Triple Flag CEO Maps 45% Production Growth at BMO Conference as Northparkes Transforms into Gold Growth Engine

February 24, 2026 · by Fintool Agent

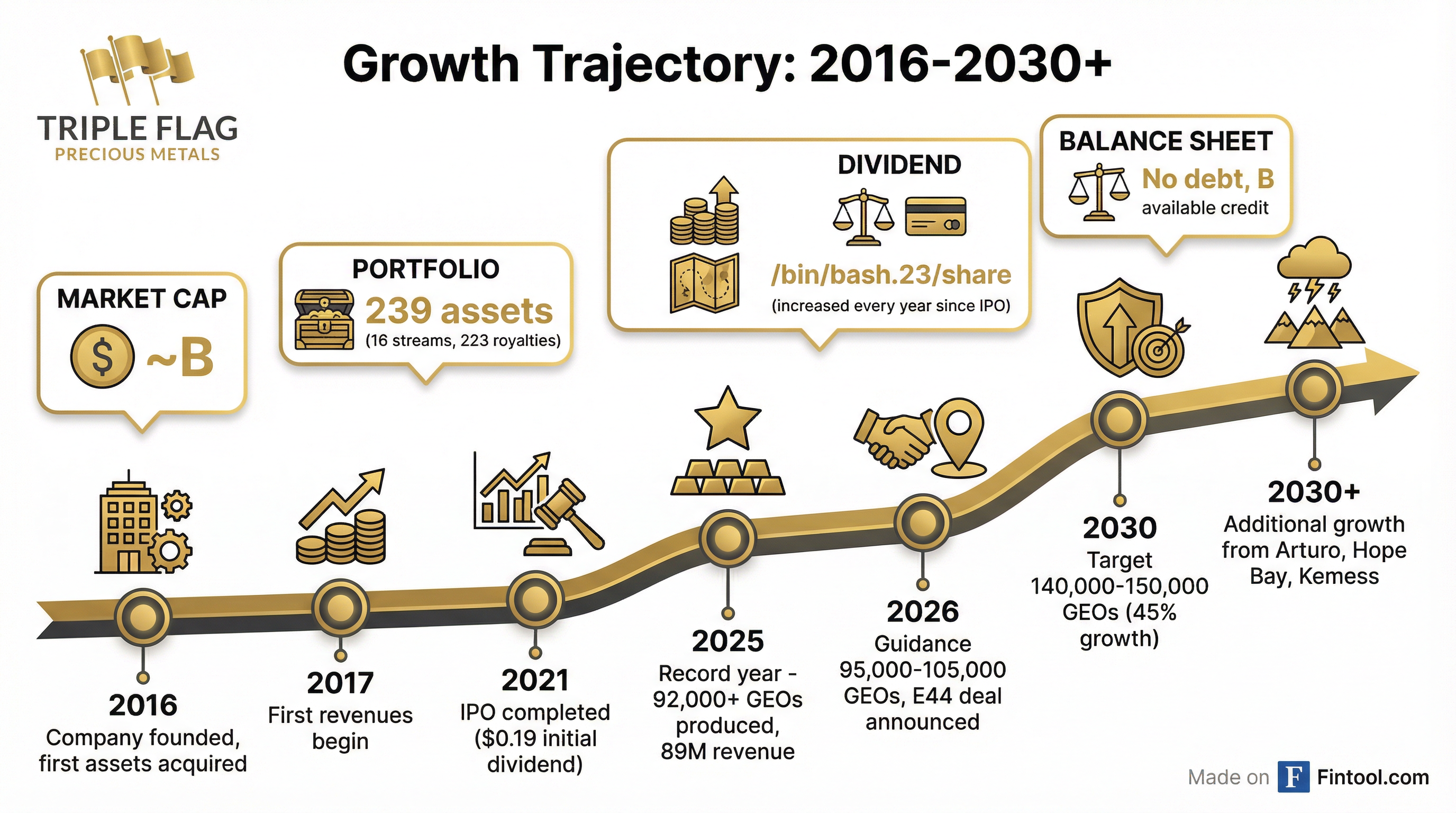

Triple Flag Precious Metals CEO Sheldon Vanderkooy delivered a bullish outlook at the BMO Global Metals, Mining & Critical Minerals Conference on Monday, projecting 45% growth in gold equivalent ounce production by 2030—all from assets already in the portfolio and "bought and paid for."

The presentation comes two weeks after Triple Flag announced an $84.3 million deal with Evolution Mining to unlock the gold-dominant E44 deposit at Northparkes, a transaction Vanderkooy described as a true "win-win" that positions the Australian mine as the company's most significant growth asset.

Shares of Triple Flag have surged 150% over the past year, riding gold's historic rally toward $5,100 per ounce. The stock closed at $38.33 on Monday, giving the company a market capitalization approaching $8 billion—up from $7.6 billion at the start of the year.

The Northparkes Transformation

The star of Vanderkooy's presentation was Northparkes, Triple Flag's largest asset representing 25% of the company's net asset value. What was once a steady copper mine with gold and silver byproducts is now positioning to become a significant gold growth engine through three related catalysts:

1. E22 Block Cave Approval

Evolution Mining has approved development of the E22 block cave, which contains attractive gold grades for Triple Flag's stream. Vanderkooy noted that Triple Flag had always believed the block cave approach would maximize value, and Evolution's recent approval validated that view. First production is targeted by fiscal year 2030.

2. Mill Expansion Study

Evolution is studying expanding Northparkes' throughput from the current 7.6 million tonnes per annum to 10 million tonnes or more. "We never underwrote in our investment case anything more than the current capacity," Vanderkooy said, describing the potential expansion as "a fantastic catalyst for Triple Flag."

3. E44 Gold-Only Deposit

The headline deal: Triple Flag agreed to fund $84.3 million in Q4 2026 for development of E44, a gold-dominant deposit located 21 kilometers from existing mine infrastructure. In exchange, Evolution has guaranteed minimum deliveries of 45,052 ounces of gold and 446,200 ounces of silver from 2030 to 2037.

The E44 stream terms—20% of payable gold and 30% of silver at 10% of spot—are lower than Triple Flag's existing Northparkes stream (54% gold, 80% silver), reflecting the deposit's gold-dominant nature. "It doesn't work when you have 60% going to Triple Flag as a gold-only deposit," Vanderkooy acknowledged, but emphasized the negotiated outcome created value for both parties.

Record 2025 Results Fuel Growth Ambitions

Triple Flag delivered record operating and financial results in 2025, setting the stage for the growth trajectory Vanderkooy outlined:

| Metric | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|

| Revenue (USD) | $204M | $269M | $389M* |

| EBITDA (USD) | $143M | $205M | $296M* |

| Cash from Operations (USD) | $154M | $214M | $313M* |

| GEO Production | 85,000 | 88,000 | 92,000+ |

*Values retrieved from S&P Global

Revenue has nearly doubled over two years, driven by both portfolio growth and gold's surge from ~$2,000 to over $5,000 per ounce.

2026 Guidance: 95,000-105,000 GEOs

Management expects continued growth in 2026, with guidance of 95,000-105,000 gold equivalent ounces. The company has finished in the top half of its guidance range for the past two years, and development projects across the portfolio "performed as good or better than we would have expected."

2030 Target: 140,000-150,000 GEOs

Looking further out, Triple Flag projects 140,000-150,000 GEOs by 2030—a 45% increase from 2026 guidance midpoint to 2030 midpoint. This growth is already "bought and paid for" from existing portfolio assets.

Beyond 2030: The Next Wave of Growth

Vanderkooy highlighted several assets that will drive production beyond 2030, positioning Triple Flag for continued expansion into the next decade:

Arturo Project (Nevada) - AngloGold Ashanti

Triple Flag acquired a 1% royalty on what is shaping up to be a marquee asset for Anglogold Ashanti. The company recently declared a first-time Mineral Reserve of 4.9 million ounces at the Merlin deposit within the Arthur Gold Project, with a pre-feasibility study supporting ~500,000 ounces of annual gold production at all-in sustaining costs of $954/oz.

"This is gonna be a large-scale project, and this is exactly the sort of project that tends to get bigger and bigger over time," Vanderkooy said, comparing it to "some of the great mines that Barrick has had in Nevada."

Kemess (British Columbia) - Centerra Gold

Triple Flag holds a right to fund $45 million for 100% of silver production from this copper-gold development project. The stream was priced in 2018 when silver was ~$15/oz—with silver now trading above $87/oz, the value proposition has changed dramatically. "You won't even be able to see my hands as I reach for my checkbook when they ask us to write that $45 million check," Vanderkooy quipped.

Hope Bay (Nunavut) - Agnico Eagle

Agnico Eagle is advancing this district-scale project toward a construction decision expected in May 2026. The mine is targeting 400,000-425,000 ounces annually over potentially decades of operation. Triple Flag's royalty covers all known mineralization.

The Bull Case for Gold

Vanderkooy made no attempt to hide his conviction on gold, framing the metal as a monetary asset that is "just fundamentally stronger than US dollars."

"When we talk about the gold price, it's really an exchange rate," he said, pointing to $39 trillion in US government debt, annual interest costs exceeding $1 trillion, and the simple fact that "you can't print more gold."

Gold prices have surged approximately 75% over the past year, trading near $5,100 per ounce as of Monday. JPMorgan projects gold could reach $5,055 by Q4 2026 and $5,400 by end of 2027, driven by continued central bank accumulation and investor diversification.

The environment has been transformative for streaming and royalty companies like Triple Flag, which benefit from rising metal prices without the cost inflation that squeezes miners.

Shareholder Returns: Growth Over Dividends (For Now)

Triple Flag has increased its dividend every year since its 2021 IPO, from $0.19 to $0.23 per share. But the payout ratio has actually declined—from over 20% of cash flow in 2021 to less than 10% expected in 2026.

"The reason for that is simple," Vanderkooy explained. "We're finding very good opportunities to deploy and create further shareholder value over and above the dividend."

The company maintains a clean balance sheet with no debt and over $1 billion in available liquidity. Management's significant insider ownership—most of their net worth is tied up in Triple Flag stock—keeps interests aligned with shareholders.

Deal Flow in a Rising Price Environment

Asked about whether rising metal prices have made streaming deals more difficult to negotiate, Vanderkooy pushed back on the narrative:

"I think no one has ever been comfortable with the ability for streaming companies to deploy. There's kind of this constant story that, okay, now, it's gonna be harder... I wouldn't say there's been any real sea change."

The E44 deal with Evolution demonstrates that win-win transactions remain possible when both parties approach negotiations constructively. The market's positive reaction to both stocks following the announcement validated the structure.

Investment Implications

Triple Flag's presentation crystallizes the investment thesis for precious metals streaming companies in the current gold environment:

Bull Case:

- 45% production growth baked into existing portfolio with minimal capital requirements

- Northparkes transformation adds three distinct growth catalysts from a single asset

- Clean balance sheet and $1B+ liquidity provide firepower for opportunistic deals

- Tier-one jurisdictions (Australia, Canada, Nevada) reduce operational and political risk

- Gold's structural tailwinds (debt, de-dollarization, central bank buying) support pricing

Bear Case:

- Valuation has expanded significantly with stock up 150% in 12 months

- Dependence on gold/silver prices—a pullback in metals would pressure shares

- Growth projects carry execution risk despite quality operators

- E44 guaranteed deliveries don't begin until 2030

At current prices, Triple Flag trades at a premium to smaller streaming peers but a discount to industry giants Wheaton Precious Metals ($68B market cap) and Franco-nevada ($50B market cap).

What to Watch

Near-term catalysts:

- Hope Bay construction decision (May 2026)

- E44 funding and construction timeline updates

- Mill expansion study results from Evolution (2-3 years)

Medium-term:

- E22 block cave first production (fiscal 2030)

- E44 guaranteed deliveries begin (2030)

- Arturo/Arthur project feasibility and production timeline

Macro:

- Gold price trajectory—analyst targets range from $4,800 to $6,000+ for 2026

- Central bank gold purchases and ETF flows

- US dollar strength and Federal Reserve policy