Amrize (AMRZ)·Q4 2025 Earnings Summary

Amrize Announces $1B Buyback as Building Materials Powers Through Soft Housing

February 17, 2026 · by Fintool AI Agent

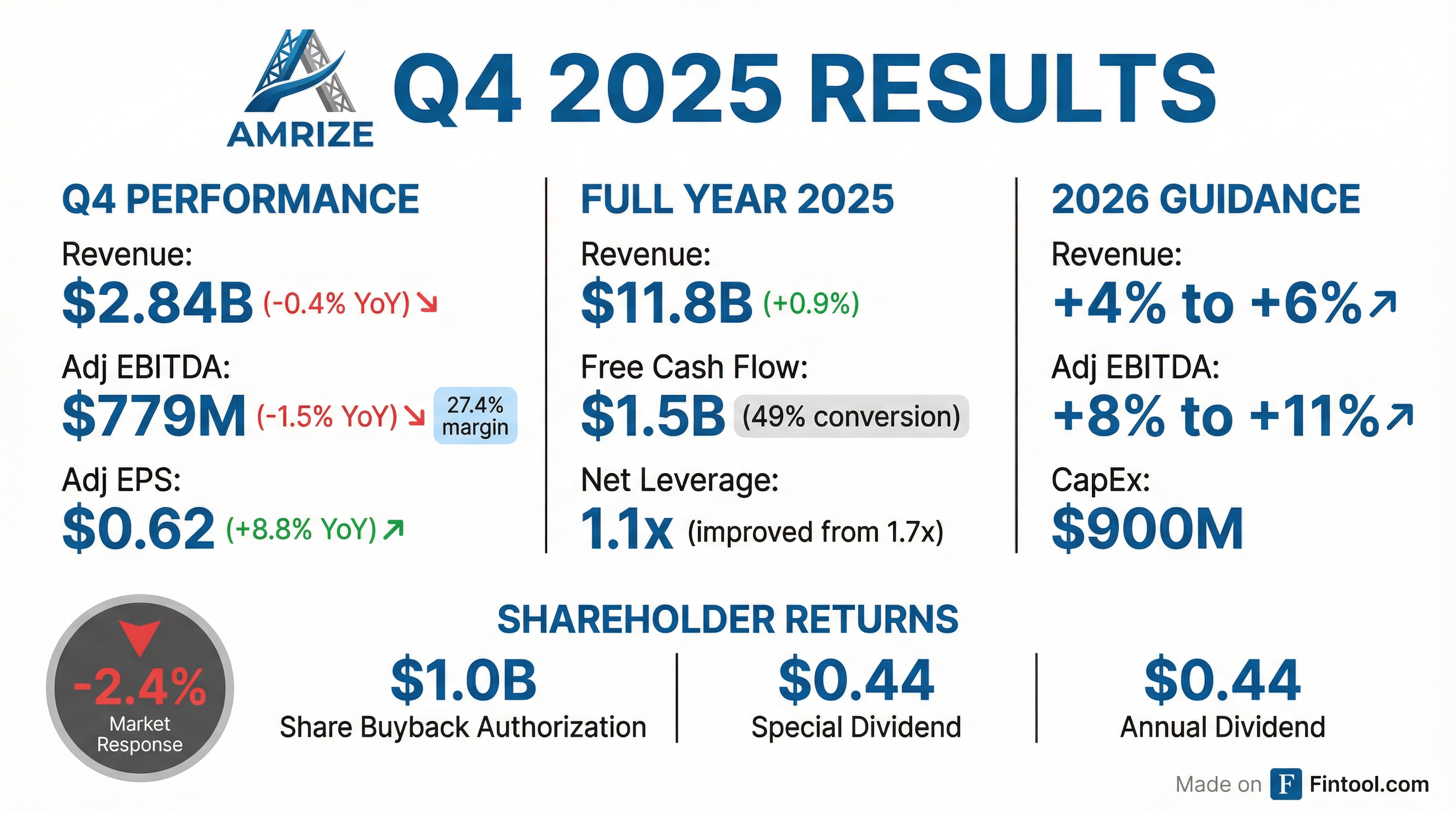

Amrize (AMRZ) delivered a mixed Q4 2025 with Building Materials strength offsetting continued weakness in Building Envelope. The construction materials company reported revenue of $2.84B (-0.4% YoY) and Adjusted EBITDA of $779M (-1.5% YoY) . The headline story: management announced a robust shareholder return program including a $1.0B share repurchase authorization and $0.88/share in dividends, signaling confidence in the company's cash generation post-spinoff .

Did Amrize Beat Earnings?

Limited analyst coverage makes consensus comparison difficult for this recent Holcim spinoff. However, the reported results show a tale of two segments:

For the full year, Amrize delivered $11.8B in revenue (+0.9% YoY), $3.0B in Adjusted EBITDA (-5.5% YoY), and $1.5B in Free Cash Flow with 49% cash conversion .

What Changed From Last Quarter?

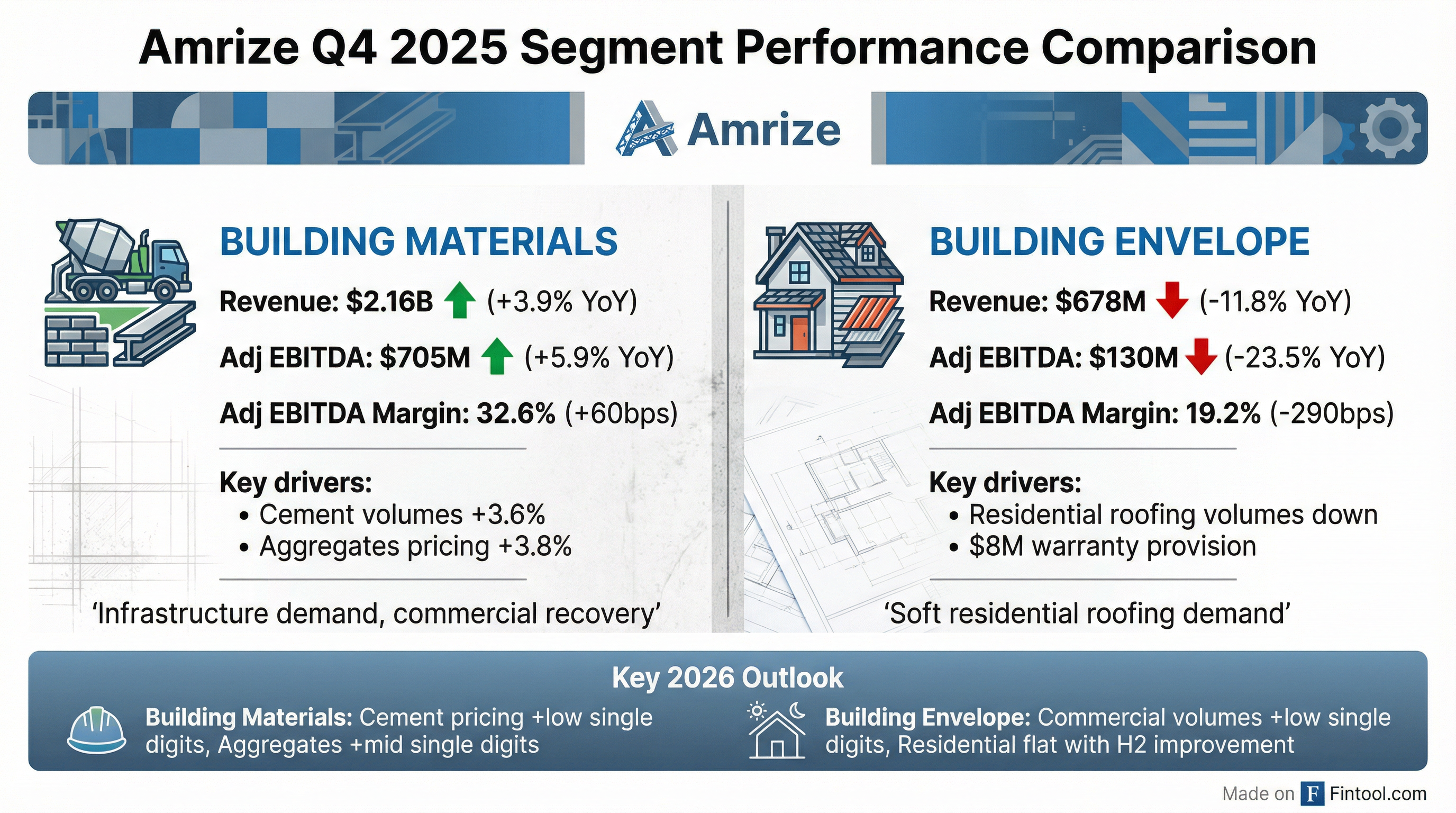

Building Materials accelerated: Revenue grew +3.9% in Q4 vs +8.7% in Q3, but critically, Adjusted EBITDA margin expanded 60bps to 32.6% . Cement volumes rose 3.6% with aggregates pricing up 3.8% (freight-adjusted) .

Building Envelope deteriorated: The segment saw revenue decline -11.8% (vs -0.7% in Q3) with Adjusted EBITDA down -23.5% . Residential roofing demand remained soft while an $8M warranty provision increase further pressured margins .

Balance sheet strengthened materially: Net leverage improved to 1.1x (vs guidance of <1.5x), down from 1.7x at Q3-end . Net debt declined to $3.35B from $4.99B in Q3 .

What Did Management Guide?

Amrize issued 2026 guidance calling for accelerating growth and margin expansion:

Key drivers for 2026:

- Building Materials: Cement pricing up low-single digits, aggregates pricing up mid-single digits, positive volume growth across both

- Building Envelope: Commercial roofing volumes up low-single digits, residential flat with improvement expected in H2

- ASPIRE program: Targeting 70bps of margin expansion in 2026, on track for $250M+ in synergies through 2028

Shareholder Return Program

The Board announced a comprehensive capital return program :

- $1.0B share repurchase authorization (12-month expiration, pending AGM approval)

- $0.44 special one-time dividend (pending AGM approval)

- $0.44 annual ordinary dividend (paid in quarterly installments)

Dividends will be paid from capital contribution reserves and are not subject to Swiss withholding tax .

CEO Jan Jenisch emphasized capital allocation priorities: "We are delivering on our commitment to invest for growth and create value for all stakeholders. We are well positioned in our $200 billion addressable market."

How Did the Stock React?

AMRZ shares fell 2.4% on the day of the earnings release, closing at $57.39.

The muted reaction likely reflects:

- Mixed near-term results: Q4 EBITDA declined despite Building Materials strength

- Building Envelope overhang: Continued residential weakness with no near-term recovery expected

- Positive guidance offset: Strong 2026 outlook (+8-11% EBITDA growth) and shareholder returns provided a floor

The stock trades at $57.39 vs. a 52-week range of $44.12 - $60.57, with shares up significantly since the Holcim spinoff in May 2025.

Key Segment Details

Building Materials (72% of Q4 Revenue)

Growth drivers: Infrastructure demand continued with federal and state-level projects, only ~50% of IIJA funding allocated to date . Commercial market improving with strong data center and energy project demand .

Organic growth investments:

- Completed 660,000-ton capacity expansion at Ste. Genevieve cement plant (North America's largest)

- PB Materials acquisition (West Texas aggregates, >$180M revenue) expected to close Q1 2026

Building Envelope (24% of Q4 Revenue)

Headwinds: Residential roofing demand remained soft with new construction weak. Commercial repair and refurbishment (R&R) showed resilience but couldn't offset the residential decline .

2026 outlook: Management expects lower interest rates to support new residential construction recovery "by late 2026 at the earliest" with U.S. housing shortage driving long-term growth .

ASPIRE Program Update

Amrize's synergy program is progressing ahead of plan :

- 450+ new logistics and service providers onboarded

- 400+ optimization projects underway across raw materials, services, logistics, equipment

- Initial savings realized in Q4 2025

- 2026 target: 70bps of margin expansion

- Through 2028: $250M+ in cumulative synergies

What Should Investors Watch?

Near-term catalysts:

- PB Materials acquisition closing (Q1 2026)

- Malarkey shingle factory commissioning in Indiana (end of 2026)

- AGM approval of buyback and dividends

Key risks:

- Residential roofing recovery timing remains uncertain

- Building Envelope margins under pressure

- Execution on ASPIRE synergy targets

Positive signals:

- Net leverage at 1.1x provides significant M&A and buyback capacity

- Infrastructure tailwinds continue with IIJA funding

- Commercial market recovery underway

Amrize Ltd (NYSE: AMRZ) is a construction materials company spun off from Holcim in May 2025, operating Building Materials (cement, aggregates, ready-mix) and Building Envelope (roofing systems) segments across North America.

Related: AMRZ Company Profile | Q3 2025 Earnings | Earnings Transcript