AMBC (AMBC)·Q4 2025 Earnings Summary

Octave Specialty Group Beats EPS, Combined Ratio Drops Below 100%

February 24, 2026 · by Fintool AI Agent

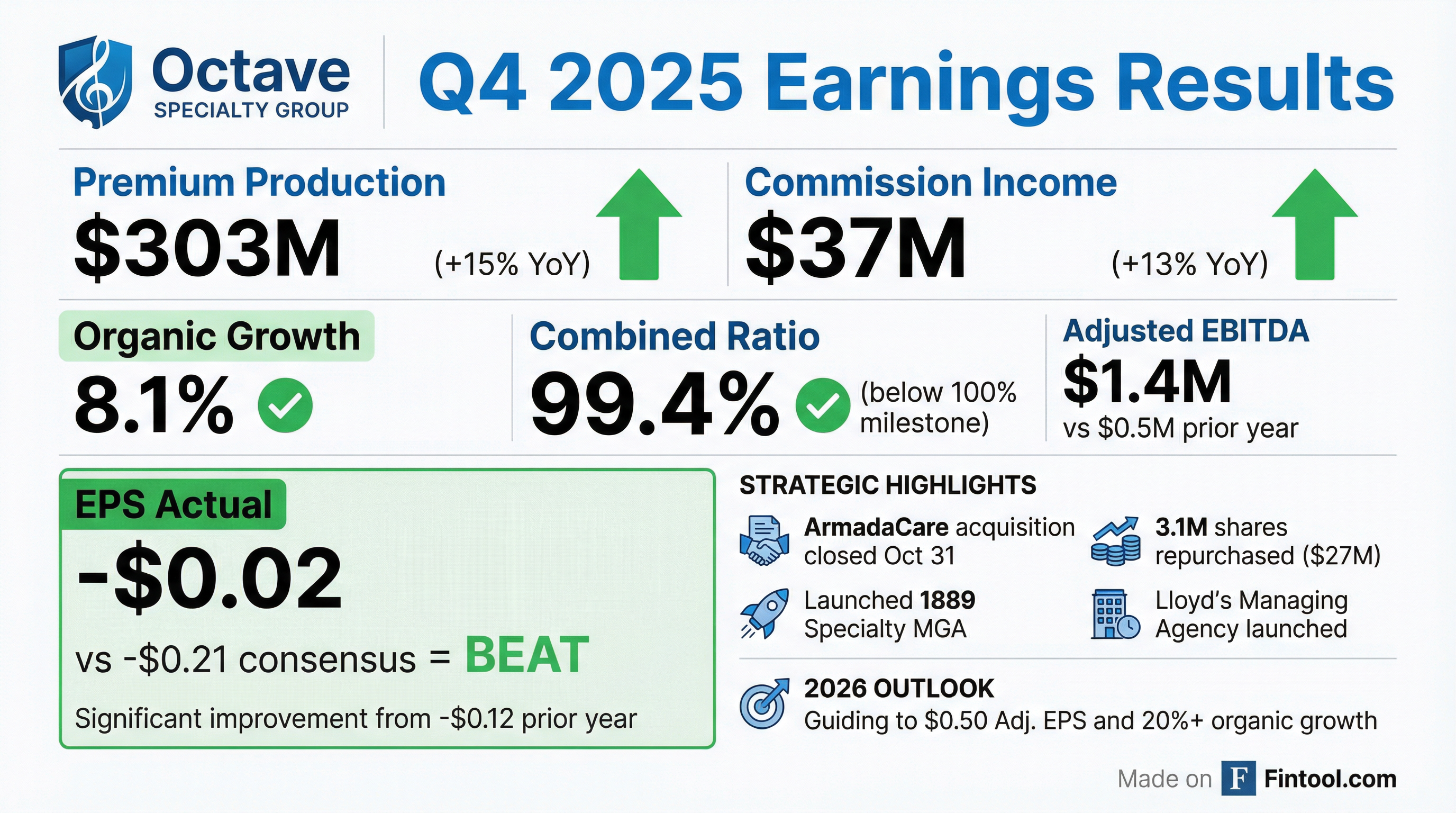

Octave Specialty Group (NYSE: AMBC) delivered a significant EPS beat in Q4 2025, with adjusted EPS of -$0.02 handily exceeding the -$0.21 consensus estimate. The specialty insurance platform achieved a key milestone as its Everspan combined ratio dropped below 100% for the first time, signaling improving underwriting discipline. Management provided bullish 2026 guidance of $0.50 adjusted EPS with 20%+ organic growth in Insurance Distribution.

Did Octave Beat Earnings?

EPS: Beat by 90% — Adjusted EPS came in at -$0.02 versus consensus of -$0.21, a $0.19 improvement. This compares to -$0.12 in Q4 2024, showing continued progress toward profitability.*

Revenue: Missed by 20% — Total revenue of $66.9M missed the $83.9M consensus estimate, reflecting the company's ongoing transformation from legacy Ambac operations to the Octave specialty insurance platform.*

The turnaround story is evident: net loss from continuing operations improved dramatically to $(30)M from $(548)M in Q4 2024, though the prior year included significant discontinued operations impacts.

What Drove the Combined Ratio Below 100%?

The Everspan specialty P&C insurance segment achieved a combined ratio of 99.4% in Q4 2025, crossing below 100% for the first time—a key milestone for the capital-light fronting platform.

GPW increased 34% year-over-year to $80M, reflecting strong momentum across casualty-focused programs. The segment now operates 25 live programs with an A- AM Best rating.

For full year 2025, the Specialty P&C segment reported a combined ratio of 105.2% (loss ratio 70.2%, expense ratio 35.1%), though this included legacy reserve development from discontinued operations.

How Did the Stock React?

AMBC shares traded at $8.29, down 4.2% on the day of earnings release. The stock remains well off its 52-week high of $13.64 but has recovered significantly from its 52-week low of $5.99.

The muted reaction despite the EPS beat likely reflects investor focus on the revenue miss and continued net losses at the consolidated level.

What Did Management Guide for 2026?

Management provided detailed 2026 guidance signaling confidence in accelerating profitability:

The $0.50/share guidance represents a significant inflection from the -$0.60/share adjusted loss in FY 2025, driven by:

- Insurance Distribution scaling with 20%+ organic growth

- Everspan achieving sustainable profitability

- Corporate cost reductions of ~$10M annualized

What Changed This Quarter?

Strategic acquisitions expanding the platform:

- ArmadaCare acquisition closed October 31 — Expands Accident & Health offerings, adding fee-based revenue

- 1889 Specialty launched — New professional lines MGA leveraging Lloyd's A+ rated syndicate capacity

- Lloyd's Managing Agency launched — Octave Ventures establishing third-party management for broader fee revenue

Capital allocation:

- 3.1M shares repurchased in October for $27M (~6.7% of shares outstanding)

- Aggressive buyback signals management confidence in undervaluation

Cost reductions underway:

- Executive management reduced from 7 to 4

- Corporate headquarters relocation saving ~$4M annually

- Total annual cost reduction of

$17M gross ($10.5M adjusted)

Insurance Distribution: The Growth Engine

The Insurance Distribution segment remains Octave's primary growth driver:

For full year 2025, Insurance Distribution achieved:

- Premium production up 93% to $952M

- Total revenue up 65%

- Organic growth of 14.2%

- Adjusted EBITDA of $22.5M vs $13.4M prior year

Start-up MGA losses totaled $2.7M in Q4 ($1.5M attributable to shareholders), which will diminish as newer MGAs reach profitability within the typical 18-24 month timeline.

The Dual-Engine Business Model

Octave operates two complementary growth strategies:

Octave Ventures (De Novos):

- Target 2-4 new MGAs per year

- $1M cumulative investment per MGA

- EBITDA positive in 18 months

- Investment recovered by month 24

- Target margins of 5%+ with improving ratios

Octave Partners (Acquisitions):

- Strategic, opportunistic acquisitions

- Focus on proven underwriting teams

- Clear integration roadmaps

- Recent examples: Beat (2024), ArmadaCare (2025)

The company launched 3 new MGAs in 2025 and 6 in 2024, building a diversified platform across specialty lines including Accident & Health, Commercial Auto, Professional Lines, Property, and Energy.

Q&A Highlights

De novo MGA pipeline: CEO Claude LeBlanc indicated they're targeting 2-3 new MGA launches in 2026, fewer than the 6 in 2024 and 3 in 2025, to allow existing platforms to scale. Focus remains on U.S. E&S and SME segments.

Cash flow and NCI buy-ins: CFO David Trick confirmed NCI buy-ins will be less than $50M in 2026, funded by cash and "some marginal additional borrowing." Distributions to the holding company continue improving.

Earnings seasonality: Q1 and Q4 remain the heaviest quarters. A&H businesses including ArmadaCare are weighted ~60% to Q1. As startup MGAs reach profitability through 2026, earnings will shift slightly toward the back half.

Pricing environment by segment:

Investment income & equity comp: Net investment income expected flat to marginally higher in 2026. Equity-based compensation will be down a few million dollars versus 2025.

Hammurabi AI Platform: A Competitive Differentiator

Management highlighted Hammurabi, their proprietary AI platform built for the medical stop-loss business. The platform is already driving record results in the ESL business after challenging prior years.

"Hammurabi replaces traditional labor-intensive processes with near-instant risk prediction and pricing accuracy, enabling our underwriters to move faster, price more precisely, and scale more efficiently than ever before." — Claude LeBlanc, CEO

Key capabilities:

- Near-instant risk prediction and pricing

- Scalable across underwriting operations

- Potential to expand to other business lines over time

- Already contributing to record ESL results in Q1 2026

The company is also actively developing additional AI tools across the platform, which management believes will help "rapidly scale and differentiate our business model into the future."

Risks and Concerns

Revenue trajectory concerns: The 20% revenue miss versus consensus warrants monitoring, though this may reflect timing differences in premium recognition versus the legacy Ambac accounting.

Combined ratio sustainability: While Q4's 99.4% combined ratio is encouraging, full year 2025 remained at 105.2%. Management must demonstrate consistent sub-100% performance across multiple quarters.

Execution risk on guidance: The leap from -$0.60/share to +$0.50/share adjusted EPS requires flawless execution across cost cuts, organic growth, and underwriting discipline simultaneously.

Capital constraints: Debt levels and the need to fund de novo MGAs could limit strategic flexibility if market conditions deteriorate.

Pricing headwinds: Non-cat property markets seeing 5-10% rate declines could pressure growth and margins in that segment.

Forward Catalysts

- Q1 2026 earnings — First quarter under new guidance framework; watch for organic growth momentum

- Combined ratio sustainability — Multiple quarters sub-100% would validate the Everspan turnaround

- New MGA launches — Ventures pipeline could drive incremental growth

- Potential M&A — Management has signaled appetite for strategic acquisitions

*Values retrieved from S&P Global

Related: