COLUMBUS MCKINNON (CMCO)·Q3 2026 Earnings Summary

Columbus McKinnon Beats Estimates on 10% Sales Surge as Kito Crosby Deal Closes

February 9, 2026 · by Fintool AI Agent

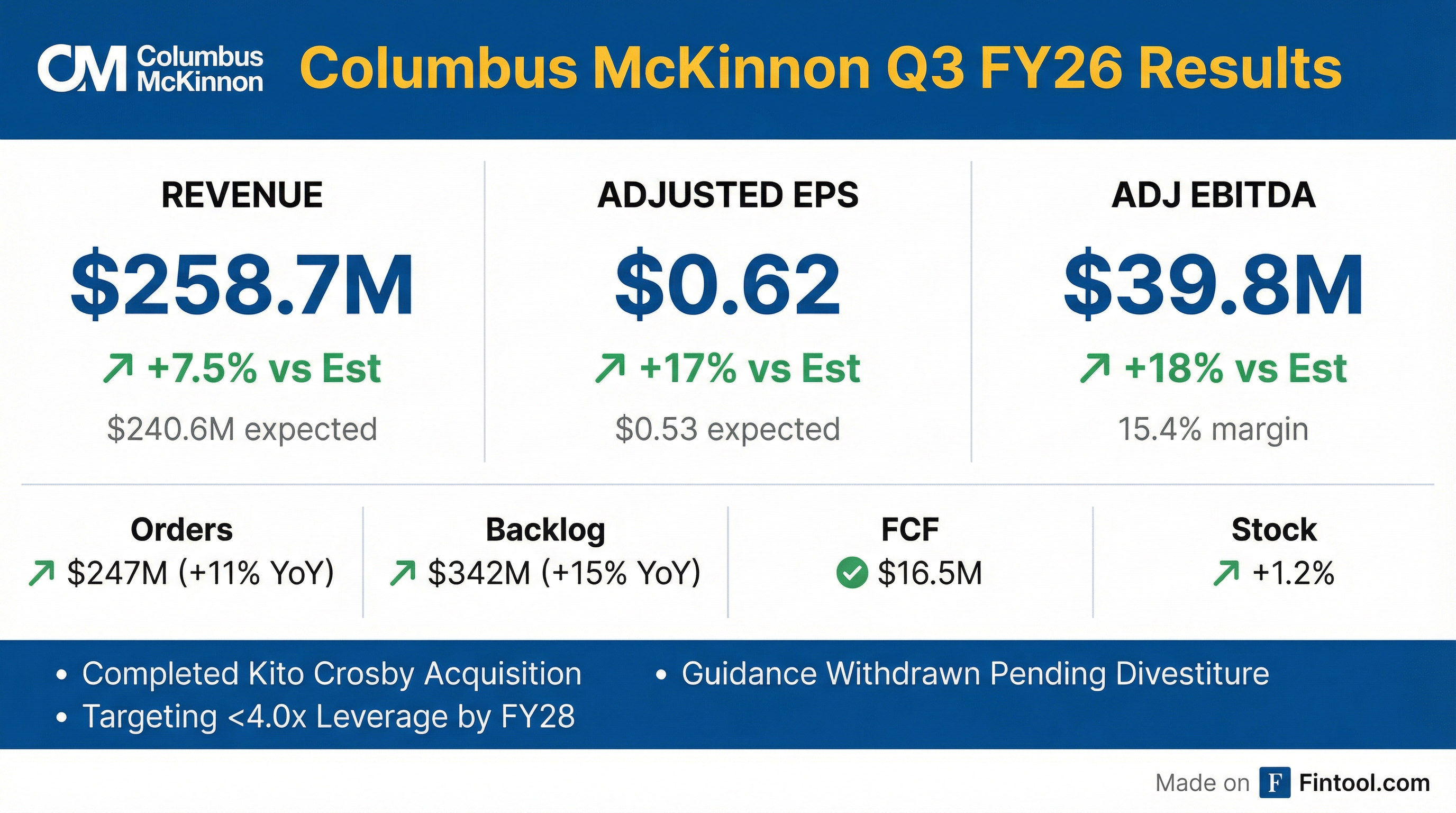

Columbus McKinnon (NASDAQ: CMCO) delivered a strong third quarter fiscal 2026, beating revenue estimates by 7.5% and adjusted EPS by 17.2%. The intelligent motion solutions provider reported net sales of $258.7 million, up 10% year-over-year, with double-digit order growth and backlog expansion across all regions.

The quarter was bookended by the completion of the transformative Kito Crosby acquisition on February 4, 2026, setting the stage for significant value creation opportunities.

Did Columbus McKinnon Beat Earnings?

Yes — both revenue and EPS exceeded expectations.

Revenue beat was driven by 10% year-over-year growth with strength across lifting, linear motion, and automation globally. The company delivered $11.7 million in higher volume, $6.1 million from pricing, and $6.7 million from favorable currency translation.

This marks the third consecutive quarter of beating estimates, following Q1 and Q2 FY26 beats.

How Did Orders and Backlog Perform?

Orders surged 11% year-over-year to $247.4 million with growth across both short-cycle and project-related orders.

CEO David Wilson noted strength in U.S. precision conveyance, lifting and automation, with a robust global funnel of opportunities. However, management flagged continued macroeconomic softness in EMEA where order conversion rates have remained slow.

What Happened to Margins?

Margin compression despite revenue growth — a key watch item for investors.

The margin decline was driven by:

- Negative tariff-related impacts

- Acquisition deal and integration costs of $6.3 million

- Prior year benefited from incentive compensation accrual release

This was partially offset by lower Monterrey factory start-up costs ($1.5M vs $3.0M prior year) and reduced factory consolidation expenses.

Tariff Outlook: Management noted they are slightly ahead of their ~$10M net tariff impact target through Q3 FY26. They expect to achieve tariff cost neutrality by year-end and margin neutrality in FY27 as mitigation actions take hold.

What Did Management Guide?

Standalone guidance withdrawn — but pro forma combined company metrics provided.

Key reasons for pulling standalone guidance:

- Uncertainty around timing of the pending U.S. power chain hoist and chain operations divestiture

- Regulatory limitations on information sharing with Kito Crosby prior to closing

- Integration of financial processes within Kito Crosby

Pro Forma Combined Business (from January 14 press release):

Note: Pro forma assumes full-year ownership of Kito Crosby and divestiture of chain/hoist operations at year start.

Q4 FY26 Warning: Certain transaction-related expenses, purchase accounting adjustments, and early integration costs will be incurred in Q4, and these plus higher interest expense are expected to be dilutive to GAAP EPS.

FY27 Guidance: Will be provided in conjunction with the Q4 FY26 earnings release in late May 2026.

Leverage Target: Management expects significant cash flow generation from the combined business, targeting Net Leverage Ratio below 4.0x by end of fiscal 2028.

How Was the Acquisition Financed?

Columbus McKinnon completed permanent financing at rates below initial estimates of ~8%:

Key financing advantages:

- Rates below initial ~8% estimate accelerates deleveraging

- Term Loan B is prepayable without penalty — significant flexibility for early debt paydown

- Divestiture proceeds (~$160M net of taxes and fees) will go directly to Term Loan B paydown

Primary capital allocation priority: Debt repayment, with substantial FCF expected to reduce net leverage below 4x by fiscal 2028.

What Changed From Last Quarter?

Several notable shifts from Q2 FY26:

Positive shifts:

- U.S. demand stabilization continuing

- Double-digit growth across both U.S. (+14%) and non-U.S. (+7%)

- Free cash flow nearly tripled Q/Q to $16.5M

Concerns:

- EMEA macroeconomic softness persists

- Margin compression across all metrics

How Did Cash Flow Perform?

Free cash flow generation was a bright spot:

YTD operating cash flow of $20.6 million increased 106% year-over-year, as strong cash generation more than offset acquisition-related cash outflows of $13.3 million.

Capital allocation priorities post-acquisition:

- Debt reduction — Primary focus on debt repayment

- Growth investments — Customer experience and operational performance

- Dividend maintenance — Maintain current dividend ($0.07/share quarterly)

- Future M&A — Over the long-term after de-levering

How Did the Stock React?

The earnings release came after market close. During regular trading on February 9, CMCO closed at $22.90, up 0.6% on the day.

The stock has rallied significantly from its 52-week low of $11.78, now trading 94% above that level. The Kito Crosby acquisition closing on February 4 likely contributed to recent strength, with shares up ~8% in the days leading into earnings.

What Should Investors Watch?

CEO's Investment Thesis Summary (Closing Remarks):

- Doubling revenue base to become a scaled global provider of intelligent motion solutions

- Complementary geographic positions: strong in North America, room to grow together in EMEA, APAC, and Latin America

- Combined product portfolio enables "one-stop" customer experience

- Combined scale benefits across material spend, Columbus McKinnon Business System (80/20), and Kito's lean manufacturing expertise

- Substantial FCF generation expected to delever balance sheet to <4x by FY28

Near-term catalysts:

- Q4 FY26 results and FY27 guidance (late May 2026)

- Kito Crosby integration progress and synergy realization

- Completion of U.S. power chain hoist divestiture (~$160M net proceeds)

- EMEA demand recovery timing

Key risks:

- Integration execution risk with Kito Crosby

- Elevated leverage post-acquisition

- Continued EMEA softness

- Q4 GAAP EPS dilution from transaction costs

- Tariff-related margin headwinds

Management credibility check:

- Delivered on Q3 despite conservative tone last quarter

- Beat estimates three consecutive quarters

- On track with Monterrey factory cost reduction

- Acquisition closing on schedule

Q&A Highlights

On Kito Crosby Performance vs. Deal Announcement:

Management provided updated Kito Crosby results showing the business outperformed original deal assumptions:

On Synergy Timing:

- Year 1: 20% of $70M = ~$14M

- Year 2: 60% cumulative = ~$42M

- Year 3: 100% = $70M run rate

Management noted synergies will naturally be back-end loaded within each year, and the integration team is working to potentially over-deliver.

On Margin Compression Drivers: CFO ranked the drivers: mix was the biggest impact, followed by tariffs. Specific mix headwinds included:

- More unit sales in lifting equipment vs. parts (bigger installed base, but lower margin)

- Lower Precision Conveyance shipments due to timing (orders up considerably, significant PowerCo/Montratec backlog remains)

- More rail project shipments, fewer Linear Motion sales

On End Market Strength:

- Strong: General industrial, automation, e-commerce, construction, aerospace & government, heavy machinery, food & beverage

- Slower: Stocking distributors (year-end inventory management), energy & utilities (project timing — expected to improve)

On Short Cycle Outlook: Orders up slightly YTD through January vs. prior year. Management sees short-cycle demand remaining robust, notably in the U.S., and expects it to continue into at least H1 calendar 2026.

On Chain Hoist Divestiture Impact: No material or outsized orders in the to-be-divested chain hoist business that would artificially inflate Q3 numbers.

Key Quotes from Management

"Our team delivered double-digit sales, order and EPS growth in the quarter, ahead of our expectations as we executed on commercial initiatives and continued to benefit from U.S. demand stabilization." — David J. Wilson, President and CEO

"While I am encouraged by our active, global funnel of opportunities, we remain cautious on the macroeconomic environment in EMEA where order conversion rates have remained slow." — David J. Wilson, President and CEO

"I have never been more excited about the opportunities that lie ahead for Columbus McKinnon. In combination with Kito Crosby, we will provide the market with a superior customer value proposition." — David J. Wilson, President and CEO

"We're working our tails off to deliver on [synergies] and to hopefully over-deliver. Our commitment is to get to the 20% in a year... we have a full and robust list of opportunities." — David J. Wilson, President and CEO

"We expect U.S. demand to remain healthy, driven by lower interest rates, favorable CapEx deduction rules as part of the new tax legislation, and benefits from onshoring." — David J. Wilson, President and CEO

Columbus McKinnon is a leading worldwide designer, manufacturer, and marketer of intelligent motion solutions for material handling, including hoists, crane components, precision conveyor systems, rigging tools, and digital power and motion control systems.

Related Links: