AVANOS MEDICAL (AVNS)·Q4 2025 Earnings Summary

Avanos Medical Beats on Revenue and EPS as SNS Segment Delivers Above-Market Growth

February 24, 2026 · by Fintool AI Agent

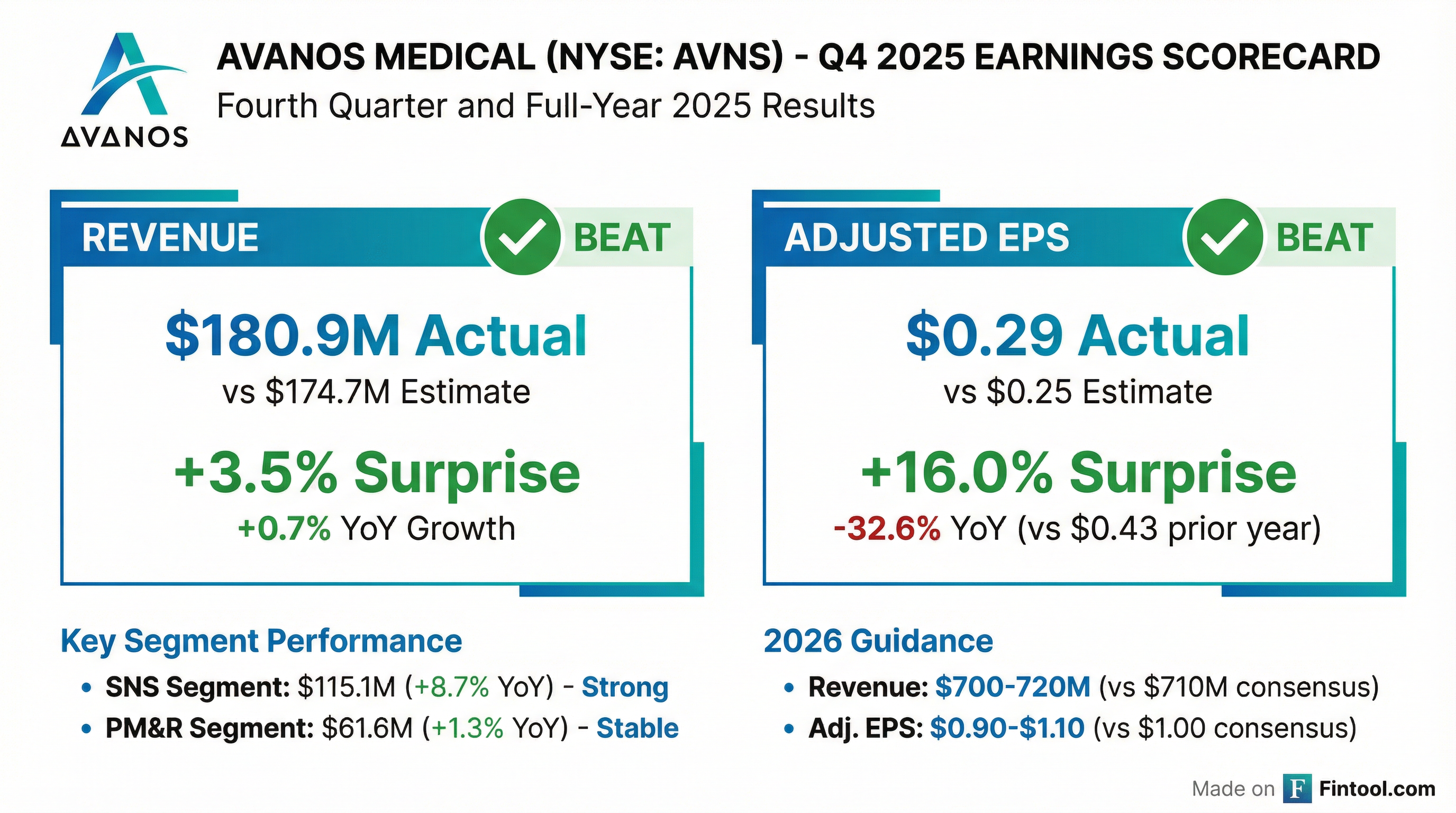

Avanos Medical (NYSE: AVNS) reported Q4 2025 results this morning that exceeded both top and bottom line estimates. Revenue of $180.9M beat consensus by 3.5% while adjusted EPS of $0.29 came in 16% above the Street, driven by continued strength in the Specialty Nutrition Systems segment which delivered 8.7% year-over-year growth.

CEO David Pacitti highlighted "meaningful progress on our strategic priorities," noting that organic growth in strategic segments reached 6% for the full year. The company expanded its transformation initiatives, now expected to deliver $15-20 million of incremental annualized savings by end of 2026.

Did Avanos Beat Earnings?

Yes — both revenue and EPS exceeded expectations:

*Consensus estimates from S&P Global

The company exceeded full-year revenue guidance and achieved the top end of EPS guidance, capping a year in which the strategic SNS and PM&R segments delivered 6% organic growth.

What Changed From Last Quarter?

Sequential improvement across key metrics:

- Revenue momentum: Q4 revenue of $180.9M improved from $177.8M in Q3 2025 (+1.7% sequential)

- Adjusted EBITDA recovered: $28.0M in Q4 vs $9.9M in Q3, reflecting better cost absorption and reduced restructuring noise

- SNS continues outperforming: Enteral feeding grew 10.7% YoY in Q4 vs 8.6% for full year, showing acceleration

- PM&R operating income surged: $5.2M in Q4 (+33.3% YoY) vs $9.2M full-year, demonstrating improving unit economics

Full-Year 2025 vs 2024 Comparison:

The year-over-year declines in profitability reflect the HA product line divestiture impact and ongoing transformation costs, though underlying strategic segment trends remain healthy.

How Did the Stock React?

AVNS shares traded at $15.23 ahead of the announcement, down 1.5% on the day. The stock has rallied approximately 20% over the past month from the $12.70 level, suggesting some of the beat may have been anticipated. Year-to-date, shares are up significantly from the 52-week low of $9.30.

Valuation context: At current prices, AVNS trades at a market cap of ~$707M, implying roughly 1.0x FY26 revenue and 15x FY26 adjusted EPS at the midpoint of guidance.

What Did Management Guide?

2026 Outlook:

*Consensus estimates from S&P Global

Key guidance assumptions :

- GAAP diluted EPS expected at $0.48-$0.73

- Assumed additional $12M of tariff expenses vs 2025

- Assumed 29% effective tax rate

- Adjustments include ~$0.26-0.28 for intangibles amortization, ~$0.06-0.08 for restructuring/transformation charges

Segment-level guidance :

- Specialty Nutrition Systems: mid-to-high single digit growth

- Pain Management & Recovery: low-to-mid single digit growth

- Foreign exchange rates assumed near current levels

The guidance implies flat-to-modest overall revenue growth, as portfolio divestitures and the transition of the US Game Ready rental business create headwinds against organic growth in strategic segments.

Segment Performance

Specialty Nutrition Systems (SNS) — The Growth Engine

SNS delivered "above-market results" for both Q4 and full-year 2025. Full-year SNS revenue reached $432.9M (+9.2% YoY) with operating income of $82.6M (19% margin). The margin compression reflects cost pressures being addressed through transformation initiatives.

Growth drivers: UK go-direct transition, recent CORGRIP tube retention launch, and late-stage US ENFit adoption cycle contributed to broad-based portfolio demand.

Pain Management & Recovery (PM&R) — Profitability Improving

PM&R showed mixed revenue trends — Radiofrequency Ablation remains a bright spot (+8.2% YoY) while Surgical Pain & Recovery declined (-7.5%). However, segment operating income improved significantly, with full-year operating income of $9.2M vs $2.7M in 2024 — a 240% increase.

Growth drivers: Higher RFA procedural volumes and reimbursement tailwinds in the UK & Japan, plus the transition of the US Game Ready rental business contributed to improved profitability.

What's Driving the Transformation?

Management highlighted several strategic priorities:

- Cost Savings: Transformation initiatives expected to deliver $15-20M of incremental annualized savings by end of 2026

- Tariff Mitigation: Efforts described as "on track" — guidance assumes an additional $12M of tariff expenses vs 2025

- Portfolio Optimization: HA product line divested, US Game Ready rental business transitioned, exiting IV therapy business

- Strategic M&A: Completed synergistic acquisition of Nexus Medical

- Debt Reduction: Net debt improved to ~$11M (0.1x EBITDA) from $27M year-over-year

- Strategic Focus: Concentrating resources on SNS and PM&R growth opportunities

Tariff Mitigation: Deep Dive

Management provided extensive detail on tariff exposure and mitigation on the call:

2026 Tariff Impact: ~$30 million total

- Two-thirds (~$20M) is China-related neonatal syringe exposure

- Represents a $12M increase vs 2025, but bottom-line impact expected to be similar due to pricing actions and cost containment

China Exit Strategy — June 2026 Deadline:

- "We are very confident in our plan to have all syringe manufacturing operations and sourcing out of China by June of this year"

- Production transitioning to Tijuana, Mexico and Cambodia

- Accelerated CapEx ($25M in 2026) supports this transition

Trade Exemptions in Place:

- Nairobi Protocol exemption — covers long-term feeding tubes produced in Mexico

- USMCA coverage — 60-70% of Mexico-produced products qualify

- Syringes moving to Mexico will also qualify for USMCA

Margin Outlook: CFO Scott Gallivan noted: "We do expect in the second half, we'll see improved gross margin, and that'll continue into 2027, due to just the weight of the tariff impact in the first half."

The company is also monitoring the recent Supreme Court ruling on tariffs and subsequent administration actions, noting they will update investors once there is more clarity.

Nexus Medical Acquisition Update

The Nexus Medical acquisition (neonatal portfolio) is exceeding expectations:

- 2025 contribution: $5 million in revenue (in-line with initial expectations)

- 2026 outlook: Double-digit organic growth expected

- Integration: "Going very well" with robust sales pipeline

- Synergies: NICU sales team leverage working as planned

CEO Pacitti noted the company continues to "look for growth accretive transactions that can achieve similar results" — signaling continued M&A focus in the SNS segment.

Balance Sheet & Cash Flow

The decline in free cash flow reflects higher capital expenditures ($31.6M vs $17.8M) and the Apex acquisition. Cash generation remains healthy with net debt at just $10.7M — a strong balance sheet position for a company generating ~$700M in annual revenue.

Q&A Highlights

Key exchanges from the analyst Q&A with Citizens JMP:

On tariff confidence:

"The big date is being out by June... we haven't had the high degree of confidence that we have now that plan will be executed, and we will be out by June, and delivering product from Mexico and our other site in Cambodia." — CEO Dave Pacitti

On organic growth guidance:

"It's around 5% for organic for the consolidated level... mid to high single digits for SNS and low to mid single digits for PMNR on an organic basis." — CFO Scott Gallivan

On R&D approach: Management is changing their R&D model — more external/outsourced projects while maintaining similar percentage-of-sales spend. A next-generation product launch is expected in Q4 2026.

On SNS demand:

"Demand remains very high for our SNS portfolio... Nexus is doing better than expected. We feel very good about the performance. It was a really nice tuck-in." — CEO Dave Pacitti

On operating leverage: Management expressed "high degree of confidence" in their ability to drive continued operating leverage, with earnings expansion expected to outpace revenue growth in 2026 despite the $12M incremental tariff headwind.

Key Risks & Concerns

- Margin pressure: Gross margin declined to 47.5% in Q4 from 54.6% in the prior year period, though adjusted gross margin held at 53.4%

- Goodwill impairment: $77M impairment charge in Q2 2025 related to PM&R segment (following $436.7M in Q4 2024)

- Tariff exposure: Company cited "new or increased tariffs or other trade restrictions" as a risk factor

- Surgical Pain headwinds: Drug shortages affecting Surgical Pain and Recovery products mentioned as ongoing risk

- Reduced earnings power: Adjusted EPS guidance of $0.90-$1.10 is below FY25's $0.94, suggesting transformation costs continue to weigh

Forward Catalysts

- Citizens JMP Investor Conference — March 2026

- China exit completion — June 2026 deadline for syringe manufacturing transition

- Investor Day — June 23, 2026 in New York

- Q4 2026 product launch — Next-generation product expected

- Gross margin inflection — H2 2026 improvement expected as tariff headwinds ease

- Transformation savings realization — $15-20M incremental savings target by end of 2026

- SNS momentum — continued above-market growth could drive multiple expansion

Company Overview: Avanos Medical (NYSE: AVNS) is a medical device company focused on delivering clinically superior solutions in Specialty Nutrition Systems (enteral feeding, neonate care) and Pain Management & Recovery (surgical pain, radiofrequency ablation). Headquartered in Alpharetta, Georgia, Avanos operates in more than 90 countries.

Related Links: