QuidelOrtho CEO, Retiring CFO, and Director Buy $568K in Stock After 18% Crash

February 16, 2026 · by Fintool Agent

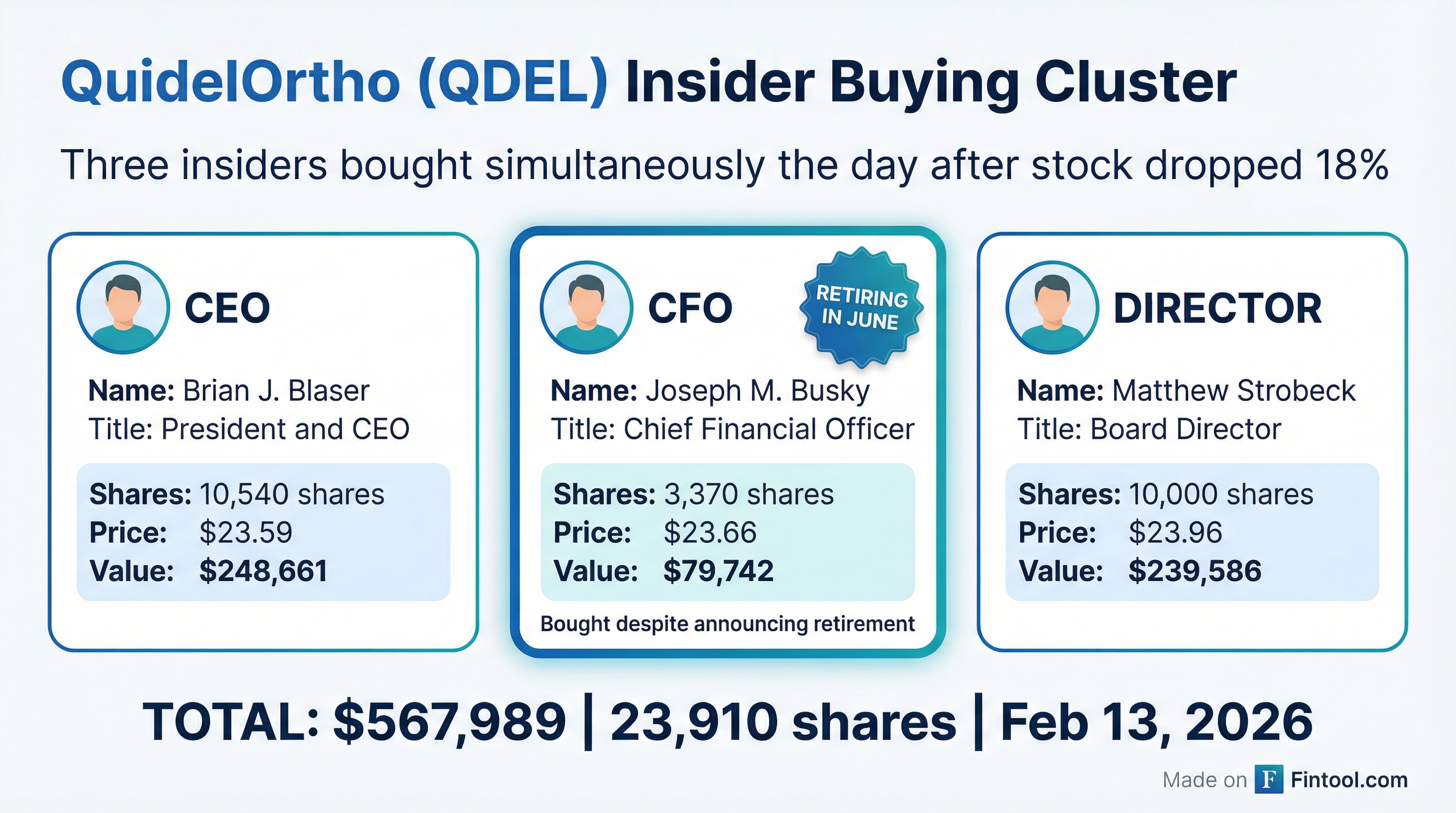

Quidelortho insiders are putting their money where their mouth is. One day after the diagnostics company's stock crashed 18% on disappointing free cash flow guidance, CEO Brian Blaser, retiring CFO Joseph Busky, and Director Matthew Strobeck collectively purchased nearly $568,000 worth of shares.

The coordinated buying—rare in both timing and scope—raises an obvious question: Do the people running this company see something the market missed?

The Numbers

On February 13, 2026, Form 4 filings revealed three simultaneous open-market purchases:

| Insider | Title | Shares | Price | Value |

|---|---|---|---|---|

| Brian J. Blaser | President & CEO | 10,540 | $23.59 | $248,661 |

| Joseph M. Busky | CFO (Retiring June 2026) | 3,370 | $23.66 | $79,742 |

| Matthew Strobeck | Director | 10,000 | $23.96 | $239,586 |

| Total | 23,910 | $567,989 |

The CFO purchase is particularly notable. Busky announced his retirement on the same earnings call that tanked the stock—yet he still bought shares. When a departing executive puts $80,000 of personal capital into a stock he's about to leave behind, it suggests genuine conviction rather than optics.

What Triggered the Crash

QuidelOrtho reported Q4 2025 results on February 11 that actually beat estimates:

| Metric | Actual | Estimate | Beat/Miss |

|---|---|---|---|

| Q4 EPS (Adj.) | $0.46 | $0.43 | Beat by 7% |

| Q4 Revenue | $723.6M | $699.8M | Beat by 3% |

But the forward guidance was the problem. Management's 2026 outlook shocked analysts:

| Metric | 2026 Guidance | Consensus | Gap |

|---|---|---|---|

| EPS | $2.00-$2.42 | $2.50 | Miss |

| Revenue | $2.7B-$2.9B | $2.77B | In-line |

| Free Cash Flow | $120-160M | ~$441M | Massive Miss |

The free cash flow miss was the killer. Analysts expected $441 million; the company guided to $140 million at the midpoint—a 68% shortfall. The stock gapped down from $28.80 to $23.74 on February 12, a single-day decline of 17.6%.

Management's Defense

On the earnings call, CEO Brian Blaser emphasized that the underlying business is performing well and that 2025 marked a successful transition from COVID-driven volatility to a "more durable, diversified diagnostics business."

Key points from management:

-

Labs business strength: The Labs segment grew 6% for the full year and now represents 55% of total revenue, demonstrating the stability of their recurring revenue model.

-

Cost savings delivering: The company generated $140 million in cost savings and expanded adjusted EBITDA margins by 240 basis points to 22%.

-

FCF timing issues: CFO Busky attributed part of the weak 2025 free cash flow to $15-20 million in ERP system issues and $20 million in Q4 sales that were collected in January 2026.

-

One-time cash uses: The 2026 FCF guide includes $50-60 million in one-time cash use for the New Jersey facility consolidation and procurement initiatives. Excluding these, recurring free cash flow would be approximately $200 million.

Perhaps most telling: management announced that executive compensation will now be directly tied to cash flow targets for the first time.

"Cash flow is a company-wide focus for us, including executive compensation incentives that will directly be tied to cash flow targets for the first time this year. So it's a major focus for the organization." — CEO Brian Blaser

Why This Matters

Insider buying clusters are among the most statistically significant signals in equity markets. When multiple executives buy simultaneously with their own money—not options exercises, not grants—it suggests:

-

Information asymmetry: Management knows the business better than anyone. If they believe the market overreacted, their personal capital is the most credible endorsement.

-

Misaligned expectations: The FCF miss looks dramatic in percentage terms, but management argues analysts had unrealistic models. The $441 million consensus was never achievable given the one-time restructuring costs baked into 2026.

-

Confidence in the turnaround path: Blaser outlined a clear roadmap to 25%+ EBITDA margins through donor screening exit (50-100 bps improvement mid-year), procurement savings, and the LEX Diagnostics acquisition.

The market is now pricing QuidelOrtho at roughly 10x 2026 EBITDA guidance ($650M midpoint), down from ~12x before earnings. For a healthcare company with a diversified diagnostics portfolio and margin expansion trajectory, that's a discounted multiple.

The Bear Case

Skeptics would note:

- CFO departure timing: Announcing retirement alongside weak guidance isn't ideal optics, regardless of personal stock purchases

- Leverage remains elevated: Net debt to EBITDA of 4.2x is above their 2.5-3.5x target range

- COVID hangover continues: Respiratory revenue declined 20% for the full year as COVID testing normalizes

- High short interest: ~15.4% of float was short before earnings, and shorts may continue pressing

The 52-week low of $19.50 is only 17% below current levels. If the FCF story doesn't improve, that technical support could be tested.

What to Watch

-

Q1 2026 results: Management expects second-half weighted cash flow, similar to 2025. The first quarter will be weak—watch for any upside surprise.

-

CFO succession: Finding a strong replacement for Busky will be critical for investor confidence. No timeline has been provided.

-

Donor screening exit: The U.S. Donor Screening wind-down should be substantially complete by mid-year. This removes a margin drag and should provide 50-100 bps improvement.

-

Lifotronic partnership: The company just announced a strategic supply agreement with Lifotronic Technology for global immunoassay portfolio expansion.

The Bottom Line

Three insiders bought $568,000 worth of QuidelOrtho stock the day after an 18% crash. The retiring CFO bought despite announcing his departure. The CEO bought despite being the face of disappointing guidance.

Either they're throwing good money after bad, or the market's reaction was excessive. History suggests that coordinated insider buying at distressed prices—especially by C-suite executives using personal funds—tends to precede outperformance.

At $23.58, the stock trades at its lowest level since mid-2024. The next few quarters will reveal whether management's confidence was warranted.

Related