Backblaze (BLZE)·Q4 2025 Earnings Summary

Backblaze Posts First Profitable Quarter, Stock Surges 10% After Hours

February 23, 2026 · by Fintool AI Agent

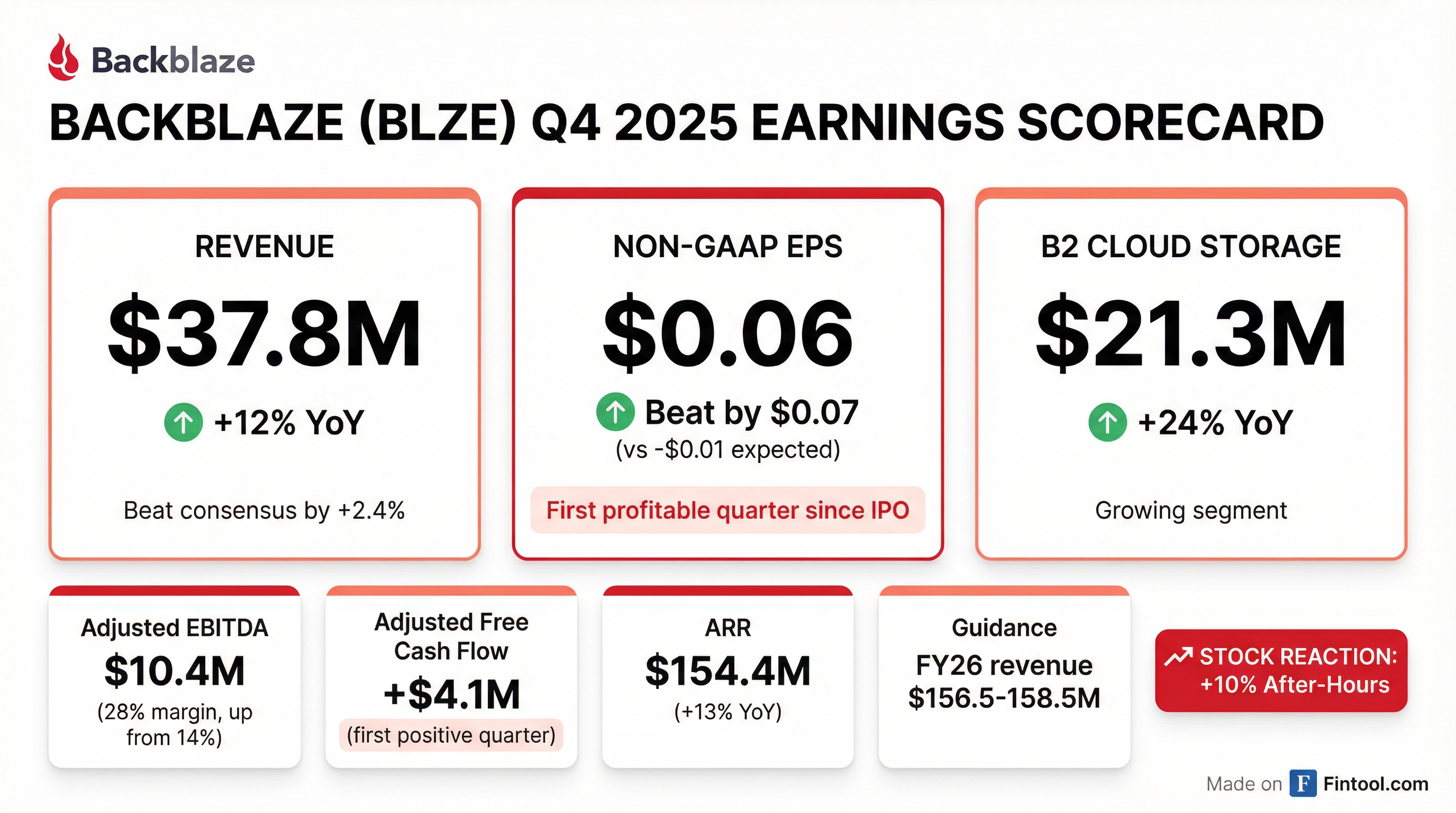

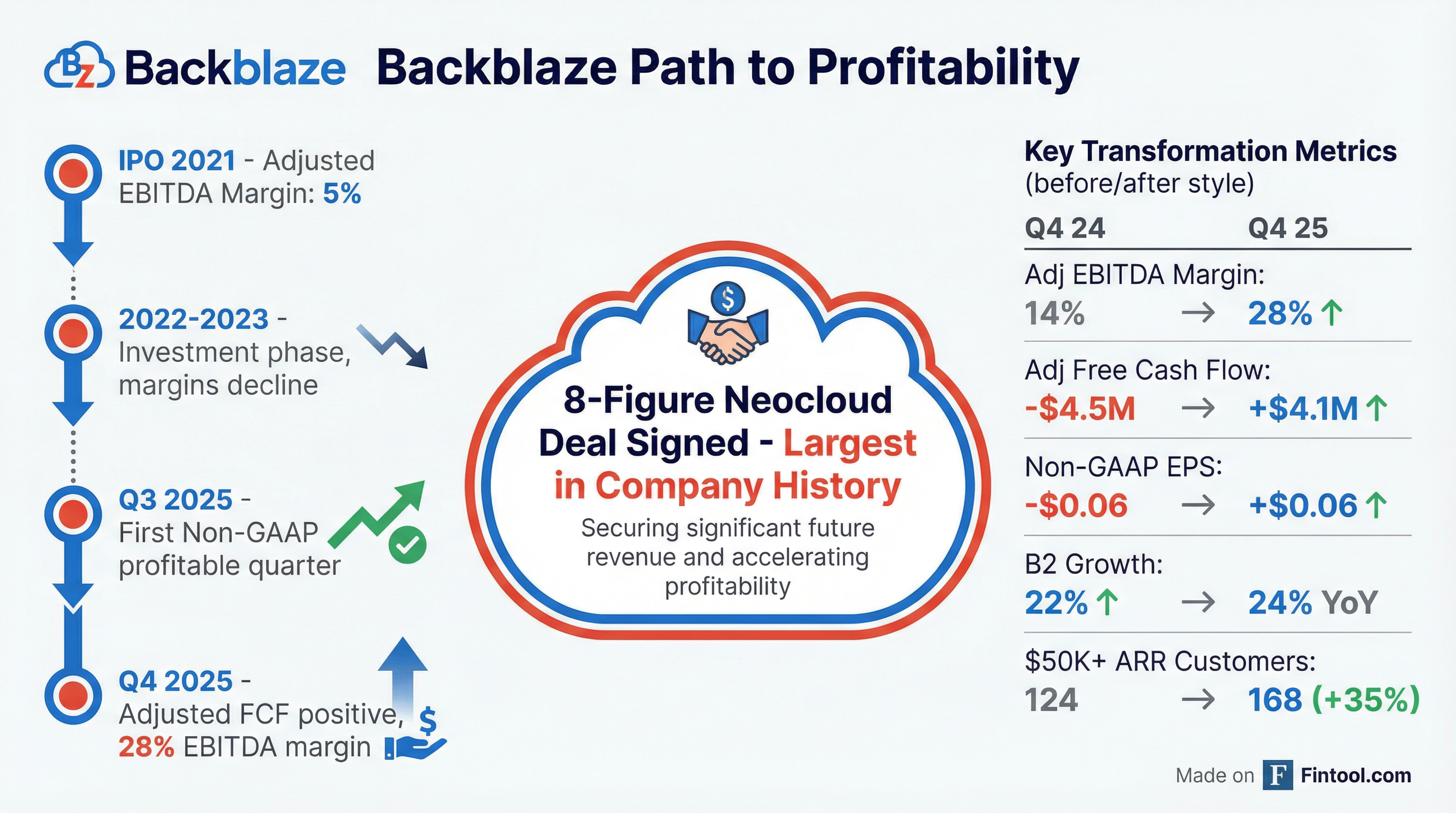

Backblaze (NASDAQ: BLZE) delivered a milestone quarter, posting its first Non-GAAP profit since going public while signing its largest contract in company history — an 8-figure neocloud deal worth over $15 million in total contract value. The stock surged 10% in after-hours trading to $4.82 following the results.

Did Backblaze Beat Earnings?

Yes — Backblaze beat on both revenue and EPS.

The EPS beat was particularly significant: analysts expected a loss of $0.01 per share, but Backblaze delivered $0.06 profit — its first profitable quarter since the November 2021 IPO.

Non-GAAP net income of $3.5 million compares to a $3.0 million loss in Q4 2024, representing a $6.5 million swing in profitability.

How Did the Stock React?

Backblaze shares closed the regular session at $4.37 (-0.7%) but jumped 10% in after-hours trading to $4.82 after the earnings release.

The stock has traded in a range of $3.83 to $10.86 over the past year, with significant volatility around earnings dates. This quarter's after-hours move is the largest positive reaction in recent memory, reflecting investor enthusiasm for the profitability milestone and neocloud deal.

What Changed From Last Quarter?

The Q4 2025 results show dramatic improvement across every key metric versus Q4 2024:

The company achieved positive adjusted free cash flow for the first time since IPO — a key inflection point management has been working toward.

What Was the Big Neocloud Deal?

The headline announcement was Backblaze's first 8-figure total contract value (TCV) neocloud agreement, worth more than $15 million over 3 years. CEO Gleb Budman called it "the largest agreement in company history."

Key Deal Details from the Q&A:

- Customer is a publicly traded neocloud with existing storage that wasn't meeting their needs

- Revenue timing: Don't expect meaningful revenue in 2026; in 2027, expected to contribute over 300 bps to B2 revenue growth

- Requires development work on both sides before full deployment

- Customer's internal leaders were already familiar with Backblaze from prior roles

"They did pretty detailed technical due diligence, and then chose us. The why came in part because we had established a lot of credibility over many years, that we are a great storage platform." — Gleb Budman, CEO

The $14B Neocloud Opportunity:

- ~200 neoclouds currently in the market

- Neocloud storage (HDD-based) estimated to be a $14 billion opportunity by 2030

- Backblaze launched B2 Neo today — a white-label storage offering specifically for neoclouds

- B2 Neo allows neoclouds to offer storage without massive capital costs or years of engineering

- In discussions with 6+ additional neoclouds at similar scale

- Existing 6 and 7-figure neocloud deals have upside potential to become 8-figure deals

"The hyperscalers are not key competitors here because they are competing with the NeoClouds as opposed to being vendors for them, the way that we are." — Gleb Budman, CEO

What Did Management Guide?

Q1 2026 Guidance:

- Revenue: $37.6M - $38.0M (midpoint implies ~2% sequential decline)

- Adjusted EBITDA Margin: 18% - 20%

Full Year 2026 Guidance:

- Revenue: $156.5M - $158.5M (~8% YoY growth)

- Adjusted EBITDA Margin: 19% - 21%

- Adjusted Free Cash Flow: Roughly neutral (with quarterly variability)

- B2 growth: ~20% for full year

Important Quarterly Cadence Note: Due to difficult comps from the large variable customer, B2 YoY growth in Q2 and Q3 will be in the 12-19% range (Q2 at low end, Q3 at high end), with the full year averaging to 20%.

De-risked Guidance Philosophy: Management excluded "swing deals" from guidance — larger, less predictable opportunities — to provide a more credible baseline. For high-variable usage customers, guidance reflects contractual minimums rather than potential upside.

Segment Performance

B2 Cloud Storage — The Growth Engine

B2 Cloud Storage now represents 56% of total revenue, up from 51% a year ago. The segment is benefiting from AI workloads, cyber resilience demand, and enterprise expansion.

Computer Backup — Stable Cash Cow

While customer count declined, ARPU expansion offset the losses, keeping revenue stable. This segment provides predictable cash flow while B2 drives growth.

2026 Outlook: Management expects Computer Backup revenue to decline 5% YoY in 2026, starting at -3% in Q1 and building throughout the year.

"We have programs in place to stabilize the business. We would like to get it to a place where it is flat and possibly even slowly growing... It's a little too early for us to have confidence in those programs." — Gleb Budman, CEO

AI Customer Momentum

Management highlighted explosive growth in AI-native customers using B2 for AI workflows:

"As we sign up more of these AI customers, we see the opportunity for NRR to go up over time as well, because they are generating data at a faster rate than your average customer." — Gleb Budman, CEO

Example: An AI audio generation company launched a year ago and already has multiple petabytes with Backblaze, signing a six-figure annual deal.

Go-to-Market Transformation Update

Backblaze is executing a multi-pronged GTM transformation to move upmarket:

Upmarket Traction:

- ARR from $50K+ customers: $26M (up 73% YoY from $15M)

- $50K+ customer count: 168 (up 35% YoY from 124)

- RPO increased to $66M (+60% YoY), driven by the large neocloud deal

Pipeline Acceleration:

- 2024 pipeline: $15M

- 2025 pipeline: ~$30M (doubled YoY)

- Target run rate: $60M (double again)

"With our industry-leading win rates, pipeline transfers into ARR quite efficiently." — Gleb Budman, CEO

Flamethrower Program Exceeding Expectations:

- Launched just days ago and already 12 startups accepted

- Includes startups from Andreessen Horowitz and Y Combinator

- Growing faster than comparable programs at other leading companies

Leadership Investments:

- Elias Mendoza joined as Strategic Transformation Leader (ex-Cirrus Capital, IBM, Morgan Stanley)

- Dan Spraggins (SVP Engineering) and Rhett Dillingham (SVP Product) — deep AI and cloud infrastructure experience

- Russ Artzt (co-founder CA Technologies) as advisor

- GTM Advisory Committee with operators from Okta, Snowflake, ZoomInfo, and Carta

Q&A Highlights: Key Analyst Questions

Why will the 8-figure deal take a year to generate revenue?

"It's a combination of work we need to do and work they need to do. They have an existing storage offering that they're going to be switching to use B2 Neo instead... All the work that we're doing for them is useful for other NeoCloud providers and also other companies, but not required for most." — Gleb Budman, CEO

What's the NRR outlook for 2026?

CFO Marc Suidan: Due to the large variable customer comp from 2025, NRR could dip to ~100% for 1-2 quarters (Q2/Q3). For the full year at 20% B2 growth, NRR should finish closer to 110%, plus or minus 300 bps.

Are there gross margin headwinds?

Data center costs and equipment have increased, combined with accelerated CapEx for large customer deployments. This will reduce gross margin by a few hundred basis points in 2026. Backblaze is launching a gross margin optimization initiative focused on pricing, packaging, and infrastructure.

How does B2 Neo differ from B2 Overdrive?

- B2 Overdrive: Designed for end customers to use directly — high-throughput storage to send data to neoclouds or hyperscalers

- B2 Neo: White-label offering for neoclouds to integrate into their own platforms and offer to their customers

"They're largely serving different sides of the market, but both serving the needs of AI and HPC-type use cases."

What's the CapEx outlook?

PP&E expected to reach high 20s% of revenue by end of 2026. CapEx is financed through capital leases with principal payments at ~mid-teens % of revenue.

What Should Investors Watch?

Bulls Will Focus On:

- First profitable quarter demonstrates operating leverage

- 8-figure neocloud deal validates enterprise/AI positioning

- Adjusted FCF positive for first time since IPO

- $50K+ ARR customers growing 73% YoY

- B2 growth accelerating (24% vs 22% prior year quarter)

Bears Will Note:

- NRR declining (111% vs 123% YoY) — expansion slowing

- Total company growth decelerating (12% vs 14% prior quarter)

- FY26 guidance implies further deceleration (~8% growth)

- Computer Backup customer count declining

- Stock still down ~55% from 52-week high

Key Quotes From the Call

"We finished 2025 with solid fourth quarter results. Revenue came in line with guidance and adjusted EBITDA margin reached 28%, doubling over the prior year. We also delivered Adjusted Free Cash Flow profitability for the first time as a public company." — Gleb Budman, CEO

"AI is reshaping how data is created and scaled, and storage sits at the center of that transformation. Across neocloud platforms and AI-native developers, we are building the foundation for the next generation of data infrastructure." — Gleb Budman, CEO

"This progress was not driven by short-term cost actions, but by the inherent leverage in our operating model as revenue scales." — Marc Suidan, CFO

"Based on our current operating plan, we expect to fund our growth through operating cash flows and capital leases. We do not anticipate a need to raise additional capital." — Marc Suidan, CFO

The Bottom Line

Backblaze delivered a transformational quarter: its first profit since IPO, its largest deal ever, and a clear path to sustainable profitability. The 10% after-hours move reflects investor relief that the long-awaited inflection has arrived.

The key question for 2026: Can the neocloud strategy and GTM transformation accelerate growth, or will NRR compression and Computer Backup erosion cap upside? At ~$250M market cap, the stock prices in skepticism — but Q4 suggests the business model is working.

Data sourced from Backblaze 8-K filed February 23, 2026, Q4 2025 earnings call transcript, and S&P Global.