Nelson Peltz Signals Potential Wendy's Takeover, Shares Surge 13%

February 18, 2026 · by Fintool Agent

Wendy's stock soared as much as 15% on Wednesday after legendary activist investor Nelson Peltz declared the fast-food chain "currently undervalued" and disclosed talks with potential financing sources about taking control of the company—a dramatic turnaround from Tuesday, when shares hit a six-year low following dismal 2026 guidance.

The disclosure, buried in Trian Fund Management's 64th amendment to its Schedule 13D since 1992, sent WEN from $7.00 to above $8.00 in heavy morning trading. But for investors who have watched Wendy's shed half its value over the past year, the question is whether Peltz—who considered and rejected a take-private in 2022—will finally pull the trigger on a deal.

What the Filing Says

Trian's amended 13D is explicit about the range of options under consideration. The filing states that Peltz has "spoken with potential financing sources, potential co-investors and certain potential strategic partners" about "potential transactions in which such parties could participate that may benefit the Company's shareholders."

Crucially, the filing specifies these discussions include transactions that could result in "the Filing Person (and/or their affiliates), either alone or with other parties...acquiring control of the Company" and potentially "a de-listing or de-registration of the Company's Common Stock."

Trian now beneficially owns 31.1 million shares representing 16.33% of Wendy's outstanding stock—up marginally from 16.09% in July 2025. The filing notes that parties have entered confidentiality and standstill agreements, suggesting serious discussions are underway.

However, Trian included standard legal disclaimers: "There can be no assurance that any such proposals will be submitted...or that any transaction will result from any such discussions or proposals."

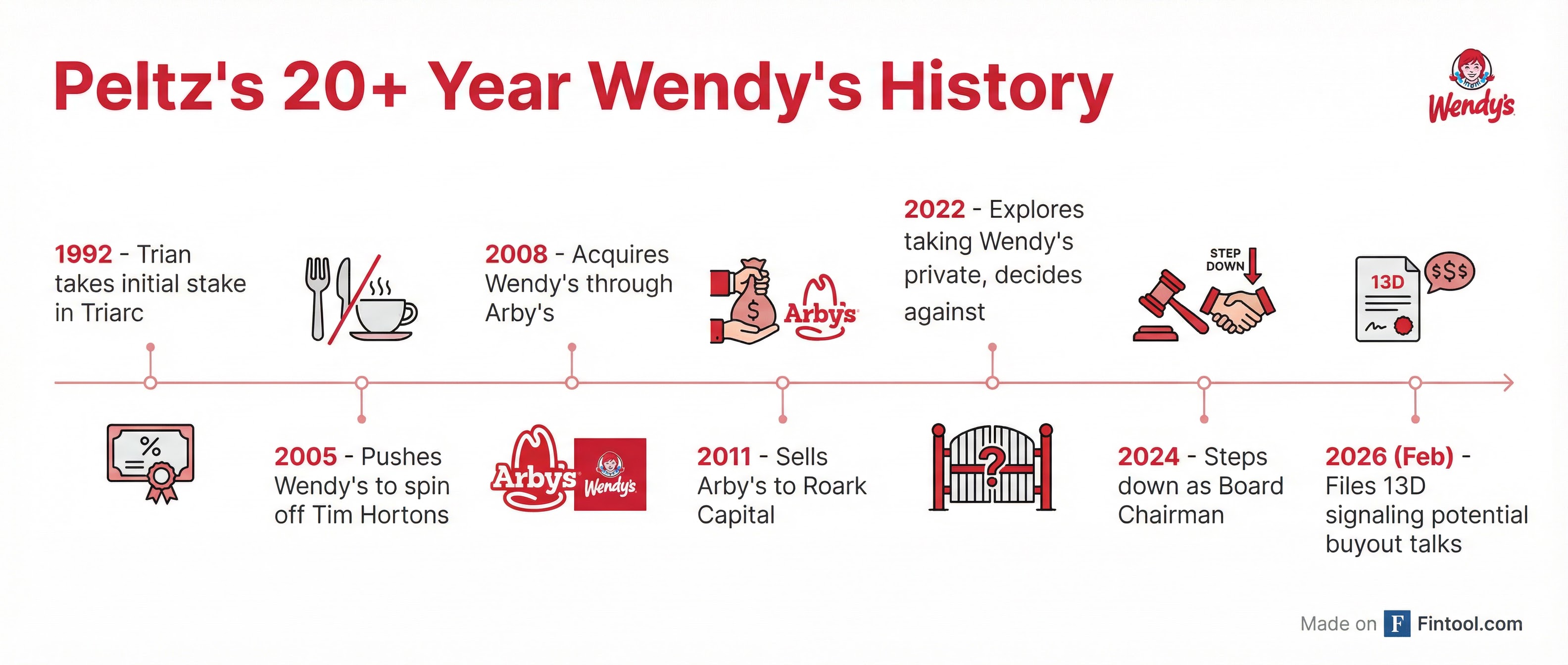

Peltz's Two-Decade Wendy's Saga

Peltz's involvement with Wendy's spans more than 30 years through a complex web of transactions:

- 1992: Trian takes initial position in Triarc Companies

- 2005: Pushes Wendy's to spin off Tim Hortons, unlocking shareholder value

- 2008: Acquires Wendy's through Arby's (which Trian controlled via Triarc)

- 2011: Sells Arby's to Roark Capital, keeping Wendy's

- 2022: Explores taking Wendy's private; decides against, opts for larger dividend

- 2024: Steps down as Board Chairman

- 2026 (Feb): Files 13D signaling renewed buyout discussions

This pattern of alternating between passive ownership and active involvement is classic Peltz. The question now is whether the current market dislocation finally creates the conditions for a deal.

The Valuation Case

At today's price around $8, Wendy's trades at roughly 11x forward earnings—a 55% discount to Mcdonald's (24.4x) and Yum Brands (23.7x).

The stock's collapse reflects genuine fundamental deterioration:

| Metric | Q4 2024 | Q4 2025 | Change |

|---|---|---|---|

| Revenue | $574.3M | $543.0M | -5.5% |

| Net Income | $47.5M | $26.5M | -44.2% |

| U.S. Same-Store Sales | -0.6% | -11.3% | -10.7 ppts |

The Q4 2025 results announced last week were ugly. U.S. same-restaurant sales plunged 11.3%, driven by a combination of reduced marketing spend and tough comparisons versus the prior year's SpongeBob collaboration. The 2026 outlook was even worse—EPS guidance of $0.56-$0.60 fell 34% below the Street's $0.85 estimate.

Project Fresh: The Turnaround Bet

Management unveiled "Project Fresh" on the Q4 call—a four-pillar turnaround strategy centered on brand revitalization, operational excellence, system optimization, and disciplined capital allocation.

Key elements include:

Brand Revitalization: A return to Wendy's roots as a quality-focused hamburger chain. CEO Ken Cook acknowledged the company "got away from what made us great" and had "zero hamburger innovation in 2025." New products launching include a Cheesy Bacon Cheeseburger, upgraded chicken sandwiches, and expanded Biggie Deals value menu at $4/$6/$8 price points.

Operational Excellence: Company-operated restaurants outperformed the broader system by 310 basis points in 2025, proving the playbook works. Management is now deploying these initiatives—enhanced training, performance management, field team expansion—to franchisees. Currently, 20% of franchisees have fully adopted the program.

System Optimization: Approximately 5-6% of U.S. restaurants will close, including 28 that shuttered in Q4 2025, with remaining closures expected in H1 2026. Breakfast hours are also being scaled back in underperforming markets.

The $15-20 million drag on EBITDA from system optimization may be a short-term headwind, but the moves are necessary medicine for a system that had allowed unit-level economics to deteriorate.

The Take-Private Math

At a $1.4 billion market cap, Wendy's is a digestible target. But the math gets complicated:

Balance Sheet: Wendy's carries approximately $4.1 billion in total debt against FY2025 EBITDA of roughly $500 million, implying leverage around 8x. The company refinanced $450 million in securitization notes in Q4 at 5.4% weighted average rate. A take-private would likely require paying down this debt or rolling it into a new capital structure.

Franchise Model: Wendy's is primarily a franchisor—around 95% of restaurants are franchised—which complicates any deal. Franchisee consent isn't required, but franchisee health is critical to any financial sponsor's underwriting.

Strategic Premium: Restaurant deals typically command 25-40% premiums. A 35% premium to today's ~$8 price implies roughly $10.80—still well below the $16+ levels from early 2025.

| Scenario | Premium | Deal Price | Enterprise Value |

|---|---|---|---|

| Low | 25% | $10.00 | $5.9B |

| Base | 35% | $10.80 | $6.0B |

| High | 50% | $12.00 | $6.2B |

What Happens Next?

The filing is a clear shot across the bow, but several scenarios remain possible:

Scenario 1: Take-Private — Peltz assembles a consortium (likely with private equity) and makes an offer. Given the 16% stake, hostile isn't necessary—but a premium would be required to win Board and minority shareholder approval.

Scenario 2: Strategic Sale — Peltz finds a strategic acquirer. Restaurant Brands International (Burger King, Popeyes) or a well-capitalized restaurant platform could view Wendy's as a turnaround opportunity.

Scenario 3: Status Quo — Like 2022, Peltz decides the timing isn't right and remains a large, influential shareholder advocating for operational improvements.

Scenario 4: Partial Exit — The filing mentions Peltz could "dispose of all or a portion" of his stake. If no deal materializes and fundamentals don't improve, he could monetize his position.

For now, the market is betting on Scenario 1 or 2. The 13% stock jump prices in meaningful probability of a deal, but there's no guarantee Peltz will follow through.

Investment Implications

For current shareholders, the filing provides a near-term floor. Even if no deal emerges, Trian's 16% stake and public declaration that shares are undervalued creates a significant holder with aligned incentives to drive operational improvement.

For prospective investors, the risk/reward has shifted. The downside—back to pre-filing $7 levels if no deal materializes and fundamentals continue deteriorating—is meaningful. But the upside, particularly in a take-private at 35%+ premium, could be substantial.

The key variable is time. Peltz is 83 years old and stepped back from day-to-day Wendy's involvement in 2024. If he's going to make a move on a company he's been involved with for three decades, the window may be narrowing.

Related: