ARM HOLDINGS PLC /UK (ARM)·Q3 2026 Earnings Summary

Arm Holdings Delivers Record Q3 as Data Center Soars 100%+ YoY, Stock Drops 10% After-Hours

February 4, 2026 · by Fintool AI Agent

Arm Holdings delivered a record-breaking third quarter with revenue of $1.24 billion, up 26% year-over-year, marking the company's fourth consecutive billion-dollar quarter . Non-GAAP EPS came in at $0.43, near the high end of guidance . However, the stock dropped approximately 10% in after-hours trading as investors digested guidance for decelerating royalty growth and potential memory supply chain headwinds.

Did Arm Beat Earnings in Q3 FY2026?

Yes — Arm beat on both revenue and earnings. The company delivered its best quarter in history across multiple metrics:

Data from earnings call . Values retrieved from S&P Global.

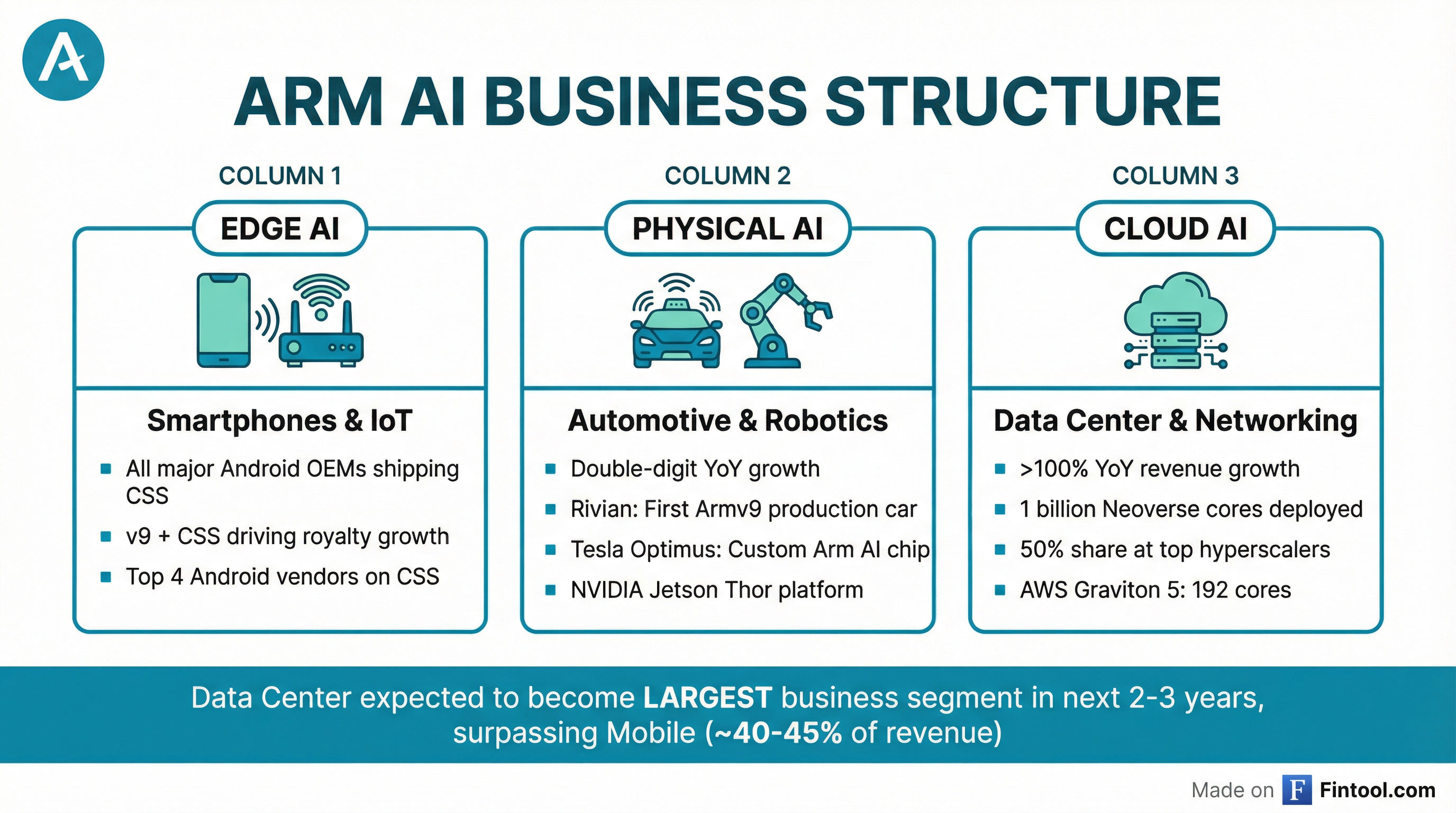

Royalty revenue was the standout, growing 27% to a record $737M, driven by "record units with strength across AI and general-purpose data center" . CFO Jason Child noted that royalty growth continues to outpace the overall smartphone market as "all the major Android OEMs are now ramping smartphones with chips based on both Armv9 and CSS" .

License revenue of $505M included a $200M contribution from SoftBank for technology licensing and design services, up from $178M the prior quarter due to the full-quarter impact of agreements signed previously .

What Did Management Guide for Q4?

Guidance beat consensus but showed royalty deceleration — the key concern for investors.

Forward estimates retrieved from S&P Global.

The Q4 revenue guidance of ~$1.47B implies full-year FY2026 revenue growth of approximately 22%, above the company's prior target of "at least 20%" . However, the royalty guidance of "low teens" growth represents a significant deceleration from Q3's 27% growth rate.

CFO Jason Child addressed the deceleration, noting it's "much more about kind of what we're comping and, to some extent, seasonality" rather than fundamental weakness . He specifically cited an "unusual timing" MediaTek chip launch in Q4 FY2025 that creates a tough year-over-year comparison.

How Did the Stock React?

The stock closed up 0.3% during regular trading but dropped ~10% after-hours.

The after-hours selloff appears driven by:

- Royalty growth deceleration: Q4 guidance for "low teens" growth vs. Q3's 27%

- Memory supply chain concerns: MediaTek cited ~15% unit volume reduction expectations for next year

- Elevated expectations: Stock had already rallied significantly from its 52-week low of $80

CFO Child attempted to mitigate memory concerns, estimating that even a 20% reduction in smartphone volumes would translate to only a "1%, maybe 2% negative impact on total royalties" due to Arm's higher royalty rates on premium and flagship devices .

What Changed From Last Quarter?

Data center momentum accelerated while smartphone faces near-term headwinds.

Data Center: The Breakout Story

CEO Rene Haas made a bold prediction: "We expect in a few years our data center business to be our largest business, larger than mobile" . Key developments:

- Data center royalty revenue grew >100% YoY for another quarter

- Neoverse CPUs surpassed 1 billion cores deployed

- Arm's share at top hyperscalers expected to reach 50%

- Major new products announced:

- AWS Graviton 5: 192 cores (2x Graviton 4)

- NVIDIA Vera CPU: 88 cores (up from 72 in Grace)

- Microsoft Cobalt 200: 132 cores on Neoverse CSS V3

- Google Axion N4A: 2X better price performance vs. x86

Data center revenue is now "in the teens to probably getting closer to 20%" of total revenue, up from "just double digit" at the start of the year .

Compute Subsystems (CSS): Expanding Moat

CSS continues to exceed expectations with momentum accelerating:

- 21 CSS licenses across 12 companies (2 new this quarter, both smartphone OEMs)

- 5 customers now shipping CSS-based chips, including 2 on second-generation platforms

- Top 4 Android smartphone vendors shipping CSS-powered devices

- CSS contribution now "well into double digits" of royalties, potentially reaching 50%+ over next few years

Business Reorganization

Arm reorganized around three AI-focused business units :

Key Management Quotes

On agentic AI driving CPU demand:

"Agent-based AI requires coordination across many agents running continuously, and that the CPU can only do coordination. As this model scales, customers need CPU chips with higher core counts and better power efficiency to operate continuously within tight power and cost constraints. This trend directly benefits Arm." — Rene Haas, CEO

On SoftBank's commitment to ARM:

"He is not interested in selling one share of Arm stock. And that doesn't mean two shares or three shares. That means any shares. He's very long on the company." — Jason Child, CFO (quoting Masa Son)

On FY2027 outlook:

"For 2027, not guiding on full year, but in terms of kind of at a high level, the 20% growth rate, I think, certainly is very reasonable and not anything that we'd back away from." — Jason Child, CFO

Q&A Highlights

Memory Supply Chain Impact: MediaTek expects ~15% reduction in smartphone unit volumes for next year due to memory constraints. However, CFO Child estimates this translates to only 1-2% revenue impact because constraints will primarily affect low-end devices (v8 and older) where Arm earns minimal royalties. Premium/flagship devices (CSS and v9) are being protected .

CSS Pricing Pressure: When asked if bill-of-materials pressure could slow CSS adoption, CEO Haas was emphatic: "No, we're not seeing any of that at all." The time-to-market value of CSS (typically cuts design cycles in half) outweighs any BOM considerations .

AI Impact on Arm's Business: Haas noted that "AI is not going to replace a physical chip anytime soon" and emphasized that "every single end application is going to be impacted by AI. And because the vast majority of the compute platforms out there today are already Arm-based, it gives us a gigantic opportunity" .

Risks and Concerns

- Royalty growth deceleration: Q4 guidance of "low teens" growth is a meaningful step-down from Q3's 27%

- Memory supply constraints: Potential headwind to smartphone volumes in FY2027

- High R&D spending: Operating expenses up 37% YoY, growing faster than revenue

- SoftBank overhang: Despite denials, market uncertainty persists about potential share sales

- Valuation: Stock trades at premium multiples requiring continued strong execution

Forward Catalysts

- March 24th Event: Arm is hosting an event where announcements are expected, though management declined to preview details

- FY2027 Guidance: Full-year outlook expected in May earnings

- Data Center Inflection: Continued market share gains from x86

- Physical AI Ramp: Automotive and robotics design wins moving to production

- Memory Normalization: Resolution of supply constraints could boost smartphone volumes

Historical Performance

Revenue in millions. Values retrieved from S&P Global.

This analysis was generated by Fintool AI Agent based on Arm Holdings' Q3 FY2026 earnings call held February 4, 2026.