Mama's Creations Targets Mid-Teens EBITDA and 100% Branded Sales Jump at 2026 Investor Day

February 24, 2026 · by Fintool Agent

Mama's Creations (NASDAQ: MAMA) shares surged 8% to a 52-week high of $17.41 during today's Investor Day as management unveiled aggressive FY2027 targets: double-digit organic revenue growth, gross margins climbing to the mid-to-high 20s, and adjusted EBITDA reaching the mid-teens by year-end. The $700 million market cap deli prepared foods company also announced a transformational shift to No Antibiotics Ever (NAE) chicken across all products—a move CEO Adam Michaels called "a moat" against competitors.

The presentation, hosted at MAMA's East Rutherford, NJ headquarters during a blizzard ("3 for 3" on snowstorms at investor days, Michaels joked), showcased the company's evolution from a single-facility meatball maker to a "one-plant, three-location" deli solutions platform now targeting $1 billion in revenue.

FY2027 Financial Framework

CFO Anthony Gruber laid out specific margin targets that represent a meaningful step-up from current performance:

| Metric | FY2027 Target | Current (Q3 2026) |

|---|---|---|

| Revenue Growth | Double-digit organic | 50% YoY (20% organic) |

| Gross Margin | Mid-to-high 20s % | 23.6% |

| Operating Expenses | 20% of sales (ex-marketing) | 21.8% |

| Net Income Margin | Mid single-digits % | 1.1% |

| Adjusted EBITDA | Mid-teens % (by year-end) | 8.0%* |

*Values retrieved from S&P Global

Management clarified that mid-teens EBITDA is an exit-rate target, not a full-year average. "It will start in the low double-digits and glide" to mid-teens by Q4 FY2027, Gruber explained.

Tier-1 Retail Wins Drive Distribution Momentum

Chief Commercial Officer Chris Darling unveiled a slate of major retail wins that significantly expand MAMA's distribution footprint:

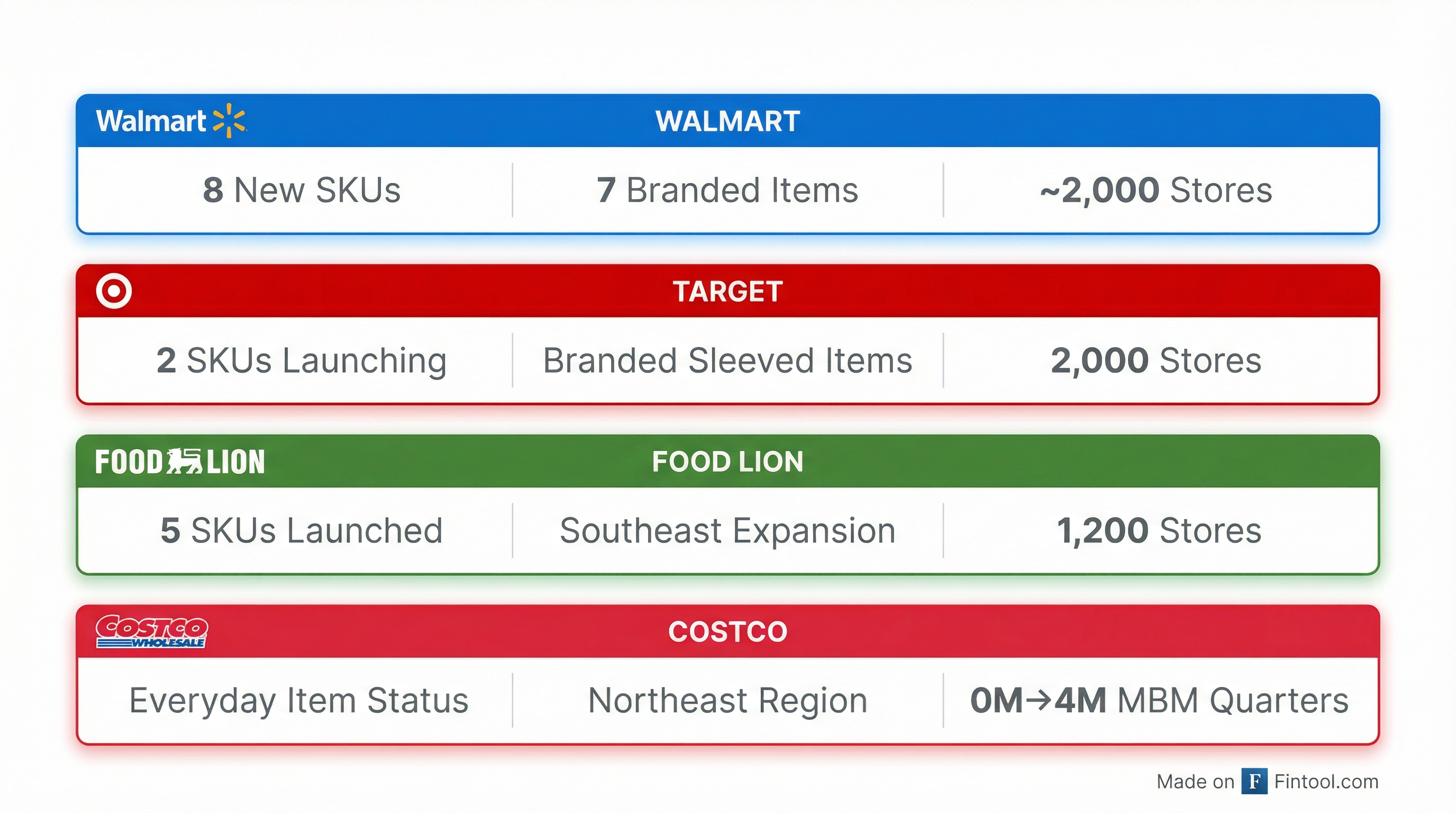

Walmart: 8 new SKUs across ~2,000 stores — This is "massive," Darling emphasized, as it represents an 8x expansion from just one item previously. Seven of the eight items are branded, with the first having already launched this quarter.

Costco: Everyday item status secured — MAMA's journey at Costco illustrates the company's patient approach to strategic selling:

- FY2023: $500K in sales, 1 product, 1 region

- FY2025: $10M in sales with rotations nationwide

- Q1 FY2026: First digital MVM, matching prior year's total in one quarter

- Q4 FY2026: First print MVM exceeding $14M

- FY2027: Everyday item status in the Northeast

"Getting everyday status has been an evolution over time," Darling said. "We delivered in very challenging situations... That builds trust."

Target: 2 branded SKUs launching this quarter in 750 stores, expanding to ~2,000 stores.

Food Lion: 5 SKUs launched in Q4 across approximately 1,200 stores in the Southeast.

NAE Chicken: The Competitive Moat

Perhaps the most strategically significant announcement was MAMA's transition to No Antibiotics Ever (NAE) chicken across all products. Michaels interrupted Darling's presentation to emphasize the importance:

"Guys, remember I said three things. That is one that you should be writing down... This creates a moat against other players that are not doing that today. It makes the job easier for Chris as he's selling in. This is a really big deal."

NAE chicken costs approximately $0.10-$0.15 more per pound on spot markets, but MAMA's scale from the Crown I acquisition—which nearly doubled chicken volume needs—enabled contracted pricing that mitigates the premium.

"It's just who we're going to be," Darling explained. "If you're buying our chicken, by the way, it's all NAE now."

Crown I Integration Unlocking Synergies

COO Skip Tappan provided an update on the $17.5 million Crown I acquisition completed in September 2025, which added a 42,000 sq ft Bayshore, NY facility and $56.8 million in trailing revenue:

Integration highlights:

- 100% of Bayshore suppliers integrated into MAMA network within months

- Beef costs reduced double-digits in the first month through procurement scale

- NetSuite ERP conversion expected by mid-FY2027

- Cross-selling underway between Crown I and legacy customer bases

"In three short months, you can no longer see where one plant begins and the other ends," Michaels said during the Q3 earnings call.

The "one-plant, three-location" strategy enables MAMA to move production between East Rutherford, Farmingdale, and Bayshore facilities based on capacity and efficiency. Management estimates 50% capacity expansion is achievable without new capital spending through schedule optimization and industrial engineering improvements—potentially up to 100% with modest capital investment.

Chicken Trimming: The Margin Engine

A key gross margin driver is MAMA's expansion of in-house chicken trimming and "artisan cut" utilization. When trimming chicken breasts, the "bottom" pieces are repurposed into meatballs, shredded chicken, strips, and paninis—eliminating waste and reducing dependence on expensive pre-trimmed chicken.

Usage of chicken bottoms will more than double in FY2027. Two-thirds of trimming capacity resides at Bayshore, with the product then distributed to Farmingdale and East Rutherford.

"The more we trim chicken ourselves and tumble it and then marinate ourselves, that's one of the biggest gross margin unlocks that we have," Tappan explained.

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue ($M) | $47.1 | $93.2 | $103.3 | $123.3 |

| Gross Margin | 24.9%* | 20.8% | 29.4% | 24.8% |

| Net Income ($M) | $(0.3)* | $2.3 | $6.6 | $3.7 |

*Values retrieved from S&P Global

Marketing Investment Rising 50%

CMO Lauren Sella outlined plans to increase marketing spend 50% in FY2027, with a target of 100% growth in branded sales.

The investment focuses on three phases of the shopper journey:

- Awareness: Influencer partnerships, digital/social ads, earned media, PR

- Shopper mindset: Retail media, Instacart advertising, search optimization

- In-store: Trade promotions, demos, displays, point-of-sale

Retail media investment doubled in FY2026, generating an $8+ return on ad spend across four new retailers.

"The number one trial generator is 'brand I trust,'" Sella noted, citing recent consumer research. "Which really supports our increase in marketing investment."

M&A Pipeline Active, But Integration First

Michaels was transparent about M&A priorities: the team has a "pipeline of not the deal next time, but the deal two times from now." However, organic growth—not acquisitions—drives the double-digit revenue target.

"I don't want to guarantee you. I do not put pressure on us to acquire a business every single year at all costs," Michaels said. "Inorganic growth has nothing to do with the algorithm."

Key acquisition criteria remain consistent: fair price, strategic alignment, operational synergy, and high confidence in integration.

What to Watch

Near-term catalysts:

- Q4 FY2026 results (fiscal year ends January 31, 2026)

- Walmart 8-SKU launch completion

- Target expansion to 2,000 stores

- Crown I gross margin improvement trajectory toward mid-20s

Risks:

- Beef commodity pressure (worst herd in 73 years, prices up 50%)

- Integration execution on Crown I ERP transition

- Private label concentration in Crown I portfolio requiring SKU rationalization

Related: Mama's Creations Company Profile