COTY (COTY)·Q2 2026 Earnings Summary

Coty Stock Crashes 18% as Company Withdraws Guidance, Warns of Weak Q3

February 6, 2026 · by Fintool AI Agent

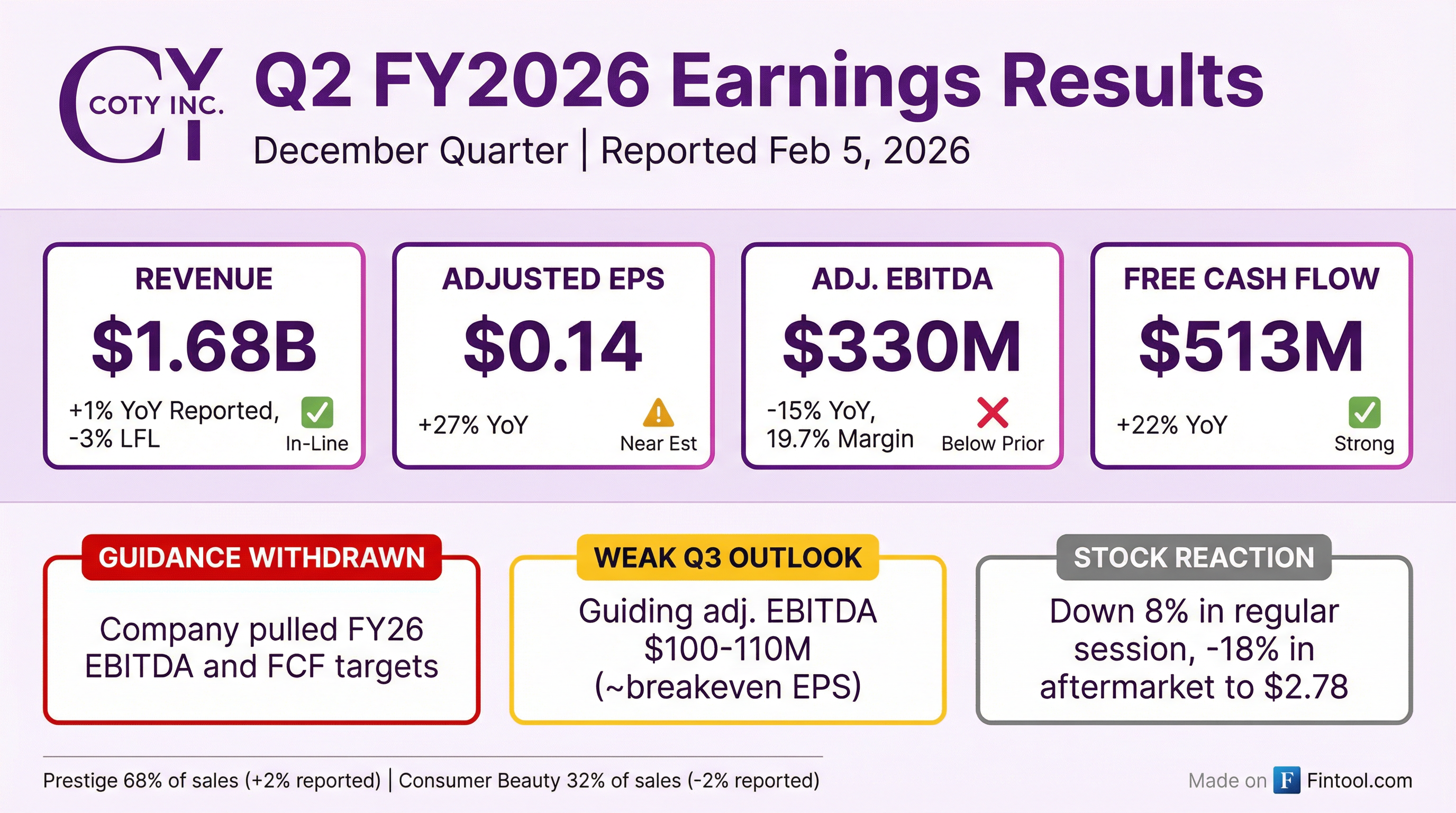

Coty Inc. (NYSE: COTY) delivered Q2 FY2026 results broadly in-line with expectations, but the stock collapsed 18% after the company withdrew its full-year guidance and warned of a significantly weaker Q3. New interim CEO Markus Strobel announced a strategic review called "Coty. Curated." while signaling major changes ahead for the struggling Consumer Beauty segment.

Did Coty Beat Earnings?

Q2 FY2026 results were mixed. Revenue of $1.68B came in essentially flat versus consensus, while adjusted EPS of $0.14 beat the prior year's $0.11 but remained under pressure from declining margins. The real story is the dramatic deterioration in profitability:

The EPS improvement was driven largely by a lower tax rate (16.8% vs 28.1%) and reduced interest expense, not operational improvement.

What Did Management Guide?

This is where the quarter took a dark turn. Coty withdrew its full-year FY26 guidance for EBITDA and free cash flow, citing the "complex beauty market backdrop and Coty's leadership transition."

For Q3, the outlook is grim:

For context, Q3 FY25 adjusted EBITDA was ~$200M. Guiding to $100-110M represents a 45-50% decline — a stunning deceleration that caught the market off guard.

Management attributed the EBITDA decline to four factors (roughly one-third each):

- Lower sales at constant currency — driving ~1/3 of decline

- 200-300 bps gross margin compression — promotional environment, mix, tariffs, FX on COGS

- Fixed cost headwinds — prior year variable compensation accrual reversals

- Deliberate A&CP protection — maintaining marketing behind key brands despite declining sales

Additional headwinds: ~$30M cash taxes related to Wella sale

How Did the Stock React?

COTY shares were punished severely:

- Regular session: Down 6.25% to $3.15

- After-hours: Crashed to $2.78, down 18% from pre-earnings close

- 52-week range: $7.10 high to $2.94 low — stock is now near the bottom

The magnitude of the decline reflects not just the weak Q3 outlook, but loss of visibility into the full year. When management pulls guidance during a CEO transition, investors assume the worst.

What Changed From Last Quarter?

Several significant developments:

1. New Leadership

Markus Strobel joined as Executive Chairman and Interim CEO effective January 1, 2026. He spent 33 years at P&G, most recently as President of Global Skin & Personal Care (SK-II, Olay, Old Spice, Native). Notably, in his early career, he was responsible for transforming Hugo Boss from a small local fragrance brand into a global success — and now Hugo Boss is Coty's largest brand.

His candid assessment: "The stock has also been hovering around $3 for several months, which I see as a signal that investors are skeptical about Coty's long-term ability to compete in beauty, sustain fair market share, and deliver consistent, profitable growth."

2. Wella Divestiture Complete

Coty sold its remaining 25.8% stake in Wella to KKR for $750M upfront cash (with potential for more later). The proceeds were used to pay down debt, bringing leverage to a 9-year low of 2.7x.

3. "Coty. Curated." Strategic Framework

The scale of complexity became clear: Coty sells 40+ brands across dozens of markets, creating 1,000+ possible brand/market combinations. The new strategic framework aims to break this cycle:

- "Making big even bigger, scaling what wins, stopping what dilutes, and removing layers that slow execution"

- Fewer assets, better execution, bigger propositions

- Ensure core brands get consistent, concentrated marketing support

- Shift spending from asset creation to working media and consumer engagement

Portfolio Decisions Announced:

- Ending the Aveda skincare license

- Reviewing "tail fragrance initiatives" — smaller, geographically dispersed activities

- Discontinuing small lifestyle fragrance initiatives and halting new projects in development

4. Consumer Beauty Strategic Review

The company is continuing its review of Consumer Beauty, with potential for divestitures or portfolio changes.

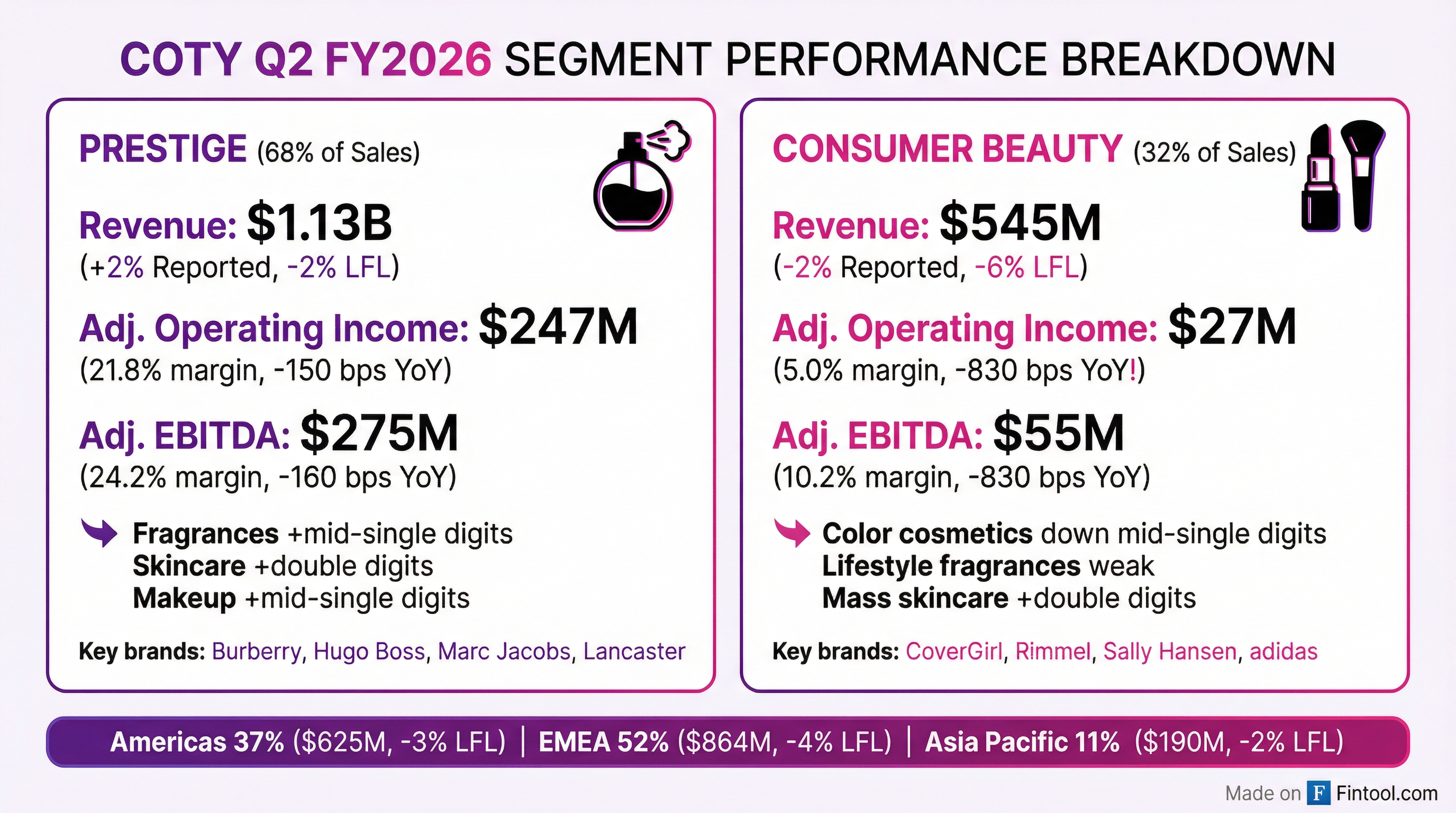

Segment Performance Deep Dive

Prestige (68% of Sales)

Prestige held up relatively well but still declined 2% on a like-for-like basis:

Bright spots:

- BOSS Bottled Beyond — Ranked #2 innovation in key markets; captured 90 basis points of U.S. market share for the Hugo Boss brand

- Burberry — Grown 140% since FY19; global fragrance ranking improved from #30 (2019) to #15 (2025); female fragrances now top 10, up from #27

- Kylie Cosmetics — Total sellout growth >20% in Q2; fragrance sales more than doubled YoY; ranked #2 among all beauty brands in 2025 for social media engagement

- Marc Jacobs — Daisy Murakami limited edition "exceeded all expectations and rapidly sold out"; Amazon launch drove double-digit sellout growth across all channels

- Prestige skincare up double-digits driven by Lancaster and philosophy

Challenges:

- Retailer destocking impact "significantly reduced" but service issues emerged from inventory complexity

- U.S. prestige fragrance market slowed from 7% growth in Q1 to ~3% in Q2

- Promotional environment "intensified through the holiday period" with aggressive discounting

- Sellout flattish in Q2, underperforming the market by several points in U.S. fragrance

What's Working in the U.S.:

- Ulta is now one of Coty's largest retail partners with strong partnership performance

- E-commerce up strong double-digits in H1

- Amazon fragrance sales up 30%+ following Marc Jacobs launch

- TikTok Shop driving halo effects for brands in both e-commerce and brick-and-mortar

Consumer Beauty (32% of Sales)

Consumer Beauty is in serious trouble:

An 830 basis point margin collapse is a red flag. The company is implementing the "Color the Future" performance improvement plan, which includes:

- Reallocating A&CP from non-working media and asset production to consumer engagement behind core brands (CoverGirl U.S., Rimmel U.K.)

- Streamlining the FY27 innovation pipeline for tighter, better-supported launches

- Doubling down on procurement savings

- Refining brand equities for clearer differentiation

Early green shoots: CoverGirl's Simply Ageless and Lash Blast franchises improved from high-single-digit declines to low/mid-single-digit declines in the past 3 months. Rimmel similarly narrowed its gap to the category.

AI Initiatives Accelerating

Coty is scaling AI across operations through partnerships with Microsoft, ServiceNow, and now OpenAI:

- 70-90% reduction in post-production asset costs for selected fragrance, cosmetics, and skincare brands through generative AI

- Preparing for "machine buying" via Generative Engine Optimization to influence how brands appear in AI recommendations

- Company-wide training and workshops to embed AI into daily operations

Key Management Quotes

Markus Strobel, Executive Chairman and Interim CEO:

"Coty has accomplished a lot in the last 5 years... Growing prestige fragrance business at 10% CAGR from fiscal 2021 to fiscal 2025 is no small feat. The company grew gross margins by close to 500 basis points and leveraged the company by over 4 turns in that time. These are major accomplishments."

"But as they say, 'If you're so smart, why aren't you rich?' There is no denying that Coty's financial results in the past 18 months have been disappointing."

"Without adequate support, our top initiatives don't reach their full potential in the markets that matter most... A disproportionate amount of our spending gets tied up in asset creation, and not enough flows into working media and consumer engagement."

"I'm confident that things at Coty will get better. It won't happen overnight, but it will happen."

"We recognize that our recent financial performance has not met expectations. There's no sugarcoating it. This leadership transition marks a fresh chapter grounded in realism, discipline and focus... Consumer demand is our North Star."

Balance Sheet Improvement

One genuine positive: the Wella sale and strong free cash flow significantly strengthened the balance sheet:

At 2.7x leverage, Coty is at a 9-year low. This provides financial flexibility for the turnaround.

Q&A Highlights

The earnings Q&A session revealed several additional strategic insights:

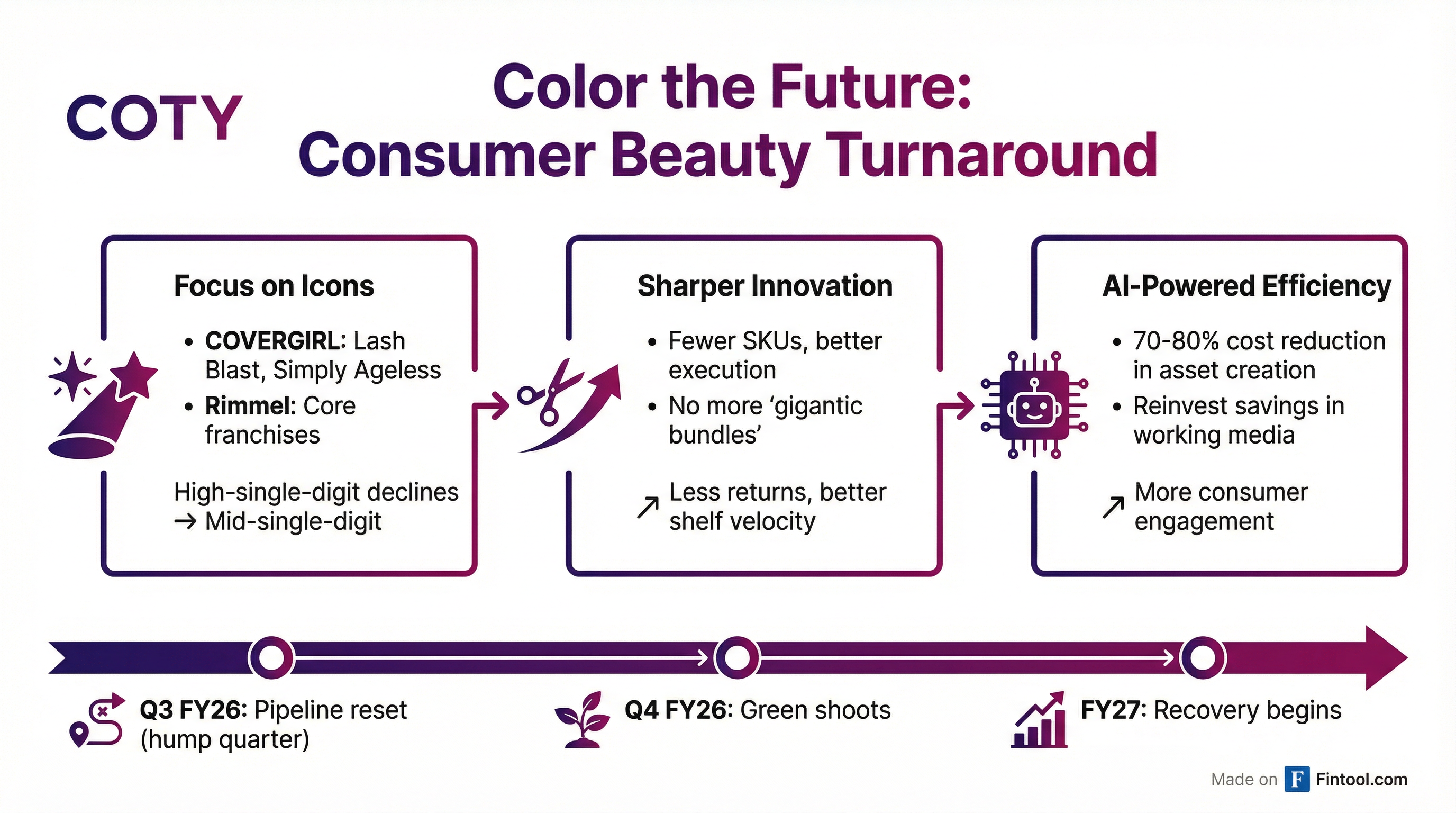

Consumer Beauty Turnaround — "Less Is More"

When pressed on the Consumer Beauty recovery timeline, Strobel outlined a three-part fix:

-

Focus on iconic assets — Concentrate on COVERGIRL's Lash Blast, Simply Ageless, and Rimmel. Early results encouraging: franchises improved from high-single-digit declines to mid-single-digit declines.

-

Sharper innovation bundles — Past bundles were "gigantic" with too many SKUs, leading to returns and crowded-out productive shelf space. The new FY26 bundle is tighter with better SKU velocity.

-

AI-powered efficiency — Experiments show 70-80% cost reduction in asset creation using generative AI, freeing up money for working media and consumer-facing investments.

"In the past, we had gigantic innovation bundles with lots of SKUs, most of them didn't work, and they crowded out productive SKUs on the shelf. So you got kind of the double whammy, and you got returns from the trade."

Gucci License Exit Strategy

The Gucci license ends in June 2028. Management outlined three actions to compensate:

On Kering: Strobel noted the company is "always open for deals that create value" — signaling openness to early termination discussions.

Channel Strategy Evolution

In response to questions about drugstore weakness and Amazon growth:

"We are investing heavily in online. We're investing heavily in e-commerce. We're investing in TikTok shops and everywhere where consumers go. But... brands like COVERGIRL and Sally Hansen, there's a huge Gen X population that shops for them."

Gross Margin Breakdown

The 200-300 bps margin compression was dissected by segment:

Prestige:

- High promotionality in late Q2 — "very high promotionality in the market" with aggressive discounting

- Tariffs: ~$8M impact in Q2, <$40M expected for full year

- FX: EUR/USD headwind from European production

Consumer Beauty:

- Fixed cost under-absorption from lower color cosmetics volumes

- Geographic mix: Brazil growing well, but high-margin U.S. brands underperforming

Operational Discipline Gaps

The new CEO identified a key cultural issue:

"We have a very, very creative organization... What we are missing a bit is the operational discipline to bring this to market in a way that is sequenced, that is properly funded, and that is well thought through."

The shift: Sell-out, not sell-in. Focus on consumer offtake and market share rather than retailer pipeline. Management is investing in a unified data lake and AI to establish "one source of truth" for performance metrics.

What to Watch Going Forward

-

Strategic Update by End of FY26 — Strobel committed to sharing "an initial, more detailed view of our strategy, our focus brands and markets, and our portfolio" by fiscal year-end

-

Consumer Beauty Strategic Review — Continuing under Gordon von Bretten's leadership; Color the Future plan execution will take "one or two years"

-

Q3 Execution — Can they hit the lowered $100-110M EBITDA target? Gross margins expected down 200-300 bps again

-

Prestige Market Share — U.S., U.K., and Germany remain key battlegrounds; need to close sellout gap

-

Promotional Normalization — Holiday discounting was intense; unclear if this is the new normal or a temporary dislocation

Pipeline Catalysts

Upcoming launches:

- Calvin Klein female fragrance (launching in "coming weeks")

- Marc Jacobs Beauty makeup debut (mid-CY26) — "excited to launch makeup under Marc Jacobs Beauty"

- Continued BOSS Bottled Beyond support with co-merchandising and halo strategy

- Cosmic Kylie Jenner Intense rollout continuing

The Bottom Line

Coty delivered an "in-line" quarter that was anything but. The headline numbers masked a 370 bps EBITDA margin decline, and the guidance withdrawal signals management doesn't have visibility into the path forward. New CEO Strobel's candid assessment that "financial performance has been disappointing" is refreshing but doesn't change the fundamental challenges: a struggling Consumer Beauty business, an intensely promotional fragrance market, and margin compression that shows no signs of abating.

The 18% stock decline is severe but arguably warranted — investors are pricing in considerable uncertainty. At 2.7x leverage and with a new strategic framework, Coty has the balance sheet to weather the storm. The question is whether "Coty. Curated." is a real turnaround plan or just rebranding of the same challenges.

Related Coverage: