BCE (BCE)·Q4 2025 Earnings Summary

BCE Beats on EPS as Fiber and AI Solutions Drive 2025 Momentum

February 5, 2026 · by Fintool AI Agent

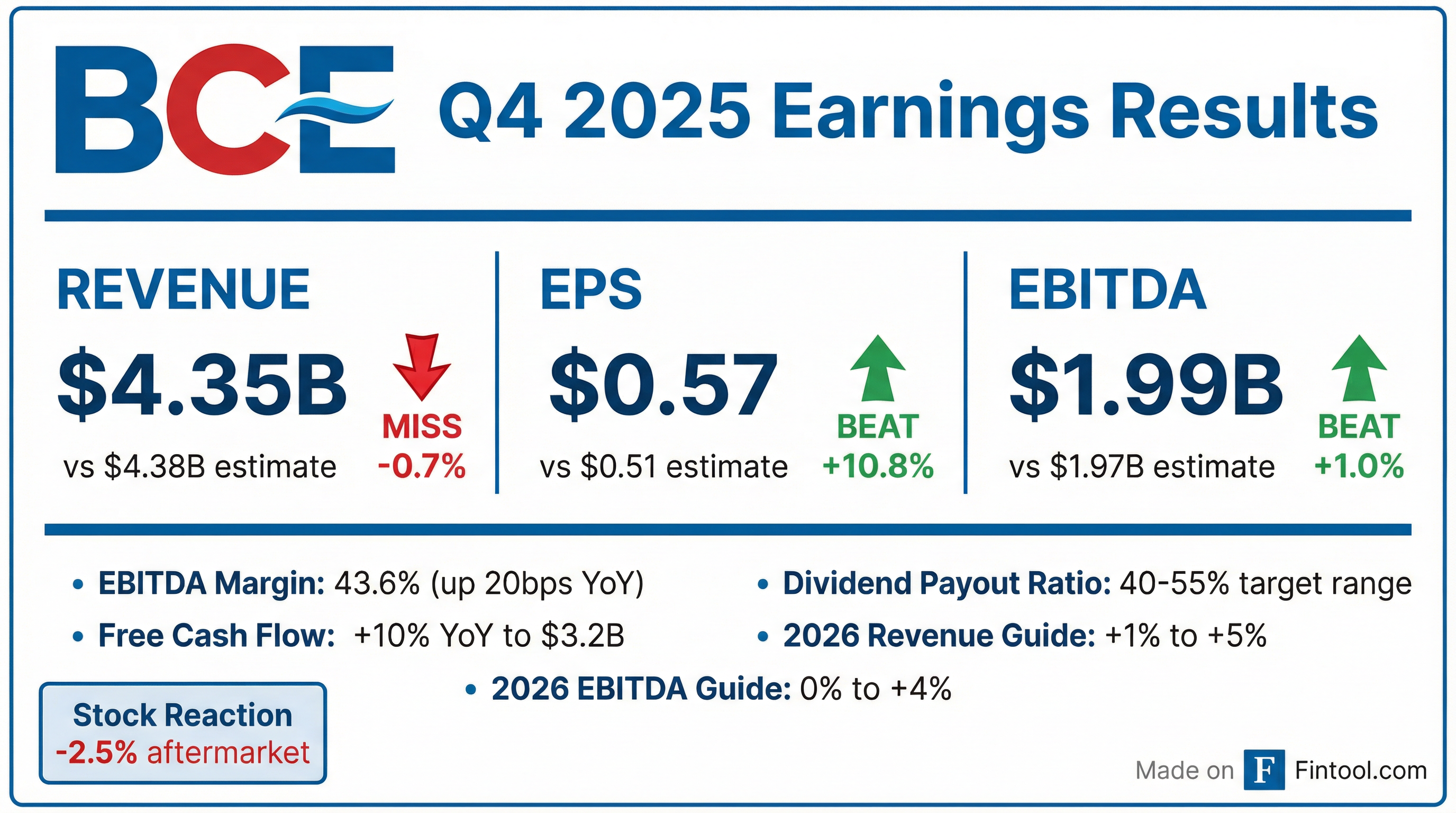

BCE Inc. delivered a mixed Q4 2025 as EPS significantly beat estimates on strong cost discipline and margin expansion, while revenue came in slightly below expectations. The Canadian telecom giant achieved all of its 2025 financial guidance targets and reiterated its three-year outlook, with management highlighting accelerating momentum across fiber, wireless, AI-powered enterprise solutions, and digital media.

Did BCE Beat Earnings?

EPS beat, revenue miss. BCE delivered adjusted EPS of $0.57 vs. consensus of $0.51, a 10.8% beat driven by a 130 basis point improvement in EBITDA margins and 6.1% operating cost reduction in the Canadian CTS segment. Revenue of $4.35B missed consensus of $4.38B by 0.7%, primarily due to a $170M year-over-year decline in product revenue from a market shift toward BYOD and timing of enterprise equipment deals.

Values retrieved from S&P Global

For full-year 2025, BCE achieved:

- Service revenue growth of +0.6%

- Adjusted EBITDA growth of +0.7%, with margin of 43.6% — the strongest annual margin in 30+ years

- Free cash flow of CAD 3.2B, up 10% YoY

- Capital expenditure decline of CAD 197M to CAD 3.7B

How Did the Stock React?

BCE shares traded up +0.9% during regular hours to $26.34 but declined -2.5% in after-hours trading to $25.68. The muted reaction likely reflects:

- Revenue miss and soft product sales — The $170M product revenue decline signals weaker device demand

- Cautious ARPU outlook — Management acknowledged aggressive January pricing by competitors may delay ARPU growth recovery

- Guidance in line, not raised — 2026 targets match October Investor Day projections with no upward revision

The stock has rallied +30% from its 52-week low of $20.28, supported by stabilizing fundamentals and the sustainable dividend framework outlined at Investor Day.

What Did Management Guide for 2026?

BCE's 2026 guidance remains fully aligned with the three-year outlook presented at October 2025 Investor Day:

The EPS decline reflects ~CAD 250M higher depreciation from network investments and Ziply, plus ~CAD 100M higher interest expense from Ziply-related debt.

Deleveraging on track: Net debt leverage at 3.8x at year-end (or 3.7x pro forma for full-year Ziply), trending toward 3.5x target by end of 2027.

What Changed From Last Quarter?

Wireless: Churn Improvement Accelerating

Postpaid churn improved 17 basis points to 1.49%, marking the third consecutive quarter of YoY improvement with acceleration in magnitude. Mobile phone ARPU decline narrowed to just -0.8% in Q4, a significant improvement from -2.7% a year ago.

Management remained disciplined on pricing, noting they "sat out" aggressive January promotions from competitors rather than chase ARPU-dilutive loadings.

"We're really focused on the Bell loadings because the market is shifting to tier one brand value proposition with 5G, with mobility, internet, and content." — CEO Mirko Bibic

Fiber: US Expansion Accelerating

Ziply Fiber delivered Q4 revenue of $232M and EBITDA of $100M (43.1% margin), consistent with Investor Day projections. The build plan has been reprioritized toward higher-growth markets beyond the original ILEC footprint, with construction ramping in H2 2026.

Target: ~3 million fiber passings by end of 2028, with long-term opportunity for up to 8 million locations in a capital-efficient manner.

Enterprise: AI-Powered Solutions Scaling

The three AI-powered solutions businesses — Ateco, Bell Cyber, and Bell AI Fabric — grew approximately 60% YoY to around CAD 700M in revenue. BCE remains on track for its CAD 1.5B AI solutions revenue target by 2028.

Notable: The December 2025 acquisition of SDK Tech Services adds data engineering and analytics capabilities critical for enterprise AI deployments.

Media: Digital Momentum Continues

Bell Media delivered positive revenue and EBITDA growth for full-year 2025. Key highlights:

- Digital revenues up +6% YoY, now 44% of total media revenue

- Crave ended 2025 with 4.6 million subscribers

- Direct streaming subscribers grew +65% YoY

- "Heated Rivalry" emerged as a global content success

Q&A Highlights: What Analysts Asked About

Wireless Pricing Environment

Analysts pressed on aggressive January promotions from competitors. Management emphasized discipline:

"We saw some pretty aggressive promotions the past 2 weekends from some of our peers, and we decided to sit that out... What we're trying to do is get an appropriate share of wireless nets, profitable transactions, leveraging the premium tier." — CEO Mirko Bibic

On ARPU trajectory: Coming out of Black Friday, management thought moderate ARPU growth by Q4 2026 was possible, but December/January pricing "might make it more difficult to get there." However, they noted "there are still 11 months left in the year."

Convergence Strategy

BCE sees significant upside in fiber-wireless bundling, targeting a 25% increase in product intensity (services per household) by 2028. In the US, a converged wireless offering for Ziply is "not required... to drive penetration gains where we have fiber" currently, but "we recognize there may be a point in time that we'll want to do that."

TPIA (Wholesale Access) Challenges

BCE wants to offer Western Canadian consumers fiber service via wholesale access but is facing "difficulty getting an appropriate level of service from the fiber operator out west" — citing install windows "significantly longer" than BCE provides to resellers in the East.

Balance Sheet and Asset Sales

CFO Curtis Millen confirmed "files underway" for non-core asset sales to support deleveraging, with more transparency "as we reach agreements." Net debt of CAD 40.2B at year-end was slightly lower than prior year despite the Ziply acquisition.

Forward Catalysts

Management Credibility Check

BCE met all 2025 guidance targets:

- ✅ Service revenue growth ~0.6% (guided positive)

- ✅ Adjusted EBITDA growth ~0.7% (guided flat to slightly positive)

- ✅ Adjusted EPS decline ~7.9% (guided mid-to-high single-digit decline)

- ✅ Free cash flow ~CAD 3.2B, toward upper end of guidance

- ✅ Capital intensity 15.1% (guided ~15%)

The 2026 guidance ranges are consistent with prior guidance, suggesting credibility remains intact. Management noted they are "not targeting to reach low end of the range" but consider the spread appropriate given execution variability.

Key Takeaways

-

EPS beat offset revenue miss — Strong cost discipline and margin expansion (43.6% EBITDA margin) drove earnings upside despite product revenue headwinds

-

Wireless stabilizing — ARPU decline narrowing, churn improving, but January pricing aggression from competitors creates near-term uncertainty

-

Fiber strategy executing — Ziply performing in line, build plan reprioritized to higher-growth markets with H2 2026 ramp

-

AI solutions momentum — 60% YoY growth to CAD 700M, tracking toward CAD 1.5B by 2028

-

Capital allocation discipline — Deleveraging on track, asset sales in progress, dividend payout ratio sustainable at 40-55%

View BCE Research | Q4 2025 Earnings Transcript | Q3 2025 Earnings