AtriCure (ATRC)·Q4 2025 Earnings Summary

AtriCure Beats on Revenue and EPS as Profitability Inflection Takes Hold

February 17, 2026 · by Fintool AI Agent

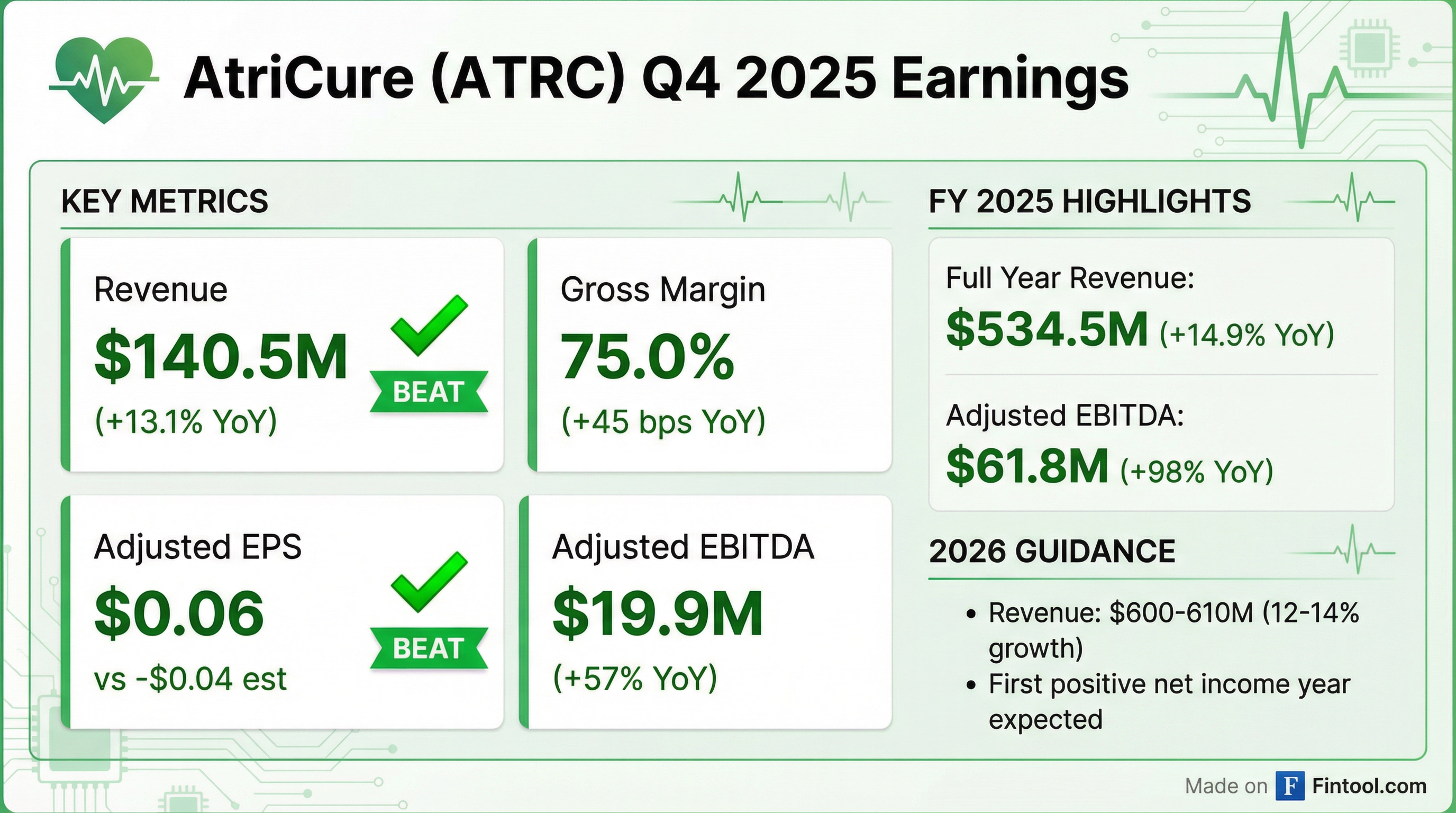

AtriCure delivered a clean beat in Q4 2025, posting revenue of $140.5 million (+13.1% YoY) that topped consensus estimates while flipping to positive adjusted earnings . The medical device company continues its march toward sustained profitability, guiding for its first positive net income year in 2026. Full year 2025 revenue hit $534.5 million (+14.9% YoY) with adjusted EBITDA nearly doubling to $61.8 million .

Did AtriCure Beat Earnings?

Yes — AtriCure beat on both revenue and EPS.

*Values retrieved from S&P Global

The standout here is the EPS flip. AtriCure went from a -$0.08 adjusted loss per share in Q4 2024 to +$0.06 profit — a $0.14 swing driven by operating leverage and disciplined expense management .

Beat/Miss History (Last 8 Quarters)

AtriCure has beaten revenue estimates in 8 consecutive quarters:

*Values retrieved from S&P Global

What Did Management Guide for 2026?

AtriCure raised the bar for 2026, projecting its first year of positive net income :

Consensus for FY 2026 stood at $602M revenue and -$0.03 EPS prior to this report, so management is guiding ahead of the Street on profitability.*

The guidance implies continued margin expansion as the company scales. CEO Michael Carrel emphasized the strategic pivot: "Entering 2026, we remain focused on driving durable growth, expanding margins and executing on strategic priorities that enhance AtriCure's leadership position across our markets."

What Changed From Last Quarter?

Several key inflections emerged in Q4:

1. Profitability Inflection Confirmed

- Q4 2025 operating income: +$2.5M vs -$14.5M in Q4 2024

- First quarterly GAAP profit in recent history: $1.8M net income

- Operating expenses as % of revenue declining — operating leverage kicking in

2. Product Mix Improving

- cryoSPHERE MAX and AtriClip FLEX-Mini driving U.S. growth

- EnCompass clamp gaining traction in open ablation

- Pain management revenue: +27% YoY in Q4 (from $17.8M to $22.6M)

3. International Acceleration

- International revenue: +15.3% (+9.9% constant currency)

- Growth across most key international markets

- International now 19% of total revenue

4. Clinical Pipeline Advancing

- LEAPS trial completed enrollment of 6,573 patients ahead of schedule; DSMB passed 50% event rate with "thumbs up" to continue

- BOX X NoAF trial initiated — 960-patient RCT targeting postoperative AFib in non-AFib cardiac surgery patients

- Dual-Energy EnCompass — First-in-human treatments completed in December with "excellent results"; combines RFA with PFA

5. STS Quality Metric — Major Catalyst

Concomitant AFib treatment is no longer optional — it will become a quality metric in Star Ratings by early next year . This is only the second time in 25 years that a therapeutic treatment has become a quality metric in cardiac surgery. This regulatory tailwind should accelerate adoption of AtriCure's EnCompass clamp and AtriClip devices in underpenetrated CABG procedures

Segment Deep Dive

AtriCure reports across four product lines. Here's Q4 2025 performance:

Source: Calculated from U.S. + International segment data

Pain Management (+24% Q4, +33% full year) and Open Ablation (+17% Q4 and FY) are the growth engines . Minimally Invasive declined 26% for the full year as PFA catheters dominate standalone AFib treatment .

Key Account Metrics:

- 830+ EnCompass accounts worldwide (mid-teens increase over 2024)

- ~500 cryoSPHERE MAX accounts in US

- 300+ FLEX MINI accounts — contributed 18% of worldwide LAA revenue in 2025

- EnCompass now >60% of US open ablation revenue

- 100,000+ patients treated with cryoSPHERE probes since 2019 launch

Geographic Mix

How Did the Stock React?

ATRC shares are trading at $32.97, up +1.0% on the day as of market close . The earnings release hit after market hours, so the full reaction will play out in after-hours and tomorrow's session.

The stock is 15% below its 50-day average and 24% below its 52-week high, suggesting the market hasn't yet priced in the profitability inflection. The guidance for first positive net income year could be a catalyst for multiple re-rating.

Historical Earnings Reactions

AtriCure has historically seen muted same-day reactions but tends to grind higher post-earnings on execution:

- Stock +29% over past 12 months despite recent pullback

- 8-quarter beat streak should build confidence in management credibility

What Did Management Say About the New Competitor?

A major competitor (likely Edwards Lifesciences or Abbott) announced entry into the LAA clip market, causing ATRC shares to decline. CEO Mike Carrel addressed this head-on during the Q&A:

"We kind of take it in a really positive way, that it validates our market. It tells you that you've got two major top five medical device companies that have decided that cardiac surgery is a market that matters... We've established a leadership position in this market, and we're pretty proud of that."

AtriCure's competitive moat:

- 10th generation product — continuous innovation since inception

- 750,000+ implants with 0.007% safety complication rate

- 21,000+ patients studied across 100+ peer-reviewed publications

- LEAPS trial exclusivity — only AtriClip included in the 6,573-patient trial

- 300+ person field force with deep domain expertise

Management noted that when a prior competitor entered the space, AtriCure's growth rate actually accelerated — open LAA grew 24% in 2025 . Guidance already contemplates "very mild competitive pressures" in the back half of 2026 .

Key Risks and Concerns

- Competitive Entry — New LAA clip competitor expected mid-2027; management confident but impact uncertain

- Minimally Invasive Decline — Hybrid AFib therapy down 26% in 2025 as PFA catheters dominate standalone treatment

- UK Reimbursement — NHS pulled pain management reimbursement; UK revenue dropped from $4M/quarter to ~$3M in Q4. Management expects UK uncertainty to persist through 2026

- Q1 2026 Seasonality — Revenue expected flat to slightly down sequentially; net cash burn anticipated in Q1 before positive cash generation resumes

- Clinical Trial Execution — LEAPS and BOX X NoAF trials need to hit efficacy endpoints for label expansion

Balance Sheet Snapshot

AtriCure enters 2026 with a strong balance sheet :

Cash increased $44.7M during 2025, reflecting positive cash generation. Management expects continued positive cash generation in 2026 .

What to Watch Going Forward

- Q1 2026 Results — Revenue expected flat to slightly down sequentially; net cash burn anticipated before positive cash generation resumes

- LEAPS Trial 75% Event Rate — Next DSMB readout expected; 100% events trigger trial completion

- Hybrid AFib Stabilization — Sequential improvement from Q3→Q4 is encouraging; watch for sustained account additions

- CryoXT Ramp — Expected to contribute more meaningfully to revenue in back half of 2026

- Dual-Energy EnCompass — Clinical trial initiation expected in 2026; combines RFA with PFA

- UK Reimbursement Resolution — Pain management and MIS ablation procedures impacted; uncertainty expected through 2026

Long-Term Targets (2028-2030)

Management reiterated confidence in exceeding their long-range plan :

At the current pace, AtriCure is tracking ahead of these targets — FY 2025 already hit 11.6% EBITDA margin vs the 2028 target of 14%

Q&A Highlights

On market opportunity:

"Globally, there's 2 million patients that undergo cardiac surgery, and in 2025, we treated about 50,000. So we're still obviously very underpenetrated in that market." — CEO Mike Carrel

On CABG penetration:

"About 20% of those patients [with AFib undergoing CABG] get treated. But if you look at it in totality, when you start to think about BOX X NoAF... that number is obviously much less than 10%."

On CryoXT rollout strategy:

"We want to make sure that we get it right, that we get feedback from them, that we learn from them as we kind of roll it out to additional sites... By the end of this year or middle of this year, we do anticipate that we're going to open that up quite a bit."

On bottom-line trajectory:

"Super pleased with the progress on the bottom line... would expect to well exceed kind of the 2028 goal here in the near term from an Adjusted EBITDA perspective." — CFO Angie Wirick

The Bottom Line

AtriCure delivered a quality quarter that extends its beat streak to 8 consecutive quarters on revenue. The real story is the profitability inflection — the company posted its first quarterly GAAP profit and is guiding for its first positive net income year in 2026.

The new competitor entry creates headline risk, but management made a compelling case for their competitive moat: 10th-generation products, 750K+ implants with exceptional safety, $100M+ invested in clinical evidence (LEAPS, BOX X NoAF), and a 300+ person field force with unmatched domain expertise. The STS quality metric news is an underappreciated catalyst that should accelerate adoption in the underpenetrated CABG segment.

With strong product adoption in pain management (+33% FY) and open ablation (+17% FY) offsetting minimally invasive declines, the growth algorithm remains intact. At ~19x forward adjusted EBITDA (implied from guidance midpoint), the valuation looks reasonable for a company finally crossing into profitability with a clear path to $1B revenue by 2030.

For more on AtriCure, see the company page or read the Q4 2025 earnings transcript.