BECTON DICKINSON & (BDX)·Q1 2026 Earnings Summary

BD Beats Q1 Estimates as Waters Deal Closes, Unveils $4B Capital Return

February 9, 2026 · by Fintool AI Agent

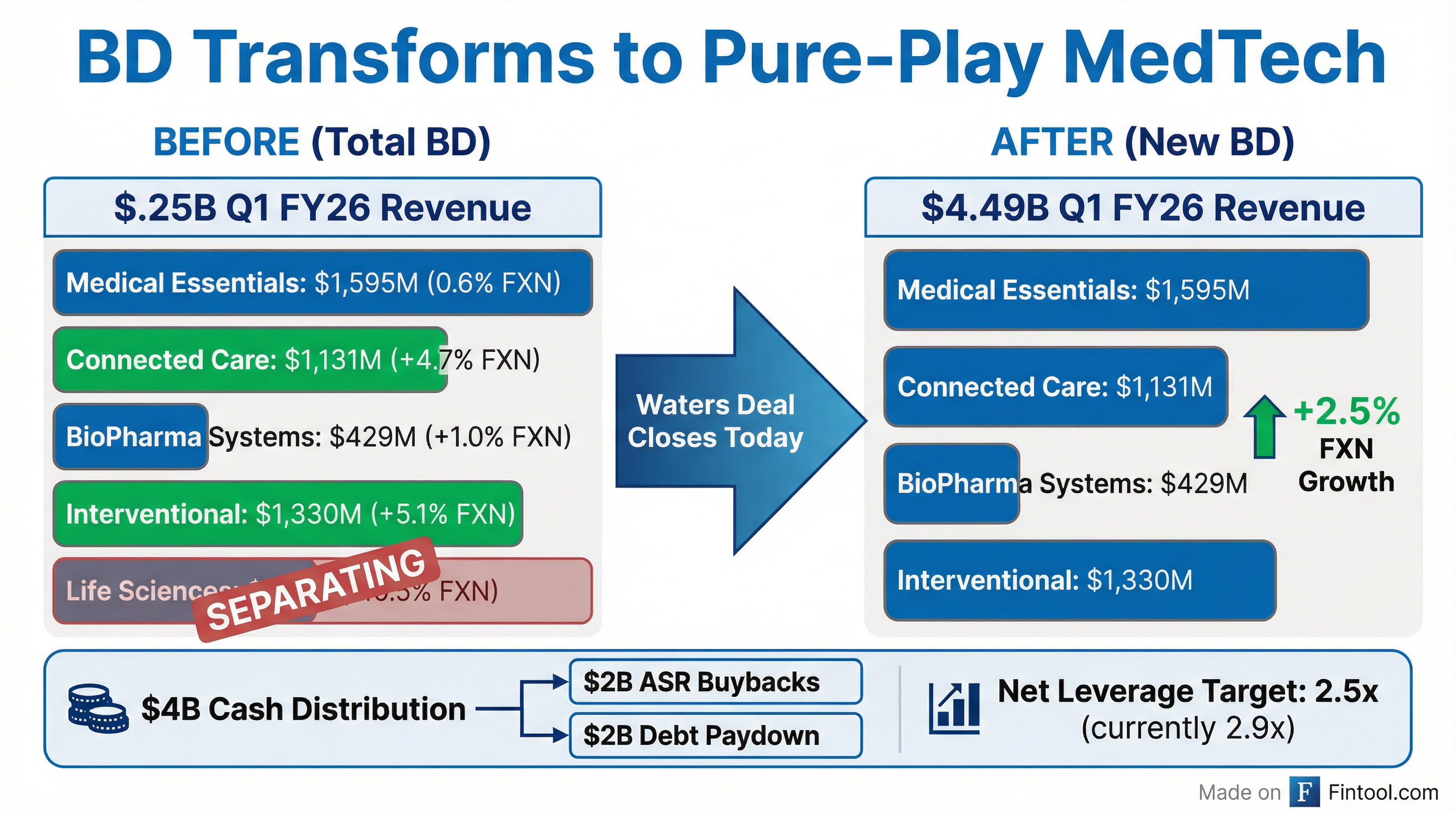

Becton Dickinson (NYSE: BDX) delivered a Q1 FY2026 beat on both revenue and earnings, reporting $5.3B in sales and adjusted EPS of $2.91—topping Street estimates by 2% and 3.6% respectively . The headline, however, is transformational: the Waters Corporation deal officially closed during the earnings call (nearly two months ahead of schedule), creating a pure-play MedTech company and unlocking $4B in capital—$2B for an accelerated share repurchase and $2B for debt paydown .

Did BD Beat Earnings?

Yes—both revenue and EPS exceeded expectations.

The beat came despite significant headwinds from the Life Sciences segment slated for separation. New BD (excluding Life Sciences) posted 2.5% FXN growth versus just 0.4% for total BD .

What Changed From Last Quarter?

The Q1 FY2026 results mark BD's first quarter operating under its new five-segment structure introduced October 1, 2025, positioning the company for the Waters separation .

Key changes versus Q4 FY2025:

*Values from prior quarter, retrieved from S&P Global

The year-over-year EPS decline of 15.2% reflects a higher effective tax rate (11.8% vs 6.9%) and increased SSG&A spend (+6.0%), partially offset by strong operational execution .

How Did Each Segment Perform?

Winners (New BD segments):

Loser (Separating):

The Urology and Critical Care unit within Interventional delivered standout +9.5% FXN growth, powered by continued adoption of the PureWick Male and Female External Catheter portfolios .

What Did Management Guide?

BD maintained its full-year FY2026 guidance for New BD (post-separation), with adjustments only for corporate overhead migrating to Waters, TSA income, and proceeds deployment .

Capital deployment from Waters proceeds ($4B):

- $2B → Accelerated Share Repurchase (ASR) program

- $2B → Debt paydown

- Net leverage currently 2.9x, targeting 2.5x

Management noted tariff commentary is based on policies in effect as of February 6, 2026, with uncertainty around escalation .

What's Driving Innovation?

BD highlighted several near-term product catalysts across its pipeline :

Launched Q1 FY26:

- Avitene Flowable (U.S.) – Enters ~$400M hemostatic market growing ~5%

- Surgiphor EU (Europe/UK) – Ready-to-use surgical irrigation solution

- Pyxis Pro – Off to a strong start with 85% of initial orders from competitive conversions

In Progress:

- HemoSphere Stream Module – Target Market Release on track for 1H FY26; expands addressable market ~10x to 300K monitors

- Surgiphor Pulse – 510(k) submitted Q1; can expand BD's surgical irrigation presence by ~40%

Pipeline products with $50M+ revenue potential:

- BD neXus Infusion Platform

- BD Libertas 5mL/10mL

- CentroVena One

- BD Scionix Sirolimus DCB

- Rotarex Small Vessel

How Did the Stock React?

Despite the beat, BDX shares traded down approximately 2.7% in after-hours to $204.26, from a pre-earnings close of $210.02. The muted reaction likely reflects:

- EPS down 15% YoY – Even with the beat, adjusted EPS of $2.91 was materially below prior year's $3.43

- Life Sciences drag – The separating segment's -10.5% FXN decline weighed on headline numbers

- Margin compression – Adjusted operating margin contracted 240 bps to 21.2%

52-Week Range: $162.29 - $235.34

YTD Performance: +8.2%

1-Year Performance: -6.9%

Geographic Performance

China remains a significant headwind, with revenue down 13.9% FXN driven by Volume-based Procurement (VoBP) pressures and market dynamics affecting both Medical Essentials and Life Sciences .

Q&A Highlights

On Alaris Competitive Momentum (Jason Bedford, Raymond James): BD's Alaris market share is "nearing 60%" with management noting record competitive wins in Q1: "We had a record in new competitive wins in the quarter. We gained about a full point of share just in the quarter" . A new Alaris platform remains in development with submission planned for late FY26 .

On GLP-1 Trajectory (Matt Taylor, Jefferies): Management reaffirmed the $1B GLP-1 revenue target by end of decade, noting they're "nearing that halfway point on that journey" with continued double-digit growth . Over 80 novel and biosimilar GLP-1s are now contracted in BD devices, with management noting "billions of dollars" in recent pharma investments in injectable capacity .

On FY27 Headwinds (Shagun Singh, RBC): Alaris expected to be a 200 bps headwind in FY27 (vs 100 bps in FY26) as remediation volumes normalize, though BD expects to be at "record share levels" competitively . China VBP will have hit ~80% of BD's portfolio by end of FY26 .

On Pricing Environment (Josh Jennings, TP Cowen): Pricing remains "stable...generally flat to slightly positive" with over 50 bps positive ex-China, offset by VBP dynamics. As VBP abates in FY27+, pricing should become a net positive .

On CFO Search (Rick Wise, Stifel): Search is "well underway" with focus on "continuity of execution and financial discipline". Vitor Roque continues as Interim CFO .

Key Management Quotes

"With the completion of our life sciences transaction, BD enters this next chapter as a far more focused, pure-play med tech company." — Tom Polen, CEO

"We have actions underway to improve this even further. BD Excellence continued to drive meaningful productivity improvements of 8% in the quarter." — Tom Polen, on manufacturing

"When we started the journey several years ago, we had a little over 90 manufacturing plants, and we're under 50 today." — Tom Polen, on network simplification

Key Risks to Monitor

- Separation execution – Waters deal closed during the earnings call; TSA/LSA arrangements and stranded costs require management

- China deterioration – 13.9% FXN decline could accelerate with VoBP and funding pressures

- Tariff uncertainty – Guidance based on Feb 6 tariff policies; escalation not contemplated

- Tax rate normalization – ETR expected 16-17% for full year vs. 11.8% in Q1

- Margin trajectory – Path from Q1's 21.2% to guided ~25% requires significant improvement

The Bottom Line

BD delivered a solid operational beat in Q1, with New BD's 2.5% FXN growth validating the strategic rationale behind the Waters separation. The $4B capital deployment toward buybacks and debt reduction should provide near-term EPS support, though investors appear cautious on the margin trajectory and China headwinds. With the Life Sciences albatross removed, BD enters FY2026 as a focused MedTech pure-play with improving growth prospects in high-value segments like Connected Care and Interventional.

Related Links: