PC CONNECTION (CNXN)·Q4 2025 Earnings Summary

PC Connection Posts Record Gross Profit, Boosts Buyback by $50M

February 4, 2026 · by Fintool AI Agent

PC Connection (NASDAQ: CNXN), the IT solutions provider serving business, government, healthcare, and education markets, reported Q4 2025 results that showcased margin strength despite modest revenue contraction. The company delivered record gross profit in both its Enterprise and Business Solutions segments, expanded gross margin by 100 basis points to 19.3%, and rewarded shareholders with a $50M buyback increase.

Shares rose 2.3% to $60.15 following the announcement.

Did PC Connection Beat Earnings?

PC Connection has limited analyst coverage, making traditional beat/miss comparisons difficult. However, the company's adjusted EPS growth of 17% on flat net income reflects improved share count from aggressive buybacks (repurchased 179,235 shares at $10.7M in Q4).

New Metric: Gross Billings — Beginning this quarter, management is disclosing gross billings (total value billed before certain adjustments). Gross billings increased 2.9% to $1.06B vs. $1.03B prior year, demonstrating underlying demand growth despite net sales headwinds.

What Changed From Last Quarter?

The Positive Shift:

- Gross margin hit 19.3%, the highest in recent quarters, driven by software sales surging 24% YoY

- Enterprise Solutions reversed course with 11.9% revenue growth vs. prior quarters of softness

- Business Solutions achieved record gross profit with margin expanding 160 bps to 25.5%

- Management initiated cost reduction actions resulting in $3.1M of severance expenses

The Challenges:

- Public Sector revenue collapsed 36.8% YoY, though margin jumped 400 bps to a record 19.4%

- Server/storage sales declined 14% as enterprises delay hardware refreshes

- Interest income fell to $3.6M from $4.8M as cash balances declined

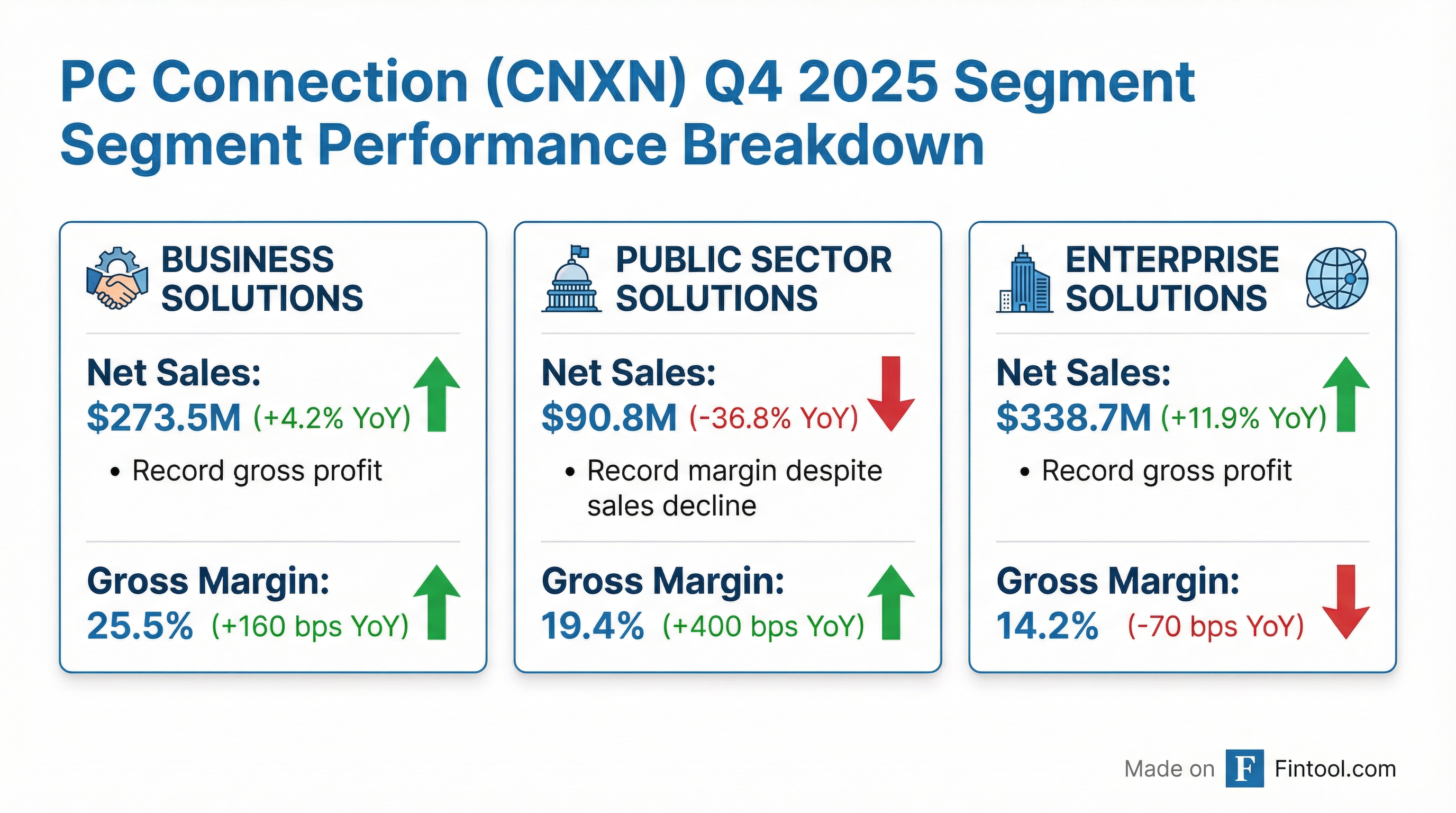

How Did Each Segment Perform?

Enterprise Solutions — The Growth Engine

Net sales surged 11.9% to $338.7M, with gross billings up 16.1% to $457.8M. The segment achieved record gross profit despite a 70 bps margin contraction to 14.2%, suggesting volume is outpacing pricing power. Enterprise now represents 48% of total revenue, up from 43% a year ago.

Business Solutions — Margin Champion

The SMB-focused segment delivered $273.5M in sales (+4.2% YoY) with record gross profit and a 25.5% gross margin — 160 bps higher than last year. This segment remains the company's most profitable per dollar of revenue.

Public Sector — Revenue Challenged, Margin Strong

Revenue plunged 36.8% to $90.8M, but management achieved a record 19.4% gross margin (+400 bps YoY). The dramatic volume decline was primarily due to a non-repeating project that straddled Q4 2024 and Q1 2025, plus delays in K-12 project rollouts. Management expects conditions to improve later in 2026.

How Did Key Verticals Perform?

The vertical performance underscores the strength in Enterprise Solutions, where customers are investing heavily in modernization and AI-driven technologies.

What Did Management Say?

"In the fourth quarter, Connection delivered record gross profit in both our Enterprise and Business Solutions segments, reflecting strong execution as our customers modernize for an AI-first IT environment. I believe we have the right team and strategy to continue to drive profitable growth and enhance long-term shareholder value."

— Timothy McGrath, President and CEO

The "AI-first IT environment" framing is notable — software sales jumped 24% YoY and now represent 12% of net sales (up from 9%). This mix shift toward higher-margin software and services appears intentional.

Q&A Highlights

On 2026 Growth Expectations: Management expects to outperform the U.S. IT market by 200 basis points, with the blended market growing around 4%. Key demand drivers include AI at the edge (61% of endpoints are now AI-enabled) and expanding edge projects.

On Backlog Strength:

"As we move into 2026, our backlog remains strong. In fact, it ended Q4 at its highest level since 2022." — Tim McGrath, CEO

On Q1 2026 Outlook: CFO Tom Baker provided color on Q1: "It's gonna look a little like this quarter — flattish on revenue, probably low to mid-single digits increase in gross profit, and sub 3% on SG&A." The public sector headwind will be ~$40M in Q1 (vs. ~$30M in Q4), but management expects that headwind to clear by Q2-Q3.

On Cost Savings: Additional targeted headcount reductions were completed at the end of January. Total restructuring charges expected at $5.9M-$6.2M, with $7M-$8M in ongoing annual cost savings. Management targets operating margins of 3.7-3.9% by year end.

On Memory Constraints: Management flagged memory supply constraints as a 2026 dynamic, noting some customers pulled orders forward in Q4 while others may delay. This contributed to above-average inventory levels as Connection procured ahead of anticipated price increases.

On December Budget Flush: December revenue hit 38% of the quarter (vs. typical 35%), driven by customers consuming year-end budgets and getting ahead of price increases.

Capital Allocation Update

The 33% dividend increase signals management confidence. Full-year 2025 saw over 1.2 million shares repurchased at an average price of $62.64. With shares trading below that average, the buyback expansion suggests management views the stock as undervalued.

Full Year 2025 Summary

The full year tells a story of margin expansion and cash generation despite headwinds. GAAP net income declined slightly, but adjusted metrics improved as the company absorbed $6.0M in severance costs from restructuring activities.

How Did the Stock React?

Shares opened at $59.71 and traded up to an intraday high of $61.95 before settling at $60.15, up 2.3% on above-average volume.

Why the positive reaction?

- Margin strength — 19.3% gross margin beat recent quarters despite revenue softness

- Buyback boost — $50M authorization increase signals confidence

- AI positioning — CEO's "AI-first" commentary and software growth suggest secular tailwinds

- Valuation cushion — At 17.7x trailing P/E, expectations were modest

The stock trades at $60.15 with a market cap of $1.52B, below its 200-day moving average of $62.26.

Risks and Concerns

Public Sector Volatility: The 36.8% revenue decline in Public Sector is dramatic. While margin improvement suggests disciplined execution, the segment's unpredictable government contract timing creates earnings volatility.

Hardware Refresh Delays: Server/storage sales declined 14%, and notebooks/mobility fell 4%. If enterprises continue postponing hardware refreshes in favor of cloud/SaaS, Connection's traditional distribution model faces headwinds.

Interest Income Decline: As the company deploys cash for buybacks, interest income fell 24% YoY to $3.6M. This creates a headwind to net income even as operating performance improves.

Restructuring Costs: The $3.1M in Q4 severance suggests cost pressures. Management is actively right-sizing the organization.

Forward Catalysts

- Q1 2026 earnings — Management guides flattish revenue with low-to-mid single digit GP growth

- Backlog at 3-year high — Ended Q4 at highest level since 2022

- Public Sector recovery — ~$40M headwind clears by mid-year

- Operating margin expansion — Target 3.7-3.9% by year end vs. 3.4% in Q4

- AI/Edge demand — 61% of endpoints now AI-enabled

- Continued buyback execution with $83.6M available

Data sources: PC Connection 8-K and Q4 2025 Earnings Call Transcript, filed February 4, 2026. Stock data from market feeds. This analysis was generated by Fintool AI Agent.