Sky Harbour Eliminates Dilution Risk With Innovative $350M Bond Structure

February 5, 2026 · by Fintool Agent

SKY Harbour Group has solved its equity financing problem. The business aviation hangar developer detailed an innovative capital structure at Noble Capital Markets' Emerging Growth Virtual Equity Conference today that eliminates the need for dilutive stock issuance through 2027 and beyond—a critical development for a stock that has fallen 38% from its 52-week high.

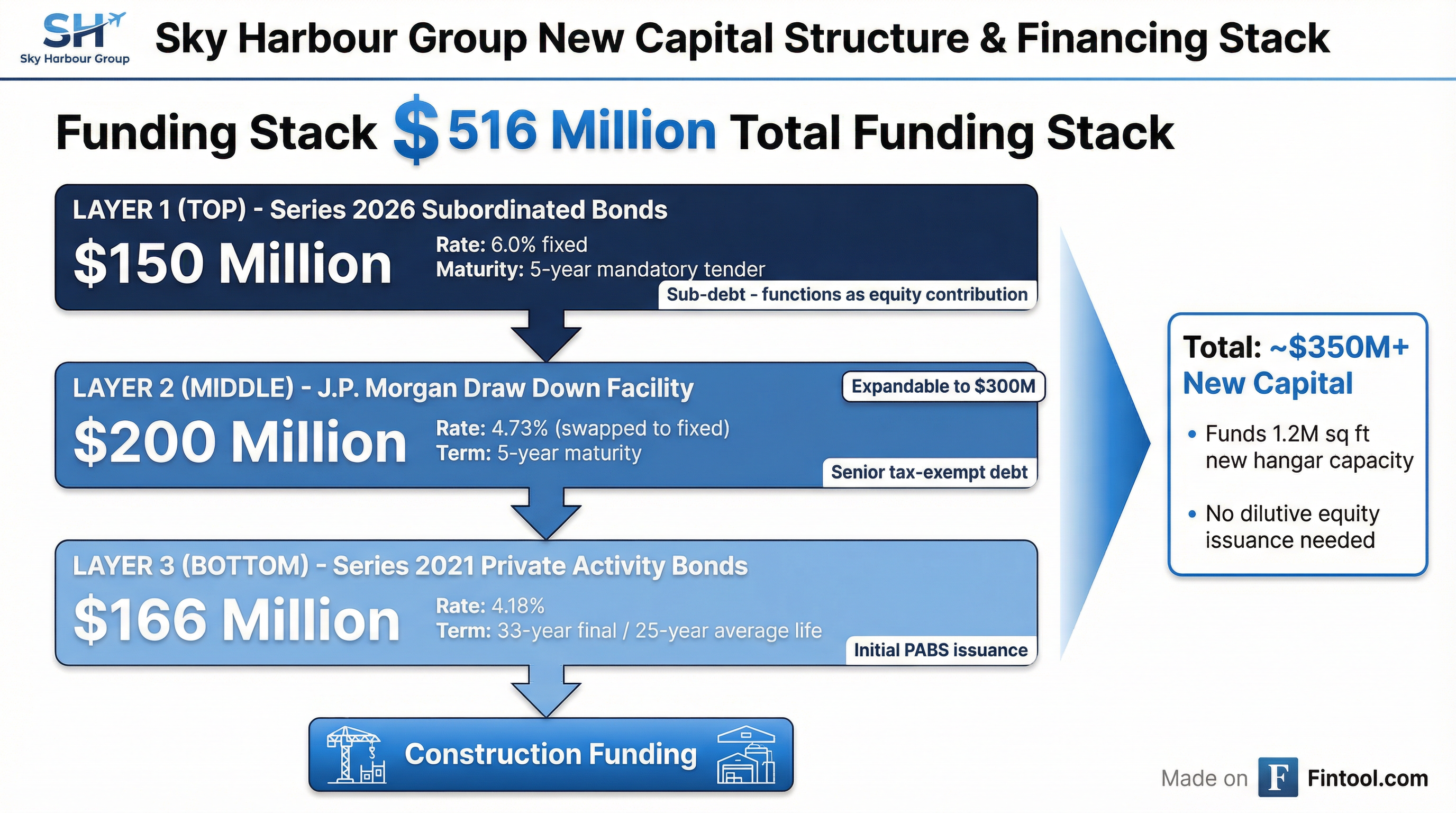

The company priced $150 million in subordinated municipal bonds at 6% last week, upsized from an initial $100 million target after receiving $450 million in orders from 18 institutional investors. These proceeds function as equity contribution into a $200 million J.P. Morgan draw-down facility locked in at 4.73%, giving Sky Harbour over $350 million in construction capital without tapping public markets.

"This sub-debt structure is pretty transformative for the business," Treasurer Tim Herr told investors at the conference. "It takes the pressure off the next couple of years to raise equity."

The Financing Innovation

Sky Harbour's breakthrough lies in using tax-exempt private activity bonds in a layered structure that dramatically reduces cost of capital:

The J.P. Morgan facility requires 65% debt paired with 35% equity contribution. Rather than issue stock at what management considers depressed prices, Sky Harbour structured the subordinated bonds to satisfy this equity requirement at just 6%—far cheaper than diluting shareholders at today's $8.79 share price.

"Shareholders should be excited about this because we can avoid the dilution by issuing that very competitive sub-debt at 6%," Herr said.

The combined $350 million+ in new capital will fund over 1.2 million rentable square feet of new hangar capacity at airports including Bradley International (BDL), Salt Lake City (SLC), Orlando Executive (ORL), Dulles International (IAD), and several others—more than doubling the company's current footprint.

EBITDA Break-Even Achieved

The conference presentation also confirmed a major inflection point: Sky Harbour reached EBITDA break-even this quarter.

"We're essentially on an EBITDA basis, as of this quarter, now break even," Herr stated. "As we finish construction at airfields this year... that will just be not break even on an EBITDA basis, but positive EBITDA and continue to grow from there."

This milestone comes as the company's consolidated revenues grew 78% year-over-year in Q3 2025, reaching $7.3 million for the quarter. The Sky Harbour Capital obligated group—covering the Houston, Miami, Nashville, Phoenix, Dallas, and Denver campuses—saw revenues increase 25% year-over-year.

Unit Economics: The Bull Case

Herr provided detailed unit economics that explain why Sky Harbour believes it can generate outsized returns:

| Metric | Per Sq Ft |

|---|---|

| Hangar Rent | $40 |

| Fuel Sales | +$5 |

| Total Revenue | $45 |

| Ground Lease | ($2-4) |

| Personnel & Other | ($4-5) |

| NOI | $35-37 |

With construction costs averaging $300/sq ft (including $250 hard costs and $50 soft costs), this translates to low-to-mid-teen NOI yields on cost. Paired with tax-exempt debt at 4-6%, management targets return on equity in the 20-30% range.

"The cheaper we can build to the spec we want—we still have high standards—but the cheaper we can build, the better it is going to be for our equity holders," Herr emphasized.

The Business Aviation Tailwind

Sky Harbour's investment thesis rests on a persistent supply-demand imbalance in business aviation hangar space. The square footage of the U.S. business aviation fleet is growing annually—driven by both longer aircraft lifespans and new deliveries of larger aircraft that require more hangar space.

Yet hangar development has not kept pace. Most airports are owned by municipalities reluctant to spend taxpayer dollars on "storage for rich people's aircraft," as Herr put it. The legacy Fixed Base Operators (FBOs) that service airports focus on fuel sales—their primary revenue driver—and build only the minimum required hangar space.

Sky Harbour's founder, Tal Keinan, identified this gap a decade ago when he couldn't find hangar space for his own aircraft. The company now positions itself as a "Home Base Operator," distinguishing from FBOs by exclusively serving based residents rather than visiting aircraft—offering greater privacy and security.

Expansion Roadmap

The company currently has ground leases at 23 airports, with its newest at Fort Worth Meacham announced in recent months. Nine campuses are operating, with construction underway at multiple sites including a phase two at Miami-Opa-locka expected to open in April, phase two at Addison Airport in Dallas, and phase one at Bradley International in Connecticut.

Management's long-term target is 50+ airports.

"We're targeting tier-one airports, and we want to be in the best 30-40 airports in the country before we have robust competition," CEO Tal Keinan said on the Q3 earnings call.

The focus on high-revenue locations makes strategic sense: while construction costs vary within a tight range nationwide, rents can differ dramatically by market. Premium locations like South Florida, Southern California, and the Northeast command significantly higher rates.

No Dividend on the Horizon

Investors hoping for income will need to wait. Management was explicit that all internally generated cash flows will be reinvested into growth for the "foreseeable future."

"It's a CapEx heavy business. As we turn cash flow positive, the best use of our capital is retaining internally and using that—they call it the flywheel—plowing it back into these high-yielding assets," Herr said.

The eventual end state is REIT status and dividend payments, but only when growth slows or attractive airports become scarce.

Stock Under Pressure

Despite the operational progress, SKYH shares have struggled. The stock closed at $8.79 today, down 2% on the session and 38% below its 52-week high of $14.20. Shares trade 4.5% below the 50-day moving average of $9.21 and 12% below the 200-day average of $9.99.

Construction cost inflation remains the primary investor concern. Development costs have risen from under $200/sq ft for early projects to the current $300/sq ft target—a 30-50% increase.

"That's not unique to us. This is kind of a post-COVID, 2021, 2022 phenomenon," Herr acknowledged. The company has responded by vertically integrating—owning a hangar manufacturing facility in Weatherford, Texas and bringing on an internal general contractor—to drive costs lower.

What to Watch

Near-term catalysts:

- Q4 2025 earnings expected in early March, with updated guidance

- Miami Opa-locka Phase 2 opening (~April 2026)

- Bradley International Airport phase one completion (late 2026)

- Investment grade rating pursuit expected mid-2026

Key metrics to monitor:

- Revenue per rentable square foot by campus

- Lease-up velocity at new campuses (Phoenix, Dallas, Denver)

- Construction cost per square foot trends

- Occupancy rates, particularly semi-private vs. private space

The subordinated bond pricing and J.P. Morgan facility represent a significant de-risking of Sky Harbour's capital structure. Whether that translates to stock appreciation depends on execution—delivering hangars on time and on budget, then leasing them up at target rents.

Related: