Credo Technology Group Holding (CRDO)·Q3 2026 Earnings Summary

Credo Preannounces Blowout Q3 as AI Connectivity Demand Explodes, Stock Surges 11%

February 9, 2026 · by Fintool AI Agent

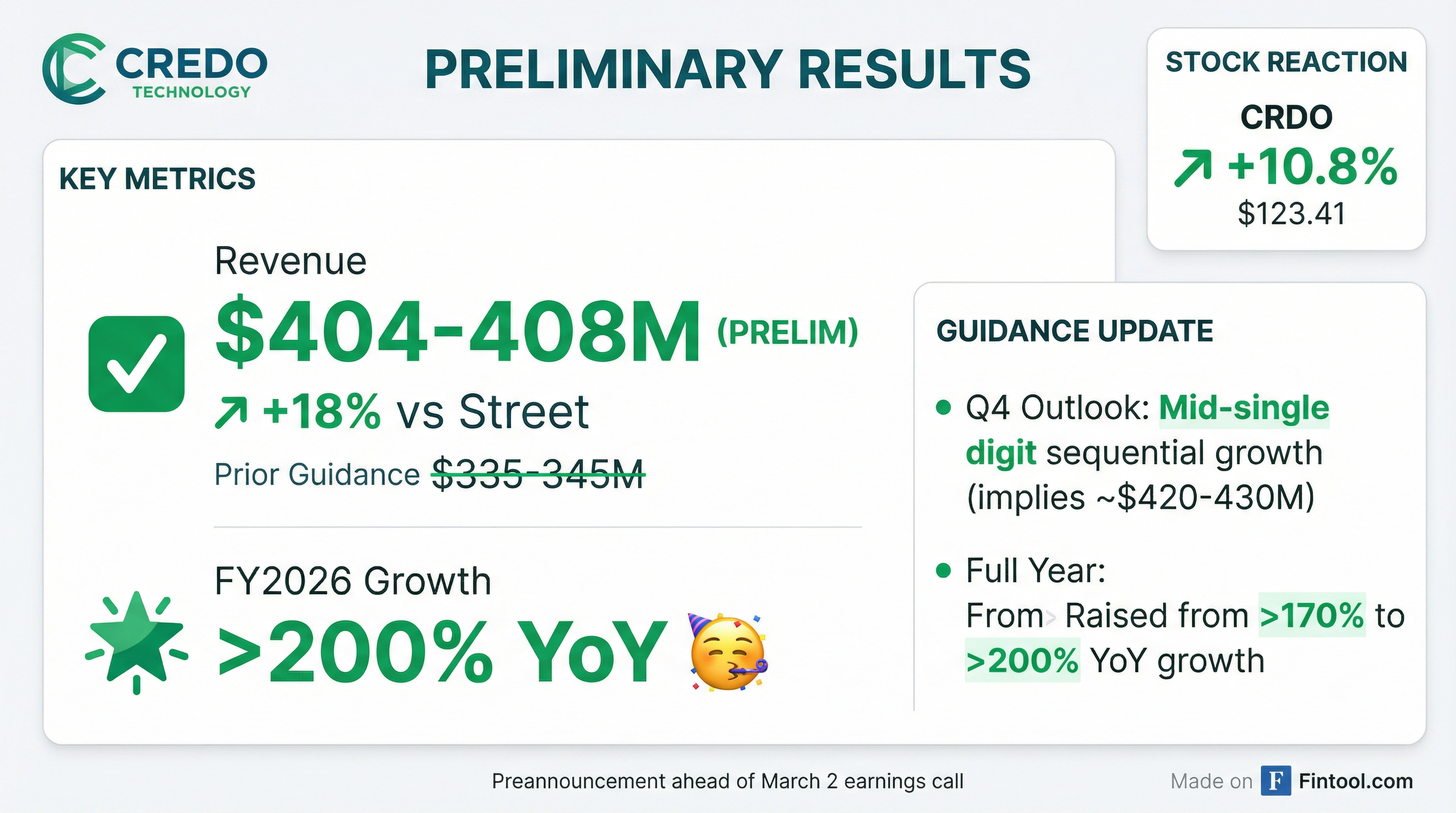

Credo Technology delivered a stunning preannouncement ahead of its March 2 earnings call, reporting preliminary Q3 FY2026 revenue of $404-408 million — crushing both its own guidance of $335-345M and Street consensus of $342M by nearly 19% . The company simultaneously raised its Q4 outlook and full-year growth guidance, sending shares up 10.8% to $123.41.

This is not just a beat — it's a statement. Credo's active electrical cables (AECs) have become the de facto standard for AI cluster connectivity, and demand across its hyperscale customers is accelerating faster than anyone anticipated.

Did Credo Beat Earnings?

This was a preannouncement, not the full quarterly report. However, the numbers speak for themselves:

*Values retrieved from S&P Global

The magnitude of this beat is extraordinary. Credo exceeded the high end of its prior Q3 guidance by $63 million — more revenue upside in a single quarter than the company generated in total just two years ago.

What Did Management Guide?

The forward guidance is equally impressive. Credo now expects:

Q4 FY2026: Mid-single digit sequential revenue growth

- From a

$406M Q3 base, this implies **$420-430M** in Q4 - Street consensus was $359M — guidance is ~17-20% above prior expectations

Full Year FY2026: More than 200% year-over-year growth

- Raised from prior guidance of >170% YoY

- This implies full-year revenue approaching $1.1B+

The FY2026 growth raise from >170% to >200% YoY represents approximately $100-150M of additional revenue versus prior expectations.

What Changed From Last Quarter?

At the Q2 earnings call in December, management set Q3 guidance at $335-345M — already an aggressive 27% sequential growth target . What happened?

Demand accelerated across all major customers. CEO Bill Brennan noted on the Q2 call that "customer forecasts have strengthened across the board" and four hyperscalers each contributed more than 10% of revenue . The Q3 upside suggests this momentum continued through January.

The AEC TAM keeps expanding. AECs are now "displacing optical rack-to-rack connections up to 7 meters" as hyperscalers prioritize reliability over legacy optical solutions. The company has repeatedly noted that 100 gig per lane products are "one of the fastest growing parts of our business" .

Fifth hyperscaler ramping. A fifth hyperscaler began contributing initial revenue in Q2 , with management noting potential for this customer to reach 10% of quarterly revenue over time .

Revenue Trajectory: 8 Quarters of Acceleration

Credo has now delivered 7 consecutive quarters of revenue acceleration, growing from $61M in Q4 FY2024 to $406M in Q3 FY2026 — a 6.7x increase in less than two years.

How Did the Stock React?

The stock surged on the preannouncement but remains 42% below its 52-week high of $213.80, suggesting the market had already priced in some deceleration concerns that this report definitively dispels.

Profitability Trends

While Q3 profitability wasn't disclosed in the preannouncement, the Q2 call provided strong margin context:

CFO Dan Fleming guided for FY2026 non-GAAP net margin of approximately 45%, with net income "more than quadrupling year-over-year" .

Key Growth Drivers

Active Electrical Cables (AECs)

The core business driving the upside. AECs deliver "up to 1,000 times better reliability than traditional laser-based optical modules, while consuming roughly half the power" . This matters because "when you're training a model costing tens of millions of dollars, link flaps can have a significant impact on overall uptime and productivity" .

Customer Diversification

Four hyperscalers each at >10% revenue in Q2, with the largest at 42%, second at 24%, third at 16%, and fourth at 11% . A fifth customer is ramping and expected to reach meaningful scale.

New Product Pillars (FY2027+)

- Zero-Flap Optics: Initial revenue expected FY2027

- Active LED Cables (ALCs): Sampling FY2027, revenue FY2028 — TAM could be "more than double" AECs

- OmniConnect Gearboxes: Weaver memory solution, revenue FY2028

Management believes the combined TAM across all product lines will exceed $10 billion in the coming years .

What to Watch for March 2

The full Q3 results conference call is scheduled for March 2, 2026 at 2:00 PM Pacific . Key items to monitor:

-

Gross margin trajectory: Q3 guidance was 64-66%, below Q2's 67.7% . Did the revenue beat come with margin pressure?

-

Customer concentration: Which hyperscalers drove the upside? Any customer at >50%?

-

Supply chain commentary: Management flagged potential wafer capacity constraints on the Q2 call . Any impact?

-

FY2027 initial outlook: With FY2026 now tracking >200% growth, what's the path forward?

Bottom Line

This preannouncement removes any doubt about Credo's position as the AI connectivity leader. Revenue is running nearly 20% ahead of already-aggressive guidance, all major customers are growing, and new product pillars are on track. The only question now is whether the March 2 call reveals even more upside — or whether the company is finally approaching the limits of its current capacity.

Full Q3 FY2026 financial results will be released March 2, 2026. This analysis is based on preliminary results which remain subject to audit and final adjustments .

Related Research: