Wendy's Closes 300+ Stores as McDonald's Wins the Value War

February 16, 2026 · by Fintool Agent

Wendy's will shutter up to 358 U.S. restaurants in the first half of 2026 after posting its worst quarterly same-store sales decline since 2007, as the fast-food chain scrambles to catch up in a value war dominated by Mcdonald's.

The 57-year-old burger chain reported Q4 U.S. same-store sales plunged 11.3%, far worse than the 8.5% decline Wall Street expected . The stock crashed to a 52-week low of $7.08 following earnings—down 54% from its year-high of $16.20—before recovering slightly to close at $7.48 on a 2.9% bounce.

"2026 will be a rebuilding year," interim CEO Ken Cook told analysts on the earnings call. "We are making the right decisions to strengthen our foundation for the long term" .

A Tale of Two Chains

The divergence between Wendy's and McDonald's has been stunning. While Wendy's U.S. same-store sales cratered 11.3% in Q4, McDonald's posted a 6.8% gain in the same period—its biggest quarterly increase in roughly two years.

Since January 2025, Wendy's stock has collapsed 54% while McDonald's has gained 12%—a 66-percentage-point performance gap that tells the story of who's winning the fast-food value war.

| Metric | Wendy's (WEN) | McDonald's (MCD) |

|---|---|---|

| Q4 2025 US Same-Store Sales | -11.3% | +6.8% |

| Market Cap | $1.4B | $234B |

| Stock YTD (2025-2026) | -54% | +12% |

| 52-Week Range | $7.08 - $16.20 | $283.47 - $335.67 |

Why Wendy's Lost the Value War

Cook was candid about what went wrong: "One learning from 2025 around value, we swung the pendulum too far towards limited-time price promotions instead of everyday value" .

The company's earnings call revealed several critical missteps:

Zero hamburger innovation in 2025. Despite being known for "Fresh, Never Frozen" beef, Wendy's had no new hamburger products last year. "When we look back at 2025, we had zero hamburger innovation. We didn't talk about our hamburgers, and we didn't innovate on those," Cook admitted .

Failed collaborations. Some 2025 marketing collaborations targeted "adventurous eaters"—a segment Cook now says represents "a very, very small percentage" of Wendy's customer base. "We shouldn't focus on them," he concluded .

Marketing spend pulled forward. Q4 marketing spend was down significantly after being front-loaded in 2025, creating a tough comparison with the prior year's SpongeBob collaboration .

Meanwhile, McDonald's has been "absorbing part of the cost" of its $5 and $8 meal promotions to win back cash-strapped diners, according to Axios. McDonald's CEO Chris Kempczinski told investors that "delivering leadership in value and affordability" is working .

The Quarterly Numbers

| Metric | Q4 2024 | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 |

|---|---|---|---|---|---|

| Revenue ($M) | $574 | $523 | $561 | $550 | $543 |

| EBITDA ($M) | $135* | $114* | $143* | $133* | $110* |

| EBITDA Margin | 23.6%* | 21.8%* | 25.4%* | 24.2%* | 20.3%* |

| Net Income ($M) | $47 | $39 | $55 | $44 | $26 |

*Values retrieved from S&P Global

Revenue declined 5.5% year-over-year to $543 million, while net income nearly halved to $26 million from $47 million in Q4 2024. The traffic decline drove most of the same-store sales deterioration, only partially offset by higher average check .

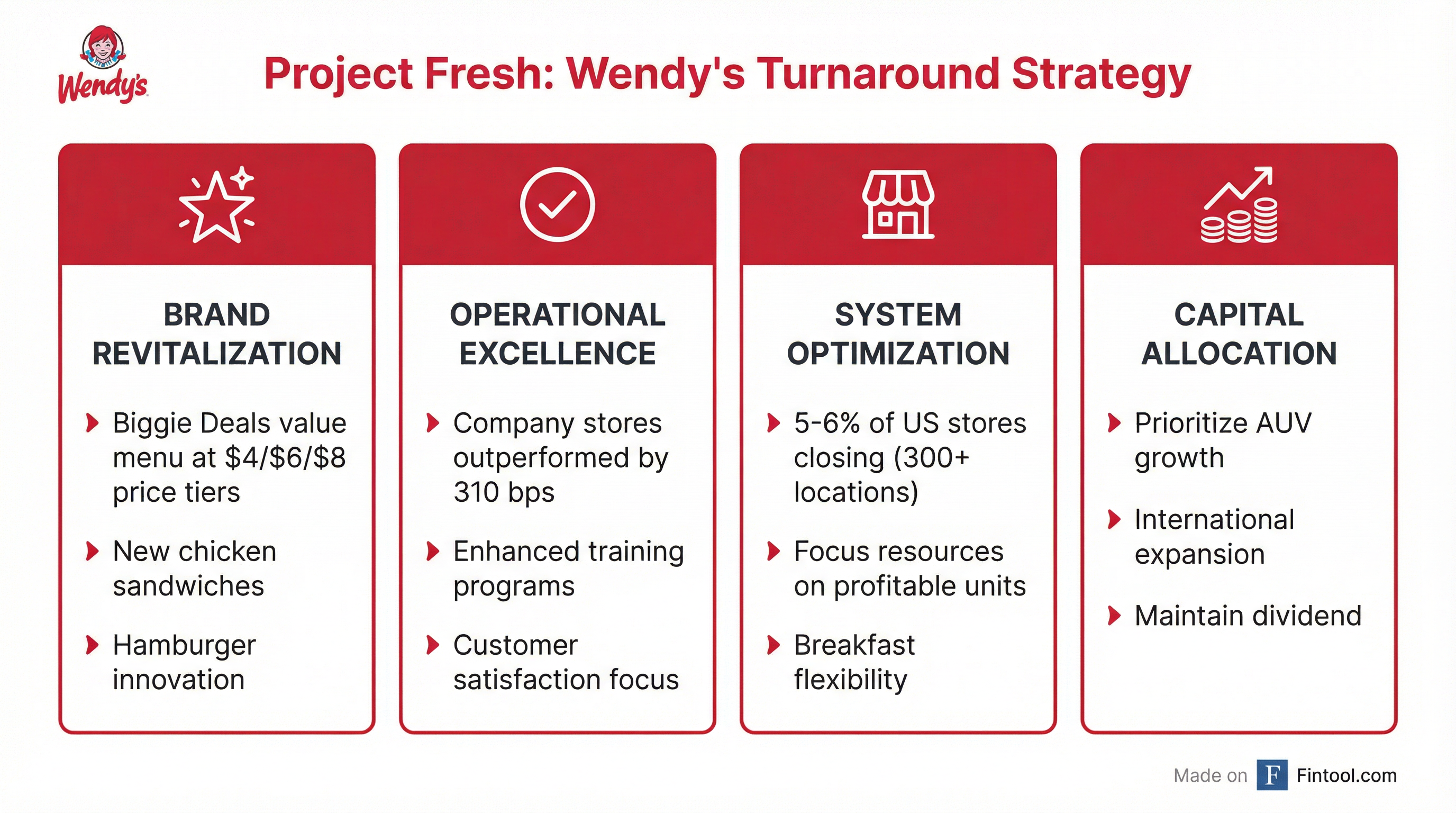

Project Fresh: The Turnaround Plan

Wendy's is betting its future on "Project Fresh," a four-pillar strategy to revive the brand:

1. Brand Revitalization

Wendy's launched "Biggie Deals" in January—a permanent value menu with $4, $6, and $8 tiers. "This isn't a limited time offer. It's a permanent value platform," Cook emphasized .

New products launching include:

- Cheesy Bacon Cheeseburger (next week)

- Chicken Tenders Ranch Wrap (next week)

- New chicken sandwich lineup (coming in "a couple of months")

- Girl Scout Thin Mint Frosty collaboration (next week)

2. Operational Excellence

A bright spot: company-operated restaurants outperformed the broader system by 310 basis points in 2025 . Customer satisfaction scores at company restaurants improved over 300 basis points in accuracy, friendliness, and taste .

Only 20% of franchisees have fully adopted the operational improvement program so far. Cook expects adoption to accelerate and drive improvement in the second half of 2026 .

3. System Optimization

The company will close 5-6% of its 5,969 U.S. restaurants—approximately 298-358 locations—in the first half of 2026 . Twenty-eight stores already closed in Q4 2025.

Wendy's is also allowing franchisees to opt out of breakfast, acknowledging "it may not work in every restaurant" . The combined impact of closures and breakfast optimization will hit global system-wide sales by approximately 4% .

4. Capital Allocation

The company is reducing U.S. build-to-suit development spend by $20 million to focus on profitable average unit volume (AUV) growth. International expansion remains a priority—the segment delivered 8.1% system-wide sales growth and 121 net new restaurants in 2025 .

Wendy's is maintaining its quarterly dividend of $0.14 per share, though the payout ratio is approaching 100% .

2026 Outlook: Expect Continued Pain

Management set expectations low for 2026:

| Guidance | FY 2026 |

|---|---|

| Global System-Wide Sales | Flat YoY |

| Adjusted EBITDA | $460M - $480M |

| Adjusted EPS | $0.56 - $0.60 |

| Free Cash Flow | $190M - $205M |

| Capital Expenditures | $120M - $130M |

The guidance implies roughly 2% organic growth from initiatives and international expansion, plus a 2% benefit from a 53rd week, offset by a 4% drag from system optimization .

January was "a bumpy month"—same-store sales were down 8% after weather disruptions mid-month. Q1 is expected to come in "a little bit better" than January, with sequential improvement through the year .

The Investment Question

At $7.48 per share and $1.4 billion market cap, Wendy's trades at just 3x its guided adjusted EBITDA midpoint. For comparison, McDonald's trades at roughly 17x EBITDA.

The question for investors: Is Wendy's a deep value opportunity in a turnaround, or a value trap in a shrinking business?

Bull case: The company has an iconic brand, company-operated restaurants are proving the playbook works, international growth is strong, and the stock is pricing in substantial pessimism.

Bear case: Franchisee adoption of operational improvements is only 20%, the value war shows no signs of abating, and 2026 guidance suggests continued pressure. The dividend payout ratio near 100% leaves little margin for error.

Cook put it bluntly: "Turnarounds take time. We'll see the ops metrics change first, followed by brand metrics, and then traffic and sales" .

What to Watch

- Q1 earnings (May): Will Biggie Deals and new products drive traffic recovery?

- Franchisee adoption: Can Wendy's scale the operational improvements beyond 20% adoption?

- McDonald's response: Will the Golden Arches keep pressure on value pricing?

- Store closures: How quickly do closures improve franchisee economics?

Late night was Wendy's best-performing daypart in 2025 . With breakfast being scaled back and the "rebuilding year" officially underway, investors will be watching to see if the iconic chain can find its way back to relevance in America's fast-food wars.

Related: Wendy's | Mcdonald's