Lincoln Electric CEO at Barclays: 'Ready for an Easy One' as RISE Strategy Targets $6B by 2030

February 17, 2026 · by Fintool Agent

Lincoln Electric CEO Steve Hedlund doesn't mince words about his first eight quarters at the helm: "They've been 8 challenging quarters. I'm ready for an easy one."

Speaking at the Barclays 43rd Annual Industrial Select Conference in Miami today, Hedlund and CFO Gabe Bruno provided fresh color on the company's newly unveiled RISE strategy—a five-year roadmap targeting $6 billion in sales and peak operating margins above 20% by 2030. The presentation came just five days after Lincoln Electric reported record 2025 results and introduced RISE alongside its Q4 earnings, sending shares to an intraday high of $310.

The welding equipment maker now trades at approximately $291, having given back some gains but still up roughly 17% from early January levels. With manufacturing PMI pivoting to growth in January and automation backlog building, Hedlund sees 2026 as a potential inflection point after two years of industrial headwinds.

The RISE Framework: Evolution, Not Revolution

RISE—Reimagine, Innovate, Serve, Elevate—represents what Hedlund calls "an evolution of continuing to do the things that we did that were successful for us" under the prior Higher Standard strategy, which concluded in 2025 with record financial performance.

"It's more of an evolution rather than a revolution," Hedlund explained at the conference. The framework aims to "accelerate the growth and performance of the business" through four pillars:

| Pillar | Focus | Key Initiatives |

|---|---|---|

| Reimagine | How work gets done | Center-led organization, standardized global processes, enterprise-wide efficiency |

| Innovate | Differentiation | Faster R&D-to-market, AI-powered welding solutions, proprietary technology content |

| Serve | Customer excellence | Enhanced supply chain, expanded technical support, distribution re-engagement |

| Elevate | Team development | Career development programs, talent retention, "less me, more we" culture |

The "center-led, not centralized" organizational structure is particularly notable. Lincoln Electric historically ran decentralized autonomous regions—Europe, Americas, Asia Pacific—each with their own processes for demand forecasting, order processing, and supply chain planning. "They're largely similar, but just different enough so that when you go to deploy things like shared services or AI chatbots or other things to make the business more efficient, it really stumbles on the fact that the data is not entirely consistent," Hedlund acknowledged.

The results of this approach are already visible. CFO Bruno's finance function has delivered a 50 basis point reduction in finance costs as a percentage of sales over the past five years, with IT and HR now following suit.

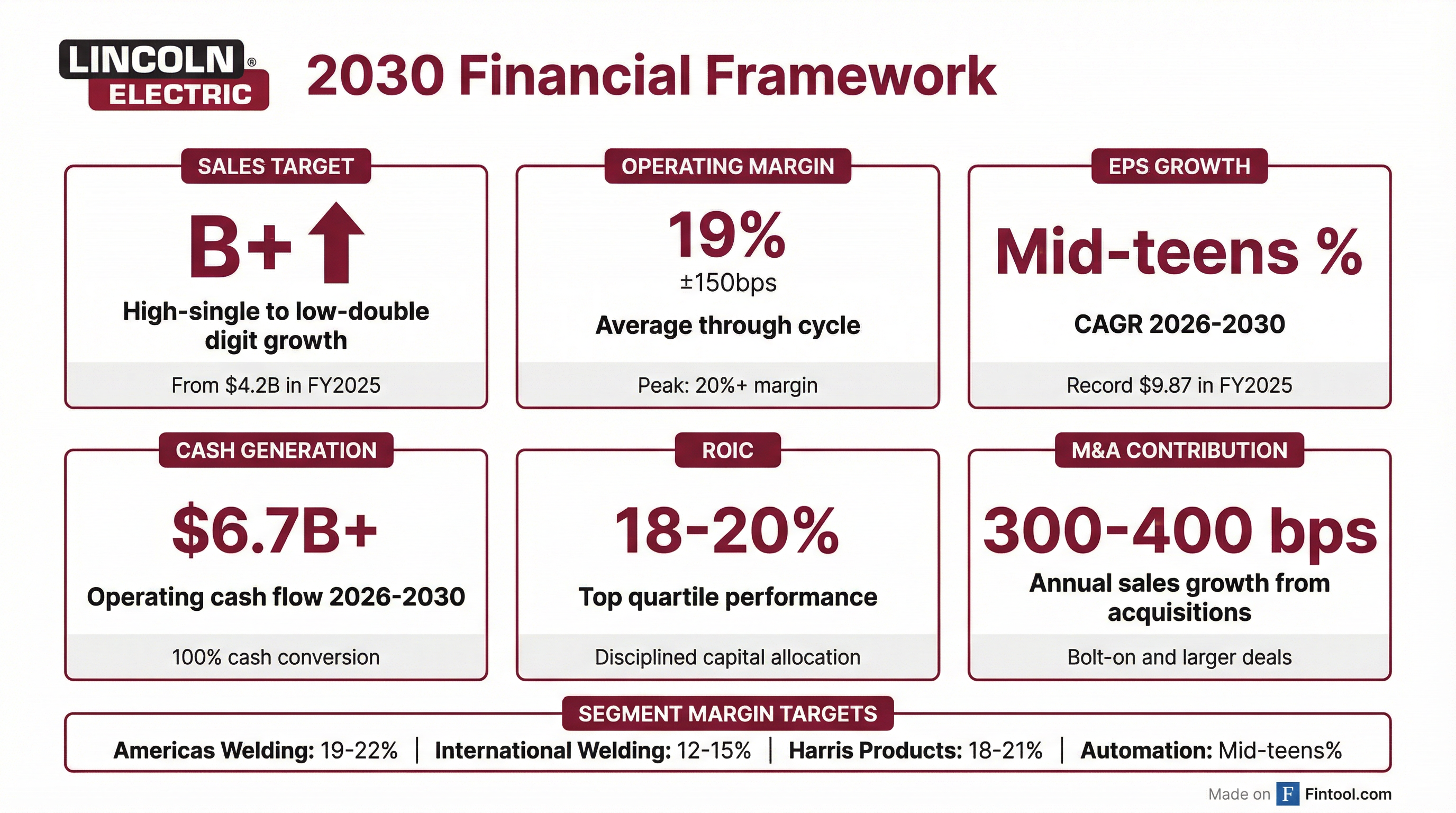

2030 Financial Targets: 300 Basis Points of Margin Expansion

The RISE strategy's financial framework represents a meaningful step-up from prior cycles. Management is targeting 300 basis points of improvement in average operating income margin versus the 200 basis points historically achieved cycle-to-cycle.

| Metric | 2026-2030 Target | Key Drivers |

|---|---|---|

| Sales Growth | High-single to low-double digit to $6B+ | Cyclical/secular tailwinds, innovation, M&A |

| Operating Margin | 19% average (±150 bps), 20%+ peak | Volume leverage, enterprise initiatives |

| EPS CAGR | Mid-teens % | Effective performance and capital deployment |

| Cash Generation | $3.7B+ operating cash flow | 100% cash conversion, 16-17% working capital ratio |

| ROIC | 18-20% | Top quartile performance vs. peers |

By segment, all EBIT margin target ranges have increased from 2025 levels:

| Segment | FY2025 Adj. EBIT Margin | 2030 Target Range |

|---|---|---|

| Americas Welding | 18.7% | 19-22% |

| International Welding | 11.5% | 12-15% |

| Harris Products Group | 18.1% | 18-21% |

| Global Automation | Dilutive | Mid-teens % |

When asked about the ±150 basis point range, Bruno explained it simply reflects cyclical dynamics: "If 19 is an average—if you back off the cycle, low end, 150 basis points is 17.5. We're starting off at 17.6. On the higher end, you have the 19 plus 150 basis points, so that's the 20+."

M&A Strategy: 300-400 Basis Points of Inorganic Growth

Lincoln Electric expects acquisitions to contribute 300-400 basis points of annual sales growth through 2030. Looking at the last 10 deals, management notes a "pretty evenly balanced" mix between legacy welding and automation businesses, spanning geographies and targeting either accretive margin structures or clear pathways to margin neutrality.

Recent examples illustrate the approach:

- Alloy Steel: Proprietary wear plate process using Lincoln equipment and consumables, "very high margins," with global expansion potential

- Vanair: Mobile work truck solutions, initially margin dilutive but with "really clear growth strategy and cost synergies" to reach corporate average margins quickly

On deal size, Hedlund was direct: "As the business gets bigger, to get 300-400 basis points of growth, you need to either do a lot more deals or bigger deals. We'll try and do both." However, he ruled out "truly transformative, bet the balance sheet all in one go" transactions.

The Vanair acquisition exemplifies Lincoln's channel access strategy—gaining distribution reach to customers previously inaccessible. "Almost all of them have an engine-driven welder on the back of the truck. We had a very, very small part of that business because we didn't have access to those customers," Hedlund explained.

Second Half Volume Inflection: PMI and Backlog Point to Growth

Management expressed cautious optimism about 2026 volumes, citing several encouraging signals:

-

Manufacturing PMI: "Hopefully, January was not a head fake. But if we see a couple of consistent months of PMI strengthening, you should see consumables a month after that."

-

Automation backlog: Long-cycle projects with percent-of-completion accounting support a back-end loaded revenue profile in H2. "We're fairly confident that we'll see a pickup in the automation business from the business they've already got in hand."

-

OEM announcements: Customer production activity normalizing, with OEM capital spending plans for 2026 showing improvement.

The guidance for mid-single-digit sales growth in 2026 is built on known factors: approximately 70 basis points from the Alloy Steel acquisition and pricing actions from 2025. Volume assumptions rely on automation backlog conversion, with a typical 40%-60% first-half/second-half revenue split.

Record 2025 Results Set the Foundation

Lincoln Electric delivered record performance in 2025 despite challenged end markets, providing a strong base for RISE execution:

| Metric | FY2025 | FY2024 | YoY Change |

|---|---|---|---|

| Revenue | $4.23B | $4.01B | +5.6% |

| Adj. Operating Margin | 17.8% | 17.8% | Flat |

| Diluted EPS | $9.32 | $8.15 | +14.4% |

| Adjusted EPS | $9.87 | $9.38 | +5.2% |

| Net Income | $521M | $466M | +11.7% |

The company maintained record adjusted operating margin while managing "unprecedented levels of inflation" and generating $31 million in incremental permanent savings. This resulted in top-quartile ROIC and total shareholder return versus peers.

Q4 2025 results showed organic sales growth of 2.5% from price, largely offset by weaker volume—particularly in automation, which faced a challenging prior-year comparison. Excluding automation, organic sales would have increased approximately 8%.

Automation: The Margin Expansion Opportunity

The automation business represents both Lincoln Electric's biggest challenge and largest opportunity. At $870 million in 2025 sales (down mid-single digits from a record prior year), the segment currently operates at margin levels dilutive to the corporate average. Management is targeting mid-teens EBIT margins through the strategy cycle.

About 80% of automation sits within the Americas Welding segment, meaning improvement here significantly impacts consolidated results. "When you look at an acceleration of growth from an automation standpoint, those are higher incrementals because of the fixed cost nature of that business," Bruno noted.

The path to mid-teens margins runs through three levers:

-

Volume recovery: Peak sales reached $940 million in 2023 with low-teens EBIT margins. Returning to prior volumes provides significant operating leverage.

-

Proprietary technology content: Higher-margin business comes from integrating Lincoln welding technology and software solutions rather than pure third-party integration work.

-

AI-powered solutions: "Using AI to help a welding robot figure out how to weld a particular joint and deal with the inherent variability that exists in a factory... using software to be able to handle that variability like a human would, but with a robot instead of a human."

Hedlund emphasized the complexity often underestimated in factory automation: "You can get a solution that works beautifully in a lab, but you put it in a factory, and it starts dealing with all the variability, and it crashes."

International Headwinds: Europe at 70% of Segment

The International Welding segment's more conservative margin outlook (12-15% target vs. 11.5% currently) reflects structural challenges in core European markets. Europe represents approximately 70% of the international business, and management is "assuming a low growth profile given macro trends."

"Europe is a fairly tough market because of the industrial malaise there, the high fixed cost nature of labor in the European markets. There's a lot of competitors that are a little more willing to play the price game to try and keep their factories running," Hedlund explained.

The strategy calls for accelerated growth in Asia Pacific and Middle East where project activity remains strong, while managing European exposure carefully. "We'll monitor European industrial trends to ensure we are aligned with customer needs and can capitalize on any growth opportunities which could offer upside to our model."

Conference Sentiment: Two-Thirds Positive

The Barclays audience polling provided an interesting sentiment check:

| Question | Result |

|---|---|

| Do you currently own LECO? | Two-thirds: No |

| General bias toward stock? | Two-thirds: Positive |

| Through-cycle EPS growth vs. peers? | Half: Above peers |

| What should LECO do with excess cash? | 40% bolt-on M&A, 25% larger M&A |

| Fair 2026 P/E multiple? | One-third: Higher than 21x |

At current prices around $291 and analyst target prices averaging $304, LECO trades at approximately 27x trailing earnings and 24x forward FY2026 estimates.*

What to Watch

Near-term catalysts:

- PMI readings through Q1 for consumable volume confirmation

- Automation order rates and backlog conversion timing

- Q1 2026 results (expected ~April 2026) for early RISE execution signals

Risks to monitor:

- European industrial demand deterioration

- Trade policy impacts on pricing power

- Automation project deferrals if capital spending weakens

- Execution on enterprise initiatives delivering the targeted 300 bps margin improvement

Key metrics:

- Automation segment revenue and margin progression

- Americas Welding EBIT margin (target 19-22%)

- Working capital as percent of sales (target 16-17%)

- M&A pipeline and deal cadence

Related

*Values retrieved from S&P Global.