77, he's a bridge to an unknown permanent successor.

For Coronado, the path forward depends less on who's in the corner office and more on metallurgical coal prices, execution of the Mammoth ramp-up, and the Stanwell contract reset. Those fundamentals haven't changed — but the market may need a clearer leadership picture before giving the stock credit for its improved operational positioning.

Photo: Coronado Global Resources