Rio Tinto-Glencore Deadline Tomorrow: $260 Billion Mining Mega-Merger Hangs in Balance

February 4, 2026 · by Fintool Agent

Tomorrow at 5:00 PM London time, Rio Tinto must either announce a firm intention to acquire Glencore or walk away for six months—the climax of what could become mining's largest-ever transaction.

An extension request appears "highly probable" according to sources close to the discussions, but the situation remains fluid as the two sides wrangle over valuation, leadership, and the future of Glencore's controversial coal business.

The Stakes: World's Largest Miner

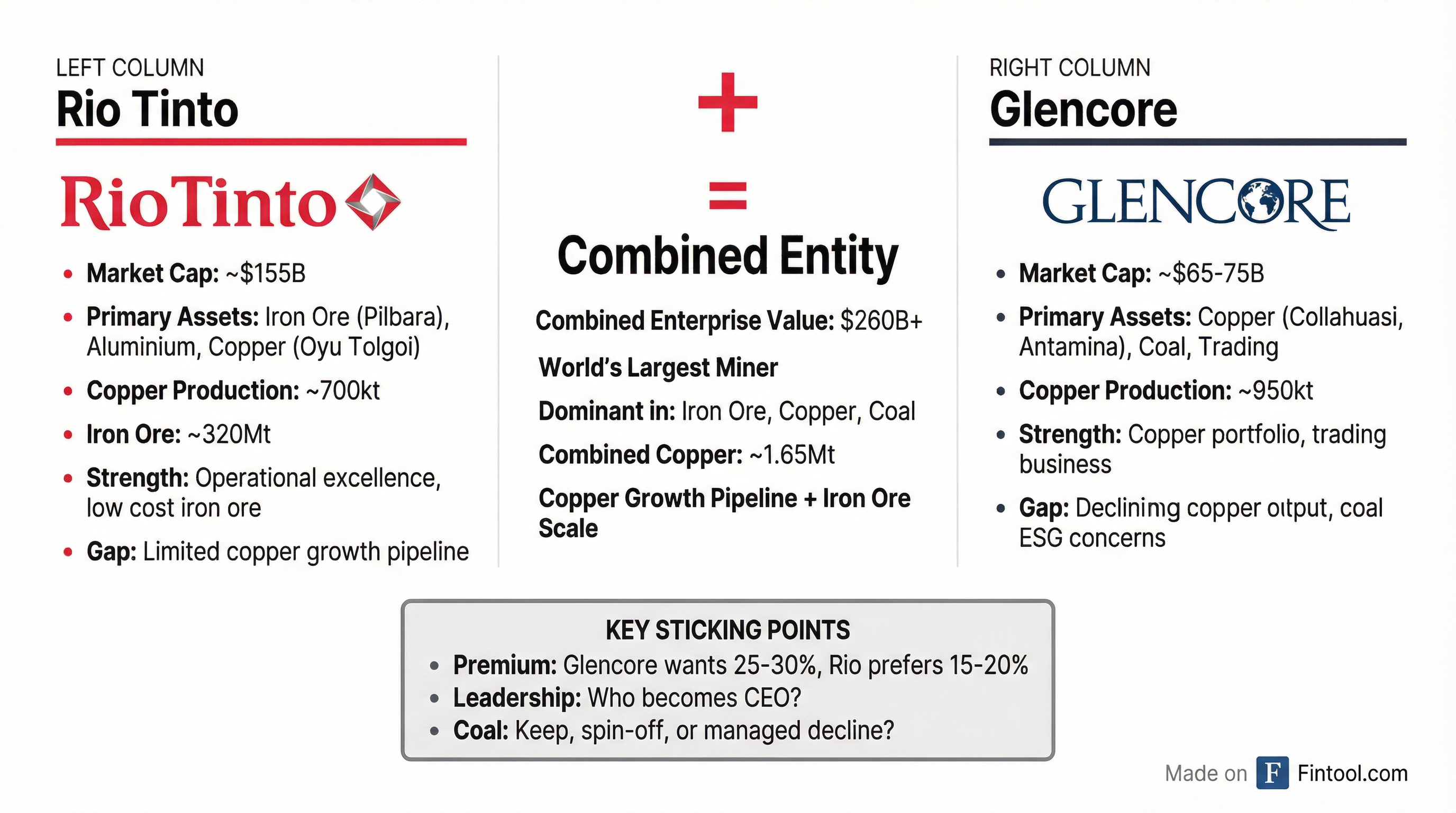

A combination of Rio Tinto and Glencore would create a mining colossus with a combined enterprise value exceeding $260 billion, surpassing BHP to become the world's largest diversified miner.

The deal's logic is straightforward: Rio Tinto would roughly double its copper production at a time when prices of the metal crucial for the energy transition recently hit a record $14,500 per ton—up 45% over the past year.

"A full combination would create a global leader in multiple industrial metals including iron ore and transition metals such as copper, cobalt and lithium," notes Derren Nathan, Head of Equity Research at Hargreaves Lansdown.

Leadership and Premium: The Sticking Points

Rio Tinto is pushing for its chairman and CEO to retain their roles in any merged entity, while Glencore is holding out for a hefty premium, according to the Financial Times.

The leadership question is particularly charged. Rio Tinto CEO Simon Trott, who took the helm in July 2025, is seen as more dealmaker-friendly than his predecessor. Meanwhile, Glencore CEO Gary Nagle—who has described a Rio-Glencore tie-up as "the most obvious deal in mining"—previously pushed to lead any combined company.

On valuation, Glencore has historically sought a merger ratio leaving its shareholders with about 40% of the combined company—implying a premium of over 25% to pre-announcement prices. RBC Capital Markets suggests a 15% to 30% premium, potentially valuing Glencore at up to $87 billion.

| Metric | Rio Tinto | Glencore | Combined (Est.) |

|---|---|---|---|

| Market Cap | $155B | $65-75B | $220-235B |

| Enterprise Value | $162B | $90-100B | $260B+ |

| Copper Production | 700kt | 950kt | 1.65Mt |

| Iron Ore Production | 320Mt | 50Mt | 370Mt |

Sources: Market data, analyst estimates

The Coal Question

A key shift in the negotiations involves Rio Tinto's apparent willingness to retain Glencore's vast coal business—a dramatic reversal for a company that divested all its coal assets by 2018 amid investor pressure over climate concerns.

Glencore is the world's biggest thermal coal shipper, and the commodity generates substantial cash flows that could fund copper growth. Sources indicate Rio would be open to keeping the coal business initially, potentially spinning it off later or managing its decline responsibly.

"Shifting investor attitudes toward coal mining means that Rio could buy Glencore outright with less fear of a backlash," Bloomberg reported.

Copper: The Real Prize

Glencore's copper assets are the strategic crown jewels. The company holds a 44% stake in the Collahuasi copper mine in Chile—a joint venture with Anglo American that investors view as exceptional.

Rio Tinto's copper growth pipeline, while solid at Oyu Tolgoi in Mongolia, offers limited upside beyond current development phases. Key projects like Resolution in Arizona remain mired in permitting battles.

"Rio has got a lot right in recent years developing Oyu Tolgoi and Simandou, but the growth beyond this current phase is far less exciting," notes RBC analyst Ben Davis. "Projects are either too small to make a difference or still stuck in courts."

The International Copper Study Group forecasts a global shortfall of up to 10 million tonnes by 2040, making securing copper reserves an urgent strategic priority for major miners.

Regulatory Gauntlet Ahead

Even if terms are agreed, any deal faces a formidable regulatory journey:

China's SAMR: As the world's largest consumer of iron ore and copper, Beijing will scrutinize how a merged entity could affect industrial commodity pricing.

Australian ACCC: Both companies have major operations in Western Australia and Queensland. Regulators will examine market concentration in iron ore logistics and coal.

European Union: Brussels will evaluate the deal's impact on Europe's access to critical minerals essential for clean energy manufacturing.

Rio Tinto's Financial Position

Rio Tinto enters negotiations from a position of strength:

| Metric | FY 2024 | FY 2023 |

|---|---|---|

| Revenue | $53.7B | $54.0B |

| Net Income | $11.6B | $10.1B |

| EBITDA | $19.1B | $19.5B |

| Total Debt | $14.2B | $14.9B |

| Cash | $8.5B | $9.7B |

| Capex | $9.6B | $7.1B |

Values retrieved from S&P Global

The company's low leverage and strong cash generation provide ample capacity for a transformative deal, though investor appetite for disciplined M&A will be tested.

Market Reaction

Rio Tinto's ADR (RIO) fell 3.1% on February 4 to $95.52, with shares having risen from ~$92 to ~$96 since merger talks became public in early January before pulling back today.

The divergent share price reaction—with Glencore up sharply since January 8 while Rio has been more muted—reflects market expectations that Rio will ultimately pay a premium.

What to Watch

February 5, 5:00 PM London: The formal deadline arrives. An extension request from Glencore appears likely, but "the situation remains fluid and could still change."

Premium Negotiations: Whether Rio can secure a deal at 15-20% rather than the 25-30% Glencore may seek will determine shareholder appetite on both sides.

Leadership Resolution: The CEO and chairman roles must be settled before any announcement—a historically sensitive issue in mega-mergers.

Australian Shareholders: Rio's Australian investors, who own roughly 20% of the company, are viewed as more conservative on deals. Keeping them onside is critical.

Related Companies