FAT Brands Files Chapter 11 With $1.45B Debt, Adding to Casual-Dining Carnage

January 27, 2026 · by Fintool Agent

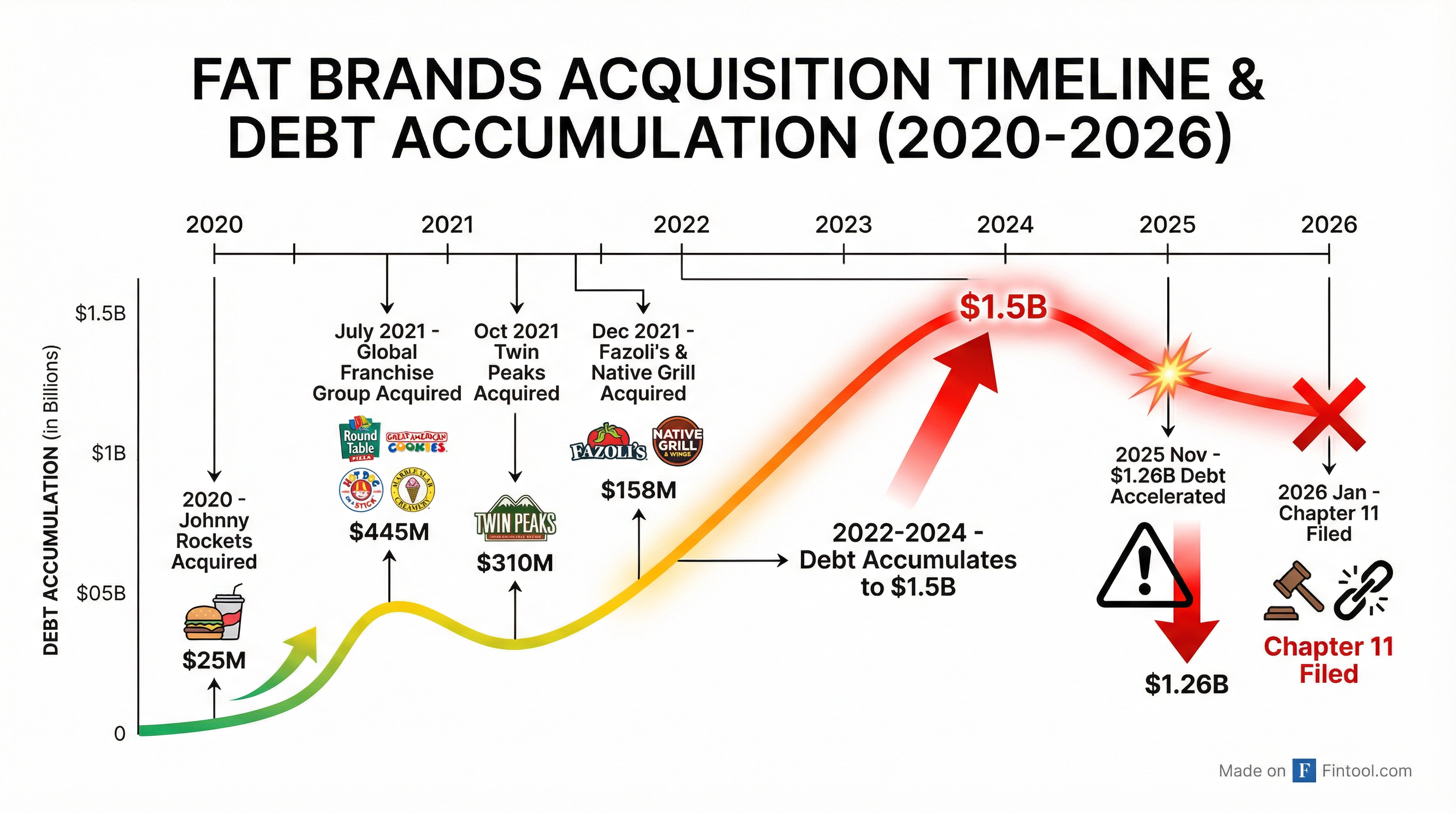

Fat Brands, the owner of Fatburger, Johnny Rockets, Twin Peaks, and 15 other restaurant concepts, filed for Chapter 11 bankruptcy protection on Sunday night with $1.45 billion in funded debt—the latest casualty in a mounting wave of casual-dining collapses fueled by aggressive debt-financed expansion.

The stock cratered 34% today to $0.26 per share, valuing the company at just $4.8 million—a stunning 94% decline from its 52-week high of $4.10.

$1.26 Billion Accelerated in November

The filing follows a cascade of events that began in October 2025 when FAT Brands missed interest payments on its whole business securitization debt. In November, trustee UMB Bank accelerated $1.26 billion in principal—demanding immediate full repayment that the company simply couldn't provide.

"The aggregate principal amount outstanding under the Accelerated Notes is $1,256.5 million... The Company and the Securitization Issuers do not currently have amounts on hand to pay such principal and interest," the company disclosed in November, warning that "such acceleration or any subsequent foreclosure may materially and adversely affect the Company's business, financial condition and liquidity."

An Acquisition Spree Gone Wrong

FAT Brands' downfall traces directly to an aggressive 18-month buying spree between 2020 and 2021 that transformed a small burger chain into an empire of 18 brands—funded almost entirely with debt.

The acquisitions came in rapid succession:

- September 2020: Johnny Rockets for $25 million

- July 2021: Global Franchise Group (Round Table Pizza, Great American Cookies, Marble Slab, Pretzelmaker, Hot Dog on a Stick) for $445 million

- October 2021: Twin Peaks for $310 million

- December 2021: Fazoli's for $138 million and Native Grill & Wings for $20 million

Total consideration: nearly $940 million in acquisitions in just 18 months, financed through whole business securitization—a Wall Street instrument that bundles franchise royalty cash flows into bonds.

Financial Deterioration Accelerated

The debt load became increasingly unsustainable as FAT Brands' operating results failed to keep pace:

| Metric | FY 2021 | FY 2022 | FY 2023 | FY 2024 |

|---|---|---|---|---|

| Revenue ($M) | $119 | $404 | $476 | $587 |

| Net Loss ($M) | ($32) | ($126) | ($90) | ($190) |

| Total Debt ($B) | $1.08 | $1.21 | $1.47 | $1.57 |

| Cash ($M) | $57 | $29 | $37 | $23 |

The company accumulated nearly $440 million in cumulative net losses over four years while debt ballooned from $1.1 billion to $1.6 billion. Cash dwindled from $57 million to just $23 million.

The Whole Business Securitization Trap

FAT Brands' collapse exposes the dark side of whole business securitization—a financing structure that has now felled multiple casual-dining chains.

The structure works by pledging franchise royalty streams as collateral for bonds. When times are good, it provides cheaper financing than traditional bank debt. But when sales decline, the rigid payment schedules become crushing.

"FAT Brands' securitization notes provide that management fees are paid ahead of debt service obligations," the bankruptcy filing notes. "However, without other sources of financing, the company had 'no choice' but to use certain collections from the whole-business securitizations to fund their operations"—triggering technical defaults.

The same mechanism contributed to the bankruptcies of Red Lobster, TGI Friday's, and Hooters—all filed within the past two years. Hooters emerged from bankruptcy just weeks ago.

Debt Structure at Filing

The Chapter 11 filing reveals the byzantine structure of FAT Brands' securitization debt across multiple special purpose vehicles:

| Vehicle | Outstanding | Rate |

|---|---|---|

| FB Royalty Securitization | $201M | 4.75-9% |

| GFG Royalty Securitization | $410M | 6-9.5% |

| Twin Peaks Securitization | $403M | 7-10% |

| Fazoli's/Native Securitization | $140M | 6-9% |

| FB Resid Securitization | $110M | 10% |

Additional non-securitization debt includes promissory notes totaling roughly $45 million at rates ranging from 13.5% to 18.65%.

The Wiederhorn Factor

CEO Andy Wiederhorn, who founded FAT Brands and orchestrated its debt-fueled expansion, stepped down in 2023 amid an SEC investigation into allegations he used $27 million in company funds for personal expenses. After the charges were dropped last summer, Wiederhorn returned to the helm.

"Our dynamic portfolio of brands has demonstrated tremendous resilience in a challenging restaurant operating environment," Wiederhorn said in the bankruptcy announcement. "The chapter 11 process will provide us with the opportunity to strengthen our capital structure to support our concepts."

The board appointed two independent restructuring directors and a chief restructuring officer from Huron Consulting Services to oversee the process.

Operations Continue—For Now

FAT Brands says its 2,200+ restaurant locations across all 18 concepts will continue operating "as usual" during the Chapter 11 process. The company has filed "first day" motions seeking emergency relief to maintain operations.

However, the filing reveals a concerning liquidity picture: "the budget only contemplating four weeks of runway." FAT Brands "cannot operate in Chapter 11 beyond this point without additional liquidity" and is actively seeking fresh financing.

Trading continues on NASDAQ with a "Q" suffix denoting bankruptcy proceedings. The company warns investors that "holders of Company's common shares of beneficial interest could experience a complete or significant loss on their investment, depending on the outcome of the Chapter 11 Cases."

What to Watch

Financing lifeline: FAT Brands has only four weeks of cash runway. Whether it secures debtor-in-possession financing will determine if this is an orderly restructuring or a liquidation.

Brand sales: Individual concepts like Twin Peaks, Johnny Rockets, or Fazoli's could be sold to other operators—potentially at steep discounts.

Franchisee impact: Over 45,000 corporate and franchise employees depend on the company's ability to emerge. Franchisees may face uncertainty about royalty obligations and brand support.

Industry contagion: The casual-dining debt reckoning continues. Any franchise-heavy restaurant with whole business securitization debt is now under scrutiny.