Apellis Pharmaceuticals (APLS)·Q4 2025 Earnings Summary

Apellis Reaches Profitability as EMPAVELI Launch Accelerates, But SYFOVRE Declines Weigh on Shares

February 24, 2026 · by Fintool AI Agent

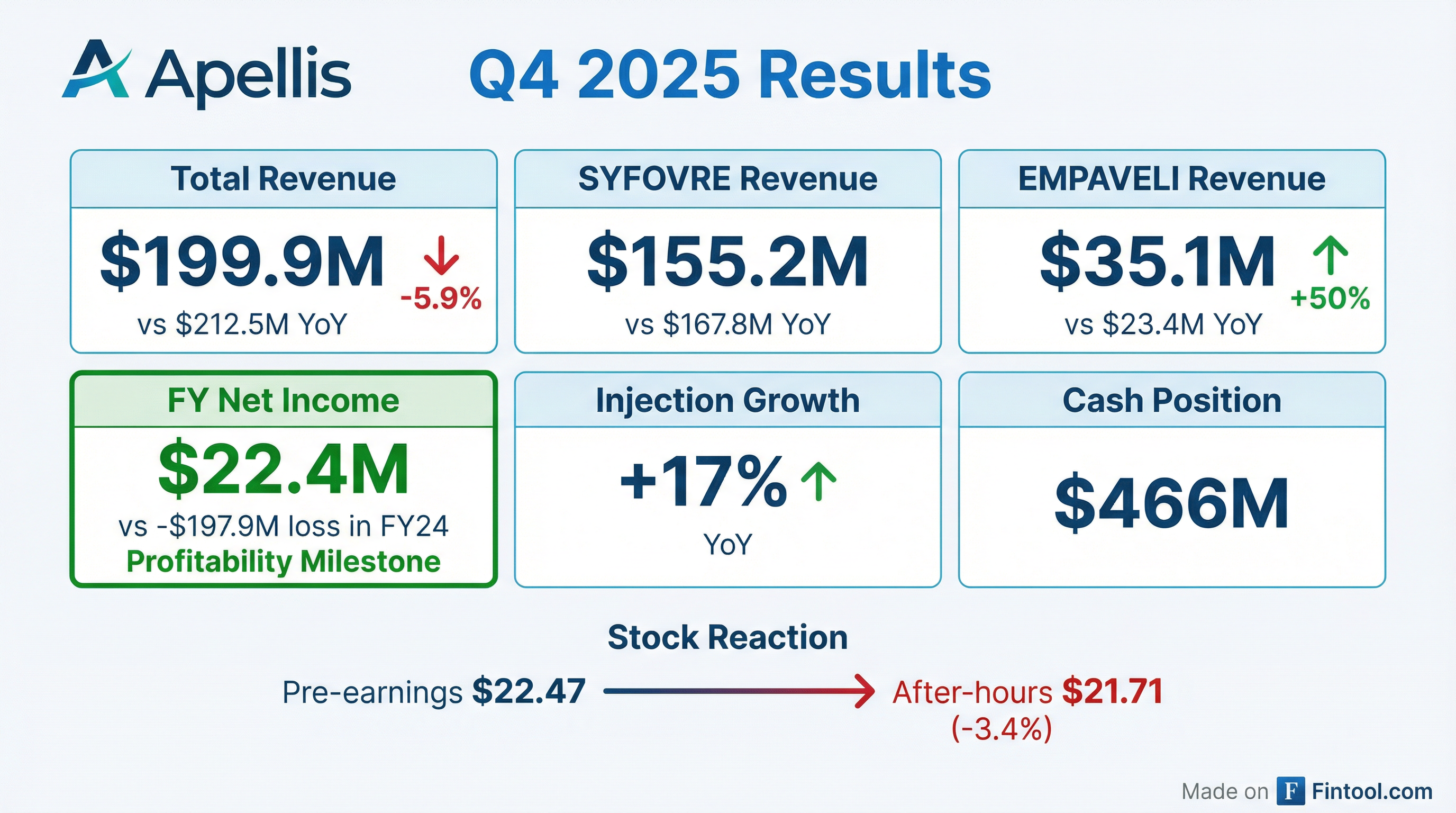

Apellis Pharmaceuticals (APLS) reported Q4 2025 results showing a mixed picture: the company achieved its first-ever profitable year, but core product SYFOVRE continued its revenue decline, sending shares down ~3.4% in after-hours trading.

The complement therapeutics company reported total revenue of $199.9M in Q4, down from $212.5M in the year-ago quarter, driven primarily by lower SYFOVRE sales. However, the full-year picture tells a more nuanced story: FY 2025 total revenue hit $1.0B (up from $781M in 2024), and net income flipped to $22.4M from a loss of $197.9M.

Did Apellis Beat Earnings?

The quarter disappointed on the top line. Q4 2025 total revenue of $199.9M represented a 5.9% decline year-over-year.

Full-year 2025 was a milestone. Despite the Q4 miss, FY 2025 marked the company's first profitable year:

The swing to profitability was largely driven by $314.4M in licensing revenue, including a one-time $275M upfront payment from the Sobi royalty repurchase agreement recorded in Q3 2025.

How Did the Stock React?

APLS closed at $22.47 on February 23 before earnings and dropped to $21.71 in after-hours trading, a decline of approximately 3.4%. This continues a volatile pattern around earnings:

The Q3 2025 earnings reaction was particularly brutal, with shares dropping nearly 17% despite the Sobi deal. The current after-hours decline suggests continued investor concern about SYFOVRE trajectory.

What Changed From Last Quarter?

SYFOVRE: Volume Up, Revenue Down

The GA franchise showed a divergence between volume and revenue metrics:

- Total injections up 17% YoY — reflecting continued strong underlying demand

- Revenue down 7.5% YoY — indicating pricing pressure or mix shift

- ~60% market share in U.S. GA market maintained

- 102K doses delivered in Q4 (89K commercial, 13K free goods)

EMPAVELI: C3G/IC-MPGN Launch Gaining Traction

The rare kidney disease launch is showing strong early momentum:

- 267 cumulative patient start forms as of year-end

- >5% penetration of U.S. C3G/IC-MPGN patient population

- 95% payer policies covering to label or with minimal restrictions

- Zero meningococcal infections — strong safety profile maintained

- Patient pipeline larger than pre-launch — upstream identification continues to grow even as patients convert to treatment

CEO Cedric Francois highlighted this as a "blockbuster opportunity" in rare kidney diseases, with potential to reach 50% of the ~5,000 U.S. patients (split ~50/50 between C3G and IC-MPGN).

Launch dynamics: The company confirmed the initial patient bolus has cleared and they've transitioned to steady-state growth. Strong interest noted particularly in pediatric, post-transplant, and IC-MPGN patient segments where Empaveli has differentiated positioning vs. competitor Fabhalta.

What Did Management Guide?

Management did not provide specific revenue guidance but emphasized:

-

Path to Profitability: "Apellis anticipates its cash, cash equivalents and projected product revenues will be sufficient to fund the business to profitability"

-

SYFOVRE Growth Initiatives:

- Prefilled syringe regulatory submission planned for 1H 2026

- OCT-F AI imaging tool expected for research use in 2H 2026

- Phase 2 SYFOVRE + APL-3007 topline data expected in 2027

-

Pipeline Progress:

- FSGS and DGF pivotal trials underway

- APL-9099 (FcRn base editing therapy) IND planned 2H 2026

Key Management Quotes

On strategic positioning:

"2025 was a year of disciplined execution and meaningful progress across the business, and we enter 2026 with clear priorities and a strong foundation. We are focused on positioning SYFOVRE for its next phase of growth, maximizing EMPAVELI's blockbuster opportunity in rare kidney diseases, and advancing a differentiated, self-funded pipeline leveraging our deep expertise in C3 biology." — Cedric Francois, CEO

On EMPAVELI's blockbuster trajectory:

"Empaveli is on a clear path to blockbuster status... it could ultimately be used by up to half of U.S. C3G and primary IC-MPGN patient population." — David Acheson, EVP Commercial

On functional OCT technology:

"Physicians are really excited for this technology, finally, to have a way to link structure to function... This will help with earlier diagnosis of GA [and] help physicians support the patient's journey." — Dr. Caroline Baumal, CMO

On free goods commitment:

"In 2025, we made a deep commitment as a company to support the retina practices to deal with patients being in a position where they could not afford the copay on their products, and to make sure that these patients would not go without treatment. That is our medical commitment to patients." — Cedric Francois, CEO

Balance Sheet and Cash Position

Cash increased $55M year-over-year, and equity improved by $142M, reflecting the profitable year.

Q&A Highlights

On EMPAVELI's 50% penetration target:

"We believe that up to 50% of the epidemiology would be patients that could end up being treated with Empaveli... the appreciation for the efficacy and safety profile of the drug really stands out." — Cedric Francois, CEO

Management estimates ~5,000 U.S. patients with C3G and IC-MPGN, split roughly 50/50 between the two indications. The company has achieved >5% penetration after just one full quarter — one of the strongest rare disease launches in nephrology.

On launch dynamics (bolus vs steady state): David Acheson confirmed the initial patient bolus hit early in the launch, and the company has now transitioned to steady-state growth: "Now we're at that steady state place that we talked about... I would be confident in the continued steadiness of what we're going to see moving forward."

On SYFOVRE Q1 2026 expectations: CFO Tim Sullivan noted Q1 will see "a bit of a modest swing" due to seasonal dynamics (weather, Medicare reverifications) and deliberate inventory management, but "much more muted than last year."

On GALE 5-year data:

"Patients who are on treatment for 5 years can save as much as one and a half year of tissue. That's an enormous benefit to 70 or 75-year-old individual who depends so much on their vision." — Cedric Francois, CEO

On prefilled syringe competitive advantage:

"Having a prefilled syringe on the market makes a very important competitive advantage... it will be a very important driver of share." — Cedric Francois, CEO

On competitive positioning: SYFOVRE maintains ~60% market share in the U.S. GA market. Management expressed confidence in their data leadership, noting "nobody else has that data" referring to 5-year GALE results.

Risks and Concerns

-

SYFOVRE Revenue Trajectory: Full-year SYFOVRE revenue declined from $611.8M in 2024 to $586.9M in 2025 despite injection growth, suggesting ongoing pricing pressure or competitive dynamics with Astellas/Iveric's Izervay

-

One-Time Boost: FY 2025 profitability was heavily aided by the $275M Sobi payment; underlying product revenue actually declined 2.9%

-

Q4 Net Loss Widened: Q4 2025 net loss was $58.9M vs $36.4M in Q4 2024, driven by higher SG&A expenses

-

Operating Expenses Rising: SG&A increased from $121.5M in Q4 2024 to $147.1M in Q4 2025 (+21%)

-

Convertible Debt Maturity: ~$94M of convertible debt matures in September 2026. Management is "actively evaluating a range of alternatives to address this obligation."

-

Gross-to-Net Pressure: SYFOVRE gross-to-net expected in high 20% range for 2026, reflecting normal buy-and-bill market evolution.

Forward Catalysts

Bottom Line

Apellis delivered its first profitable year, but the achievement rings somewhat hollow given its reliance on the Sobi one-time payment. Core product SYFOVRE continues to see revenue pressure despite strong injection growth, while the EMPAVELI rare kidney launch shows genuine promise with >5% market penetration already achieved.

The stock's 3.4% after-hours decline reflects investor skepticism about whether SYFOVRE can return to growth and whether EMPAVELI can scale fast enough to offset the GA headwinds. Key near-term catalysts include the prefilled syringe approval, which could improve clinic workflow and boost adoption.

View Apellis company profile | Q4 2025 Earnings Transcript | Q3 2025 Earnings