Lennox CFO Signals January Improvement at Barclays Conference: 'Okay Is an Improvement From Bad'

February 17, 2026 · by Fintool Agent

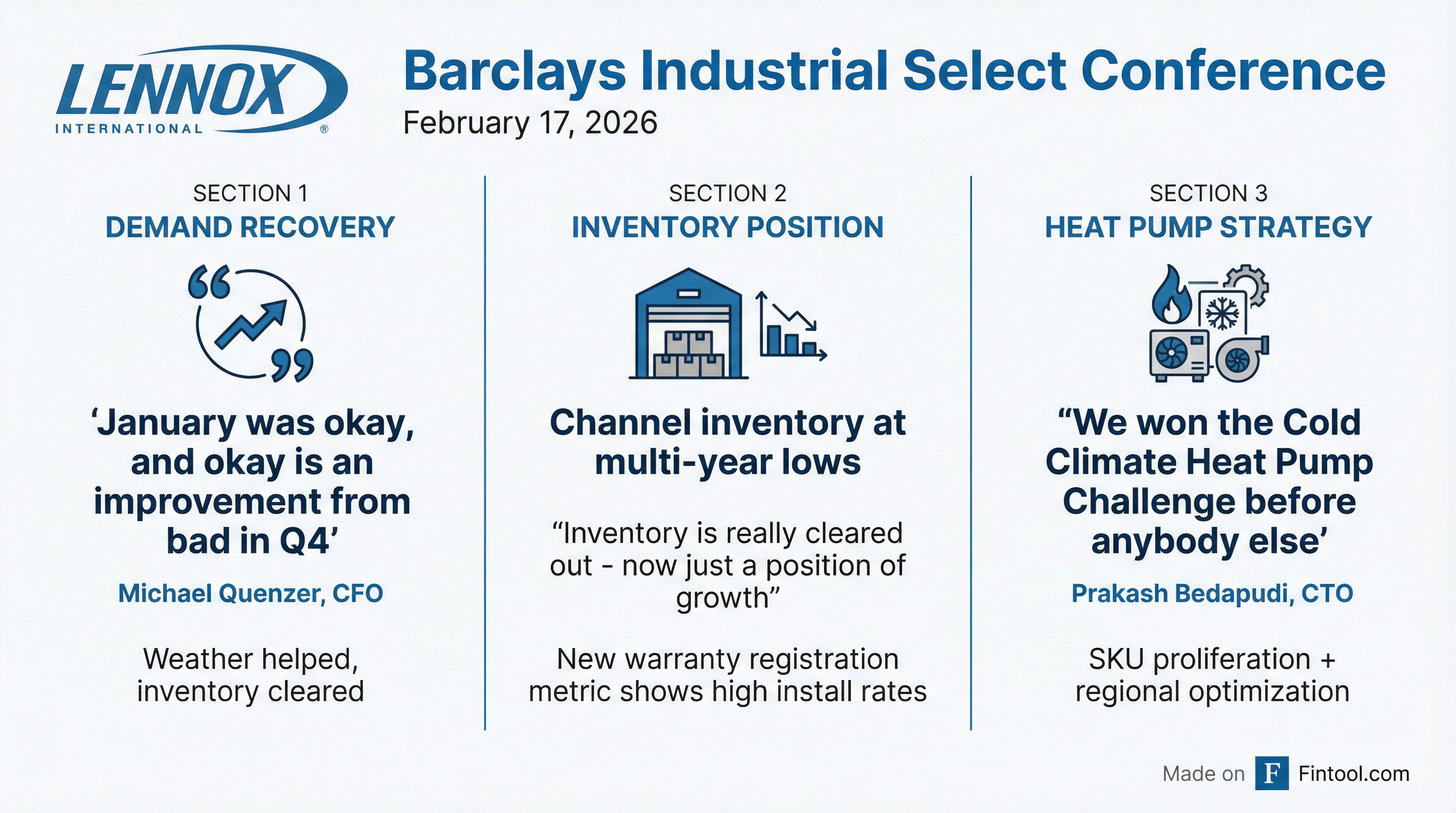

Lennox International CFO Michael Quenzer delivered cautiously optimistic commentary at today's Barclays 43rd Annual Industrial Select Conference, characterizing January demand as "okay"—a notable improvement from what he called a "bad" fourth quarter.

The HVAC manufacturer, still digesting a tough Q4 that saw revenue decline 11% year-over-year, is seeing early signs of stabilization as channel inventory clears and the industry emerges from a prolonged refrigerant transition. Shares closed at $563.90, down 0.4% on the day, trading 18% below their 52-week high of $689.

The Inventory Picture Clears

The most significant update from the conference: Lennox believes channel inventory is now at multi-year lows.

"We think inventory is low, and now it's about demand in 2026," Quenzer said. "Inventory is really cleared out and just a position of growth now."

Lennox has developed a new metric using warranty registration data to track sell-through. By comparing trailing three- and six-month shipments against warranty registrations (which occur at installation), the company can now identify inventory builds in both one-step and two-step channels.

"You're actually seeing warranty percentages very high compared to historical averages of the trailing shipments, which suggests inventory in the channel is low," Quenzer explained. "In fact, it might be lower than normal."

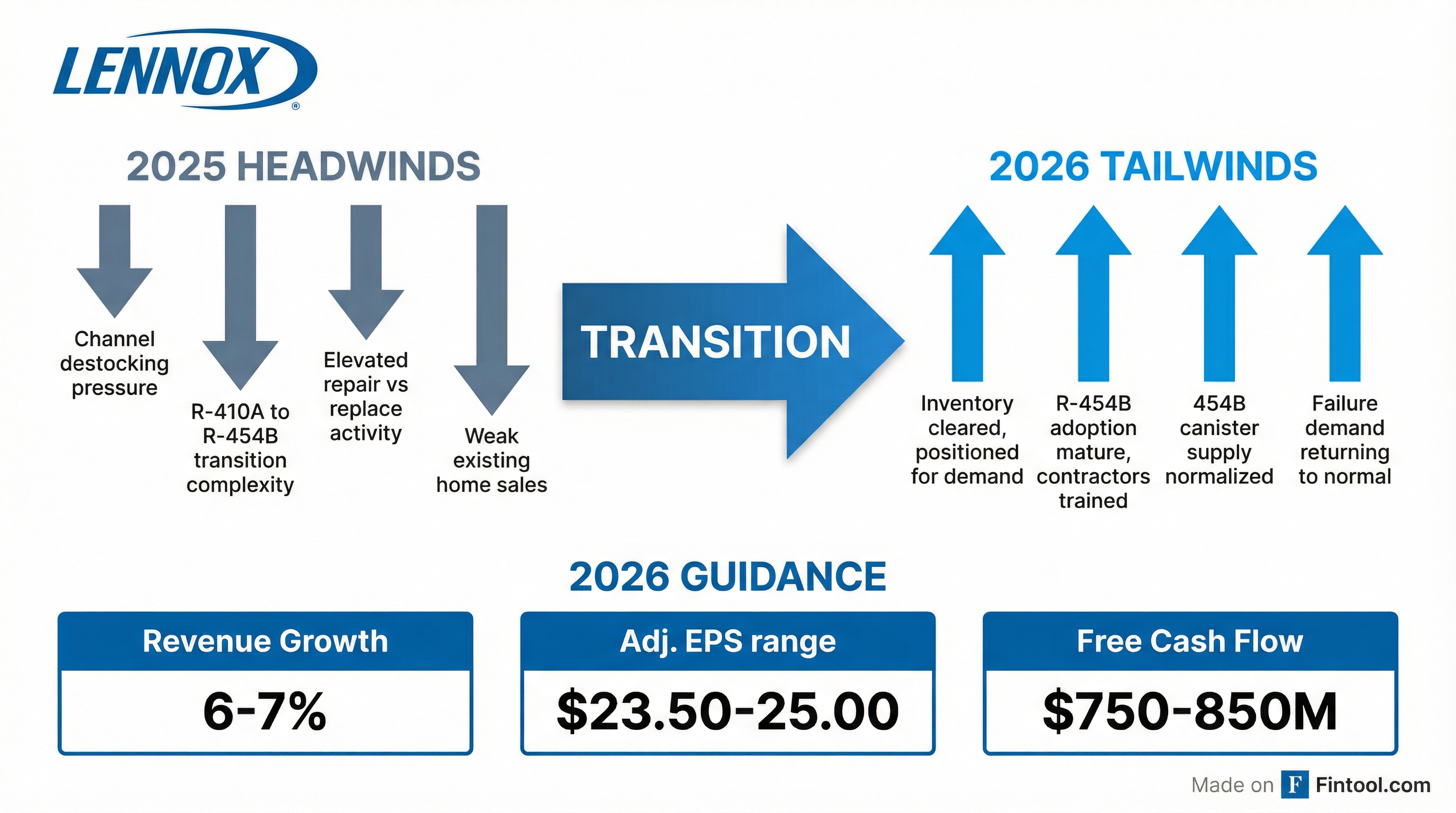

2026 Guidance: Mid-Single-Digit Volume Decline, But Growth Story Intact

Despite the encouraging inventory data, Lennox is guiding for mid-single-digit volume declines in residential HVAC for 2026.

| Metric | 2026 Guidance |

|---|---|

| Revenue Growth | 6-7% (incl. 4% from M&A) |

| Adj. EPS | $23.50 - $25.00 |

| Free Cash Flow | $750M - $850M |

| CapEx | $250M |

| Cost Inflation | 2.5% |

Source: Lennox Q4 2025 earnings release

The volume decline assumption reflects ongoing pressure in residential new construction, where Quenzer acknowledged "pricing pressures in some of that business" and low-margin business being lost.

Three Headwinds Turning to Tailwinds

Management identified three factors that pressured repair-versus-replace activity in 2025, all of which they expect to reverse:

1. R-454B Transition Complete The regulatory shift from R-410A to low-GWP R-454B refrigerant created adoption headaches in 2025—contractor learning curves and canister shortages pushed homeowners toward repairs. "We think that's behind us," Quenzer said. "That'll now turn into a tailwind."

2. Existing Home Sales Bottoming With existing home sales at 1990s lows, many homeowners are "stuck" and opting for repairs over replacements. "Hopefully, existing home sales seem to be maybe bottoming and coming up," Quenzer noted.

3. Repair Economics Deteriorating Quenzer pointed to homeowners making "not great economical decisions"—spending $4,000-$5,000 repairing 18-year-old units. But repair costs are rising: legacy R-410A gas prices are increasing, technician shortages are worsening, and contractors prefer system sales for higher margins.

CTO Prakash Bedapudi added important context on repair durability: replacing a compressor in a 15-17 year old system typically adds "another year, year and a half" at best because the underlying root cause—leaks, valve issues—remains unaddressed.

Heat Pump Strategy: SKU Proliferation and Regional Optimization

Bedapudi provided extensive detail on Lennox's heat pump positioning, addressing a historical weakness.

"Lennox always had a great heat pump technology. We won the Cold Climate Heat Pump Challenge for both residential and commercial before anybody else in the industry," Bedapudi said. "The issue was about having all the applications, SKUs required to fit all the applications."

The company recently launched what it claims is "the most compact, shortest air handler available in the industry with the highest performance"—addressing the Florida market where equipment must fit in tight closet spaces.

The strategy has two prongs:

- SKU proliferation: Filling product gaps across all applications

- Regional optimization: Different heat pump recipes for different climates—cold climate technology for the north, efficiency-optimized variants for Texas, Georgia, and Florida

Bedapudi also highlighted progress bringing variable speed technology—essential for heat pump performance—to mid-tier price points: "We have some proprietary variable speed technology we've developed in-house that you are beginning to see at a lower cost point."

Joint Ventures Expanding Product Portfolio

Lennox outlined how its Samsung and Ariston joint ventures fit the broader strategy of capturing more share of contractor wallet.

Samsung JV (Ductless/Mini-splits): Manufacturing by Samsung, distribution by Lennox, with integrated cloud connectivity allowing a single app to control both Lennox ducted systems and Samsung-powered ductless units. "75% of our contractors buy ductless," Quenzer noted. This will be "the first year of us really gaining the benefit of that Samsung joint venture."

Ariston JV (Water Heaters): Same distribution model, targeting the 50% of Lennox contractors who currently buy water heaters elsewhere.

Commercial: 15 Months of Decline, But Emergency Replacement Growing

The Building Climate Solutions (BCS) segment has faced 15 consecutive months of industry decline, with weakness in education and retail verticals.

However, Lennox sees opportunity in emergency replacement—40% of the commercial market—where it had been absent due to supply constraints. "We're now back in that piece of the vertical, and we're actually seeing growth," Quenzer said.

The Mexico manufacturing facility, while past its ramp-up headwinds, is now delivering improved lead times and quality for large national accounts, even if full cost productivity benefits are still emerging.

Q1 Absorption Headwind to Weigh on Results

Investors should expect a weaker Q1, primarily due to production absorption headwinds.

Lennox entered 2026 with elevated finished goods inventory—a deliberate choice to maintain availability if demand rebounds sharply. To balance production and demand, the company is reducing output in Q1, keeping inventory flat but creating an absorption headwind that will disproportionately impact the smaller first quarter.

"That reduction of production in the first quarter will create an absorption headwind that we'll recognize in the period," Quenzer explained. The noise should dissipate by Q2, with potential absorption benefits in H2 as factories ramp back up.

The excess inventory will "burn down in the second half of this year," with management viewing the carrying cost as minimal against near-zero obsolescence risk.

Commodity Hedging Limiting Cost Exposure

Lennox's 2.5% cost inflation guide has drawn scrutiny given double-digit commodity price increases. Quenzer broke down the math:

- 20% of ~$3B cost of goods sold is commodities

- Half of that (steel) is locked in via fixed contracts

- A third (aluminum) is hedged 18 months out

- The remainder (copper) is being actively reduced through product redesign

"Procurement team have done a really great job moving away from copper. It would've been a significant headwind to this organization had we not done that," Quenzer said.

What to Watch: March 4 Investor Day

Lennox will host its 2026 Investor Day on March 4 in Dallas-Fort Worth, featuring presentations from CEO Alok Maskara, CFO Quenzer, CTO Bedapudi, and segment presidents. The event will include optional facility tours of customer training, product development, and distribution facilities.

Bedapudi teased upcoming announcements: "We're pretty excited about now that we're on the other end of the A2L transition... all our technology organization is working on having a full portfolio of heat pump products."

Key areas to watch:

- Long-term growth targets

- Heat pump portfolio expansion details

- Smart thermostat and IoT ecosystem progress

- Commercial electrification products for national accounts

The Bottom Line

Lennox is navigating the final innings of a difficult destocking cycle with its margin structure intact—FY2025 segment margins hit a record 20.4% despite volume headwinds.

The January "okay" commentary, while hardly euphoric, represents the first hint of stabilization after a Q4 that saw 11% revenue declines. With inventory cleared, the R-454B transition behind, and failure demand building from systems installed during the pre-pandemic era, Lennox is positioned for the volume recovery—whenever it arrives.

The March 4 Investor Day should provide clarity on whether the company can convert this positioning into sustainable market share gains.

Related