ACV Auctions (ACVA)·Q4 2025 Earnings Summary

ACV Auctions Beats Q4 Guidance But Slowing Growth Sends Stock Down 15%

February 23, 2026 · by Fintool AI Agent

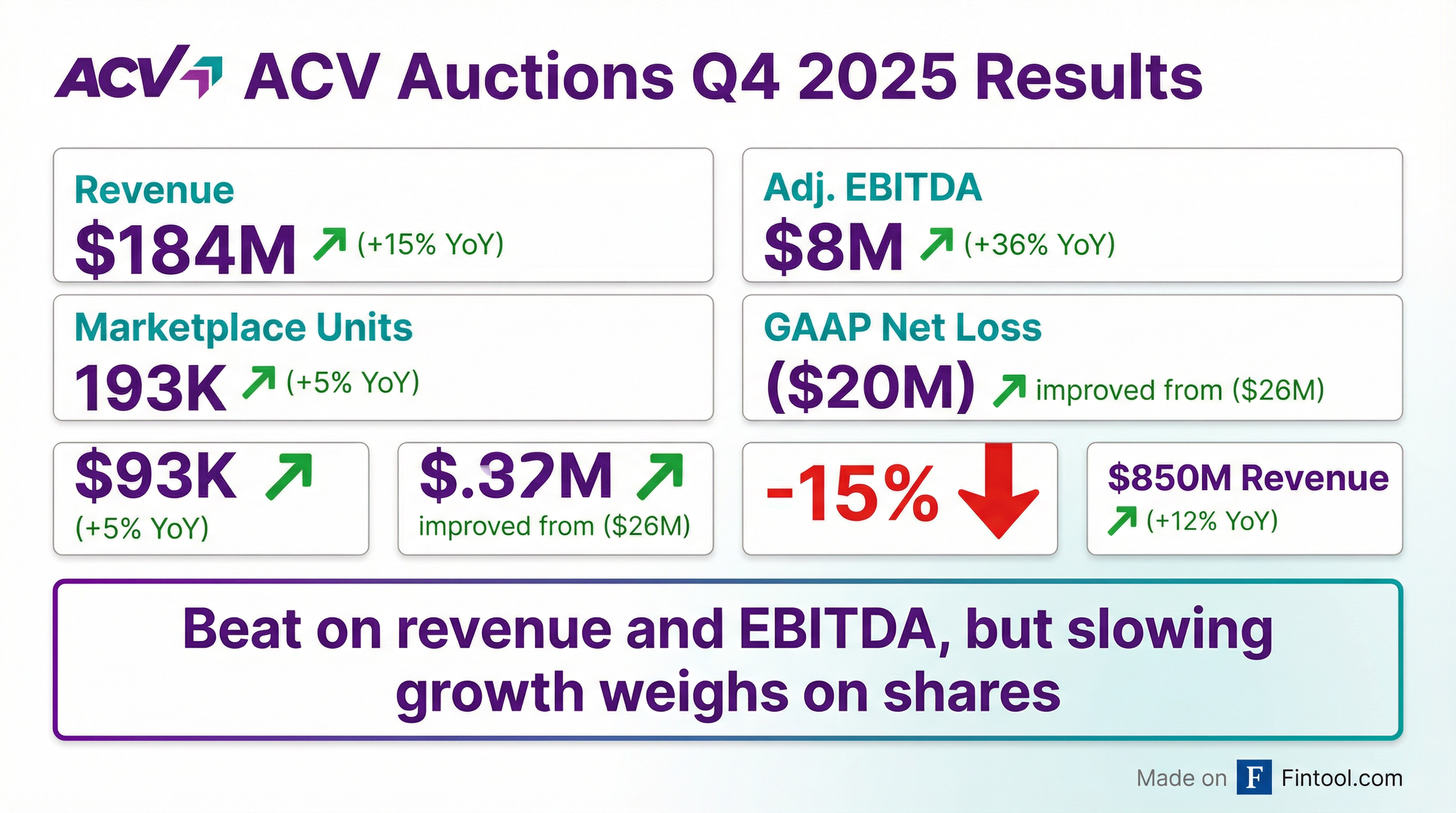

ACV Auctions (NYSE: ACVA) delivered Q4 2025 results that exceeded guidance across the board, but the digital auto marketplace's stock plunged 15% as investors digested a decelerating growth outlook for 2026. Revenue of $184M (+15% YoY) hit the high-end of guidance while Adjusted EBITDA of $8M beat the top of the range.

Did ACV Auctions Beat Earnings?

Yes — ACV beat on both revenue and profitability metrics:

CEO George Chamoun noted: "We are very pleased with our fourth quarter results, with revenue at the high-end of guidance and Adjusted EBITDA above the high-end of guidance, along with continued margin expansion."

The full-year 2025 results showed strong execution:

What Did Management Guide?

FY2026 guidance implies growth deceleration — the key driver of today's selloff:

Key assumptions in guidance:

- Conversion rates and wholesale price depreciation expected to follow normal seasonal patterns

- Non-GAAP OpEx (ex. COR) expected to increase approximately 9% YoY

- Revenue growth expected to outpace OpEx growth by ~300 basis points

The FY2026 revenue growth midpoint of 12% compares unfavorably to FY2025's 19% growth, signaling that while ACV continues gaining market share, the overall wholesale auto market remains challenged.

How Did the Stock React?

ACVA shares fell 15% on the earnings release:

The selloff reflects investor disappointment with the decelerating growth trajectory. While ACV continues to gain market share and improve profitability, the FY2026 outlook suggests the wholesale auto market headwinds are persisting longer than hoped.

What Changed From Last Quarter?

Positive developments:

- Margin expansion continues: Adjusted EBITDA margin improved to 4% in Q4 (vs guidance of 3-4%) and 8% for FY2025, on track toward mid-term targets

- Operating leverage: Non-GAAP Cost of Revenue as % of revenue fell from 47% to 49% YoY while Non-GAAP OpEx (ex. COR) as % of revenue declined from 53% to 49%

- Strong cash position: $270M cash (includes ~$171M marketplace float), with solid operating cash flow

- ACV Transport growth: 20% revenue growth with ~110,000 transports delivered, AI-optimized pricing driving strong growth and revenue margin already at mid-term target in the low 20s

- ACV Capital expansion: 48% YoY revenue growth despite actively lowering exposure to higher-risk customer segments

- Franchise rooftop penetration milestone: Reached 35% during the year, with major account team delivering 300 bps increase

- ClearCar traction: Existing dealers that launched ClearCar increased wholesale volumes at ACV by over 50% after going live

- ACV MAX bundling success: New ACV MAX dealers increased wholesale vehicle sales by 40% within 1 quarter of launching MAX

- Sell-through improvement: Up 150 bps YoY in Q4, with over 10 bidders per car on average

- Network growth: 15,000 unique sellers and over 22,000 unique buyers transacting with ACV in 2025

Concerns:

- Sequential revenue decline: Q4 revenue of $184M was down from Q3's $200M, reflecting normal seasonality but also market softness

- Growth deceleration: FY2026 guidance of 11-13% growth vs 19% in FY2025 and 32% in FY2024

- Marketplace GMV slowing: Only +2% YoY vs +5% unit growth, indicating lower average selling prices

- January weakness: Dealer wholesale market down 6.5% YoY in January per AAA data

Revenue Breakdown

ACV's diversified revenue streams showed mixed performance:

The auction and assurance revenue growth faced a tough comparison against Q4 2024's 40% growth. ARPU of $528 grew 6% YoY and 4% sequentially, driven by ACV Guarantee adoption.

ACV Transport achieved revenue margin in the low 20s — already at mid-term targets — with AI-optimized pricing driving both growth and operating efficiency. Off-platform transportation service gaining traction.

ACV Capital grew 48% despite actively reducing exposure to higher-risk customer segments following the Tricolor bankruptcy. New growth strategies implemented while driving process enhancements to mitigate portfolio risk.

Key KPIs and Operating Metrics

Regional performance highlights strong execution:

- Carolinas: Strong YoY unit growth

- South Florida: Strong YoY unit growth

- Texas East: Strong YoY unit growth

- Southern California: Strong YoY unit growth

ARPU Outlook: Management expects Q4's $528 auction and assurance ARPU to be "flat to maybe up very modestly" in 2026, reflecting a conservative stance on pricing power.

Balance Sheet & Capital Position

ACV maintains a strong balance sheet to fund growth:

The increase in long-term debt to $190M reflects continued investment in the ACV Capital floor plan financing business.

Management Credibility Check

ACV has consistently delivered results in line with or above guidance:

The team has demonstrated operational discipline, but the repeated downward revisions to growth outlooks over the past year have eroded investor confidence in the long-term growth story.

Q&A Highlights

On AI Competitive Moat:

When asked about AI disruption risk, CEO George Chamoun pushed back firmly: "The irony is we are that disruptor. We are the AI disruptor in this category... We're the company who's trying to help a traditional retailer, like a franchise dealer, as cars drive through a service drive, take pictures and videos and predict the retail price within $38... We're in a really unique spot."

On competition from potential startups: "They'd have to raise hundreds of millions of dollars, if not billions, to then have the balance sheet and the data, which would be very difficult to do, where we've inspected over 1 million cars a year."

On VIPER Product Rollout:

VIPER (ACV's next-gen inspection technology) is entering commercial launch: "We're starting to implement somewhere around 5 to 10 a month right now... Our goal is to put somewhere north of 100 of these out in the field, maybe as close as 200. We've got at least 200 hand raisers."

The three key objectives for VIPER: 1) Help dealers buy more cars, 2) Faster retail photos on websites, 3) Increase service revenue through upsells like tire depth predictions with 90%+ confidence.

On Market Conditions:

"In January, according to AAA, dealer wholesale was down by 6.5%... Too early to say it'll be down for the whole year... We are still thinking that it'll be a flattish year."

70% of wholesale business still happens at physical auctions, representing significant runway for digital conversion.

On Conversion Rates:

"Our conversion rate for Q4 was up year-over-year, where most of our competitors were flat or down... We've got 9.8 bidders per car. I think we're now at over 10 bidders per car."

ACV Guarantee (no reserve auction) mix increased to 19% in Q4 and is already in the 20% range in Q1 2026.

On FY2026 Investment Strategy:

CFO Bill Zerella clarified the incremental spending: "The incremental spend that we baked into our guidance for this year in terms of those go-to-market investments is approximately $11 million. If you look at our incrementals, excluding that, they would have actually grown 500 bps year-over-year from 25% to 30%."

Additional VIPER investment of "high single-digit millions" will flow through as CapEx.

On Service Drive Opportunity:

"We've got rooftops buying anywhere between 4 and as high as 10% of all ROs (repair orders)... This could be anywhere between 40 and 100 cars a month. [One dealer is] already buying over 150 a month."

Key Risks and Concerns

-

Wholesale market headwinds: January dealer wholesale was down 6.5% according to AAA, though management still expects a flat year

-

Tricolor bankruptcy impact: ACV recognized $18.7M in losses related to an ACV Capital customer bankruptcy in FY2025

-

Tariff exposure: Management flagged potential impacts from "new, reinstated or adjusted tariffs" in forward-looking risk factors

-

Arbitration costs: Elevated in Q4 within a specific customer cohort, though "steps are already showing positive returns in early 2026" following removal of bad actors

-

Competition: Physical auction giants Manheim and ADESA continue investing in digital capabilities; market may evolve to duopoly rather than winner-take-all

-

GAAP losses persist: Despite improving profitability, ACV guided to ($50M)-($54M) GAAP net loss in FY2026

What to Watch Next

- Q1 2026 results (expected May 2026): Will revenue hit the $200-204M guidance range? Early Q1 shows ACV Guarantee mix already at 20%+

- VIPER commercial rollout: Goal is 100-200 units deployed in 2026, scaling to mass rollout in early 2027

- Inspector hiring progress: 20-30 currently in training; goal to complete national footprint by end of Q3

- Commercial wholesale greenfield: Houston operational, Chicago launching 2026

- Wholesale market recovery: January down 6.5%, watching for seasonal normalization and used car pricing trends

- ACV Capital credit quality: Monitoring for additional credit losses after Tricolor bankruptcy

Sources: ACV Auctions Q4 2025 Earnings Presentation, Form 8-K, Press Release (February 23, 2026)

View ACVA Company Profile | View Earnings Transcript | Prior Quarter: Q3 2025