Western Midstream CFO Outlines Capital Discipline Strategy in Q4 2025 Fireside Chat

February 24, 2026 · by Fintool Agent

Western Midstream Partners CFO Kristen Shults laid out a measured playbook for navigating producer pullbacks in a fireside chat released Monday, cutting 2026 capital expenditure guidance by approximately $175 million while defending the partnership's 5% EBITDA growth target and strategic project timelines.

The message to unitholders: WES can throttle discretionary spending quickly when activity softens—without derailing the Aris integration or crown-jewel projects like the Pathfinder pipeline.

Record 2025 Sets the Stage

The numbers backing Shults' confidence are compelling. Full-year 2025 Adjusted EBITDA reached a record $2.48 billion, exceeding the midpoint of guidance and marking a 6% year-over-year increase. Free cash flow of $1.53 billion—a 15% jump—came in above the high end of the $1.275-$1.475 billion guidance range.

Q4 2025 Adjusted EBITDA landed at $636 million, though Shults noted this included roughly $30 million in negative non-cash revenue recognition adjustments. "Without that adjustment, we would have been right around $665 million for Q4," she explained.

The partnership's cost discipline has been relentless. Excluding Aris, Q4 2025 operations and maintenance expense declined 12% year-over-year—the third consecutive quarterly improvement. "We've eliminated more than $100 million in annualized operation and maintenance expenses from Q1 to Q4 2025," management noted on the formal earnings call.

The 2026 Balancing Act

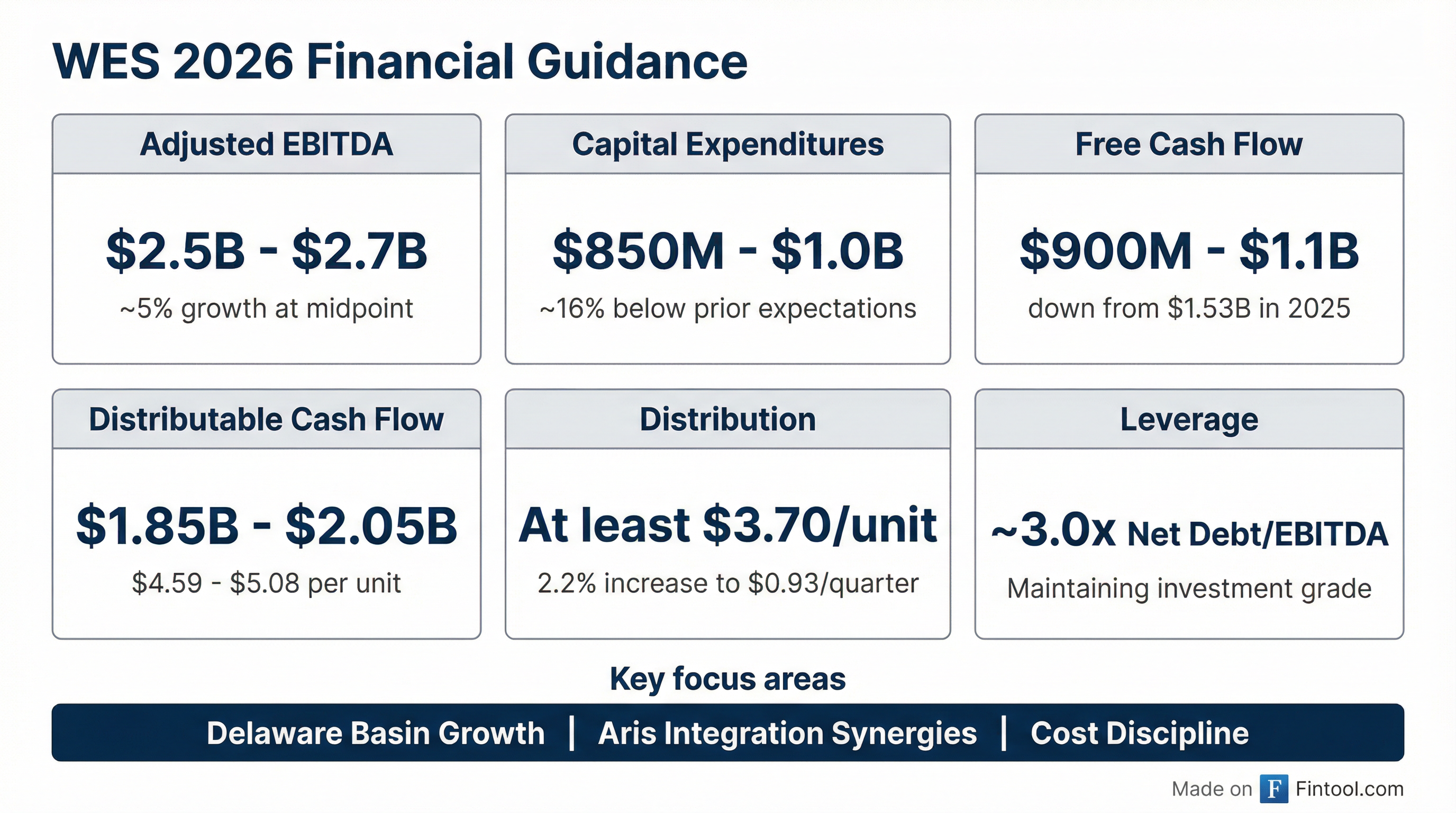

WES's 2026 guidance reflects the tension between growth ambitions and producer retrenchment. Adjusted EBITDA is projected at $2.5-$2.7 billion—roughly 5% growth at the midpoint—while capital expenditures have been slashed to $850 million-$1 billion.

The capex reduction—from "at least $1.1 billion" just last quarter—demonstrates what Shults called the partnership's ability to "push and pull on the capital side of things in order to help manage Free Cash Flow when we are getting a little bit more of a volatile environment."

| Metric | 2025 Actual | 2026 Guidance (Midpoint) | Change |

|---|---|---|---|

| Adjusted EBITDA | $2.48B | $2.6B | +5% |

| Capital Expenditures | $722M | $925M | +28% |

| Free Cash Flow | $1.53B | $1.0B | -35% |

| Distribution/Unit | $3.64 | $3.70+ | +2% |

The free cash flow step-down—to $900 million-$1.1 billion from $1.53 billion—reflects the heavy lift on Pathfinder and North Loving II construction, not operational deterioration. Approximately half of 2026 capex is directed toward these two projects, both still on track for 2027 start-ups.

Producer Headwinds by Basin

Shults was candid about the activity slowdown affecting WES's forecasts. "We use our producers' forecast to come up with our throughput expectations for the year, and what we saw really in the last few months of the year and into the beginning of this year has been a pullback in some of those forecasts."

The pain is concentrated outside the Delaware Basin:

- DJ Basin: Mid- to high-single-digit volume declines expected for natural gas and crude plus NGLs in 2026

- Powder River Basin: Natural gas throughput projected to fall 10-15% given commodity sensitivity

- Delaware Basin: Low-to-mid single-digit growth in crude, NGLs, and natural gas; 80%+ growth in produced water (driven by Aris)

"We're expecting declines in activity in the Powder River and the DJ. We talked about that last year some, but I think that's a little bit more pronounced than originally thought," Shults acknowledged.

The Waha pricing situation added complexity. Negative natural gas prices at the West Texas hub prompted some private producers to curtail volumes in Q4. CEO Oscar Brown noted on the earnings call that WES is working with exposed customers on commercial solutions—potentially aggregating commitments to downstream transport that individual producers couldn't make alone.

Aris Integration: Ahead of Schedule

The $1.5 billion Aris Water Solutions acquisition—which closed in Q4 2025—is exceeding expectations.

Integration milestones completed include:

- Full ERP and purchasing system consolidation

- Operations and project management system integration

- Vendor contract harmonization

- Complete IT and HR system migration

The $40 million in targeted cost synergies has been achieved, with 85% to be realized by end of Q1 2026 and the remainder by year-end as legacy contracts expire.

"The acquisition has strengthened our commercial organization, expanded our capabilities, and increased direct engagement from our producing customers now that the platform has been fully brought under the WES umbrella," Brown stated.

WES now operates one of the largest integrated water footprints in the Delaware Basin, with capabilities spanning:

- Fresh water supply

- Recycling (1.4 million barrels/day capacity)

- Gathering

- Long-haul transportation (Pathfinder)

- Disposal

- Beneficial Reuse treatment technology

The 2026 O&M outlook reflects this transformation. Despite including a full year of Aris, total O&M is expected to increase only 10-15%—"significantly below what the two standalone companies would have been on a pro forma basis."

Pathfinder: Costs Down, Interest Up

The Pathfinder Produced Water Pipeline—a 42-mile, 30-inch diameter system with 800,000+ barrels/day capacity—remains on track for Q1 2027 startup.

Brown revealed encouraging developments on the commercial front: "We're seeing a significant pickup in interest in both more integrated solutions... and straight-up commitments to the pipe, whether it's our customers or even some of our peers."

Construction costs are also improving. A late-2025 commercial transaction provided better access to land and disposal well opportunities, allowing WES to optimize the pipeline path. "The cost of Pathfinder is coming down meaningfully," Brown said. "Even with the MBCs [minimum barrel commitments] we already have in place, we see the returns on that project going up."

Distribution Strategy: Coverage Over Growth

WES is recommending a $0.02/unit distribution increase to $0.93/unit starting Q1 2026—a modest 2.2% bump that prioritizes coverage growth over distribution growth.

"We have talked a lot about coverage and wanting to increase coverage naturally over time," Shults explained. "As we're growing Adjusted EBITDA by 5%, and we're trailing that distribution, right around 2%, it'll help with that natural growth of Distribution Coverage."

The full-year 2026 distribution guidance of "at least $3.70 per unit" implies the partnership has room to accelerate if conditions warrant.

Notably, Shults emphasized that free cash flow remains central to capital allocation decisions despite the introduction of DCF guidance. "Free Cash Flow is still a very important metric for us. It is very much in our discussions and our strategy decision-making here... We look at it when we're thinking about capital allocation decisions, just like leverage."

No Strategy Change

Despite the activity headwinds, management insisted the fundamental playbook remains intact.

"No, we're not expecting to change our strategy," Shults stated. "If you look at what we did in 2025 from a growth perspective, both organic and inorganic, we expect to use the same playbook in 2026 and beyond in order to continue to grow the business."

The low leverage position—approximately 3.0x net debt/EBITDA even after financing the Aris acquisition—provides flexibility to pursue additional M&A. "We've kept leverage low for a reason. It allows us to go out and go after these growth opportunities, and it allows us to make sure that our distribution is safe and in check as well."

Market Reaction

WES shares closed at $41.20 on Monday, up 0.24%, and traded at $41.75 in after-hours—essentially flat with the analyst consensus price target. The stock is up 5% from its February lows but remains 8% below its 52-week high of $44.74.

The muted reaction suggests investors had largely priced in the guidance framework following last week's formal earnings release. The fireside chat provided color rather than surprises.

What to Watch

Q1 2026 earnings (late April): First full quarter of Aris contribution and winter storm impact quantification. Management flagged $10-20 million of storm-related headwinds.

Pathfinder commercial progress: Additional customer commitments and potential peer participation could signal the project's strategic value beyond WES's own footprint.

Waha egress relief: New pipeline capacity coming online in H2 2026 should alleviate some curtailment pressure on WES's gas-exposed producers.

Beneficial Reuse developments: WES retained Aris's beneficial reuse treatment technology business—potentially a meaningful long-term value driver as produced water management regulations evolve.

Related Companies: Western Midstream Partners · Occidental Petroleum