BridgeBio Pharma (BBIO)·Q4 2025 Earnings Summary

BridgeBio Delivers Triple Phase 3 Wins as Attruby Sales Surge 35% QoQ

February 24, 2026 · by Fintool AI Agent

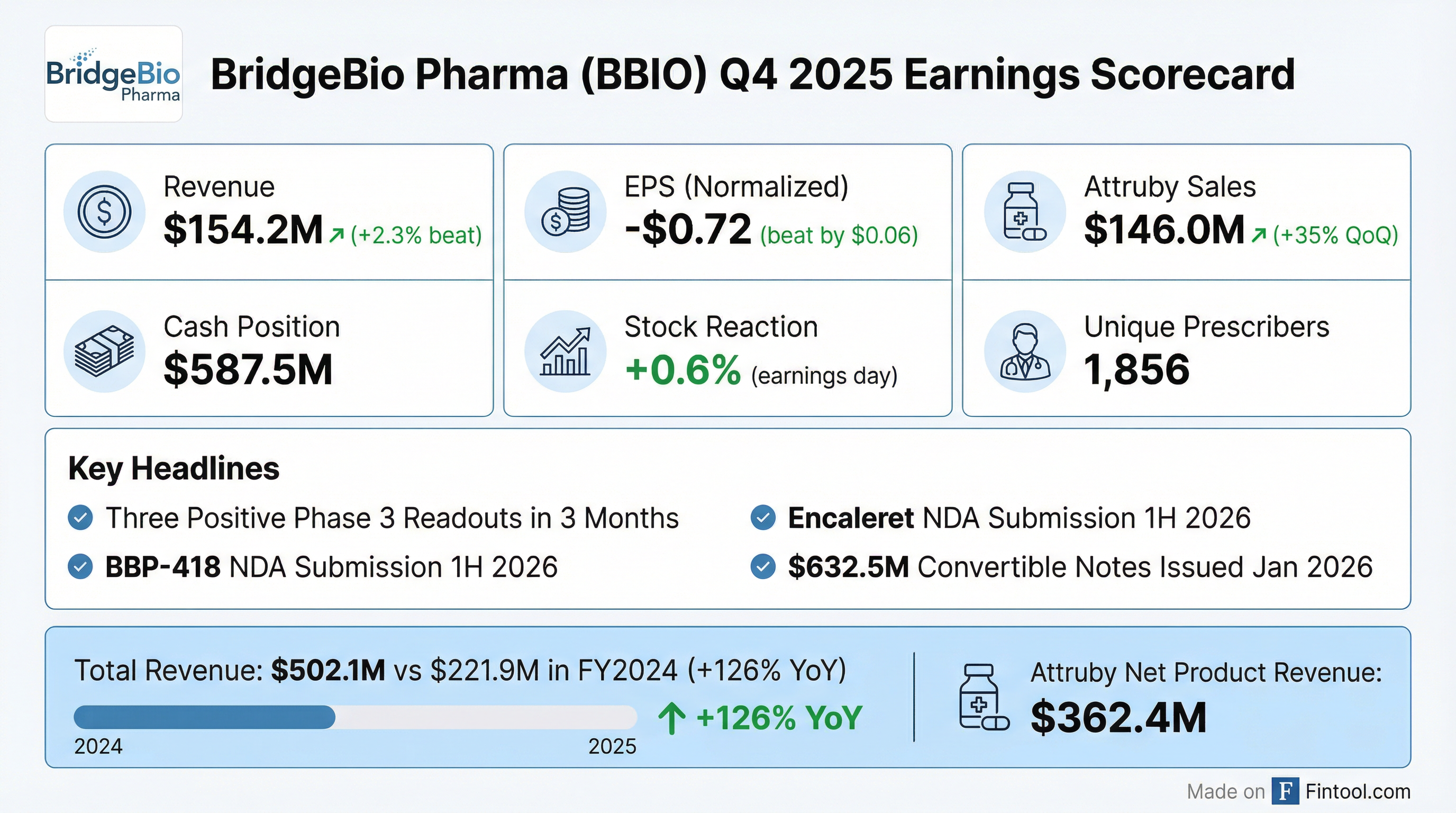

BridgeBio Pharma (BBIO) delivered a strong Q4 2025, beating revenue estimates with $154.2M in total revenue (+126% YoY) powered by Attruby's commercial momentum and punctuated by three consecutive Phase 3 wins that validate its pipeline strategy. The stock traded up modestly (+0.6%) on the day as investors weigh near-term losses against the transformational potential of multiple late-stage assets approaching commercialization.

Did BridgeBio Beat Earnings?

Revenue: Beat by ~2.3% — Q4 total revenue of $154.2M exceeded analyst estimates of ~$150.7M, driven by Attruby's commercial traction.

Normalized EPS: Beat by ~8% — Reported normalized EPS of -$0.72 came in better than consensus expectations of -$0.78, reflecting operating leverage despite continued pipeline investment.

The dramatic revenue transformation reflects BridgeBio's transition from development-stage to commercial-stage biotech following Attruby's November 2024 FDA approval.

What's Driving Attruby's Commercial Success?

Attruby (acoramidis) continues to establish itself as a first-choice therapy in ATTR-CM, demonstrating clinical differentiation as the only near-complete TTR stabilizer on the market (≥90% stabilization).

Key Commercial Metrics as of Feb 20, 2026:

- 7,804 unique patient prescriptions written

- 1,856 unique prescribers engaged

- 35% QoQ growth in net product revenue ($146M vs $108M in Q3)

- Repeat use and patient persistence exceeding company expectations

What management said:

"Attruby delivered 35% quarter-over-quarter growth in net product revenue in Q4, driven by its differentiated profile as the only near-complete stabilizer on the market, continued prescribing growth, repeat use, and patient persistence that has exceeded our expectations." — Matt Outten, Chief Commercial Officer

At AHA Scientific Sessions 2025, data showed acoramidis significantly reduces all-cause mortality through Month 42, including in the V142I variant population that disproportionately affects individuals of Western African ancestry.

Three Phase 3 Wins: What's Next for the Pipeline?

BridgeBio achieved a remarkable feat — three positive Phase 3 readouts in just over three months — validating its hub-and-spoke drug development model.

BBP-418 for LGMD2I/R9 (NDA 1H 2026)

FORTIFY achieved all primary and secondary endpoints with a statistically significant and clinically meaningful 2.6-point NSAD improvement vs placebo at 12 months. FDA recommended pursuing traditional approval (not accelerated), supporting a robust regulatory path.

- U.S. launch anticipated: Late 2026/early 2027

- Market significance: Would be first approved therapy for any form of LGMD

- Leadership: Claudia Bujold (ex-Novartis, Skyclarys launch) joined as SVP Sales & Marketing

Encaleret for ADH1 (NDA 1H 2026)

CALIBRATE met all primary and key secondary efficacy endpoints. Pre-NDA meeting completed successfully.

- U.S. launch anticipated: Late 2026/early 2027

- Market development: >1,700 unique patients claimed under dedicated ICD-10 code (E20.810) in 24 months through Oct 2025

- Leadership: Jeron Evans (30+ years commercialization experience) joined as SVP Sales & Marketing

Infigratinib for Achondroplasia (NDA 2H 2026)

PROPEL 3 met its primary endpoint (p<0.0001) with +2.10 cm/year height velocity improvement vs placebo at Week 52. First statistically significant improvement in body proportionality against placebo in achondroplasia.

- U.S. launch anticipated: Early-to-mid 2027

- Differentiation: First oral therapy option for achondroplasia

- Leadership: Aaron McIlwain (ex-Ionis ATTR brand lead) joined as SVP Sales & Marketing

How Did the Stock React?

BBIO traded up modestly on earnings day (+0.6%), closing at $68.31. The muted reaction suggests the strong results were largely priced in following the string of positive Phase 3 readouts.

Stock Performance Context:

- 52-week range: $28.33 - $84.94

- Current price: $68.31 (Feb 24, 2026)

- 50-day moving average: $75.26

- Market cap: $13.2B

Analyst sentiment heading into earnings:

- 11 Buy ratings, 0 Sell ratings

- Median price target: $94 (+38% upside)

- Recent targets: HC Wainwright $100, Wells Fargo $98, Morgan Stanley $96

What Changed From Last Quarter?

Key operational changes:

- Hired 3 new SVP Sales & Marketing leaders to lead BBP-418, encaleret, and infigratinib launches

- Completed $632.5M convertible notes offering in January 2026 to extend runway

- Stock-based compensation: $34.9M in Q4 vs $36.4M in Q4 2024

What Did Management Guide?

BridgeBio did not provide explicit revenue guidance but signaled confidence through:

-

NDA submission timelines:

- BBP-418: 1H 2026

- Encaleret: 1H 2026

- Infigratinib: 2H 2026

-

Launch expectations:

- BBP-418: Late 2026/early 2027

- Encaleret: Late 2026/early 2027

- Infigratinib: Early-to-mid 2027

-

Pipeline advancement:

- RECLAIM-HP (encaleret in chronic hypoparathyroidism) Phase 3 to initiate 2H 2026

- CALIBRATE-PEDS initiated for pediatric ADH1

- Depleter (next-gen ATTR-CM) IND submission 2027

Forward analyst estimates:

*Values retrieved from S&P Global

Balance Sheet and Cash Position

Cash position remains solid at $587.5M as of Dec 31, 2025, bolstered by January 2026 convertible notes issuance.

Capital raises in past 12 months:

- $632.5M 2033 convertible notes (Jan 2026)

- $575M 2031 Notes (Feb 2025)

- $297M royalty agreement with HealthCare Royalty/Blue Owl (Jun 2025)

Management lowered interest expense and extended debt maturity through the convertible notes strategy.

What Are the Key Risks?

-

Execution risk on three simultaneous launches: BridgeBio plans to launch three new products (BBP-418, encaleret, infigratinib) in 2026-2027 while scaling Attruby. Commercial infrastructure must expand rapidly.

-

Competitive pressure in ATTR-CM: While Attruby leads on TTR stabilization, Pfizer's tafamidis franchise and emerging therapies create competitive dynamics.

-

Cash burn trajectory: Despite ~$588M cash and recent financing, the company burned $446M from operations in FY2025 . Multiple launches will require continued investment.

-

Regulatory risk: Three NDA submissions planned for 2026 create binary event risk across multiple programs.

Forward Catalysts

CEO perspective on 2026:

"As we close our first decade at BridgeBio, we're reflecting on just how far we've come – from a bold idea about a new type of biotech rooted in a hub-and-spoke model to a company with incredible commercial strength and multiple late-stage successes. In all, we hope this leads to 6 approved products as our first decade draws to a close." — Neil Kumar, Ph.D., CEO