Day One Biopharmaceuticals (DAWN)·Q4 2025 Earnings Summary

Day One Crushes Q4 as OJEMDA Revenue Surges 82% QoQ, Stock Jumps 5%

February 24, 2026 · by Fintool AI Agent

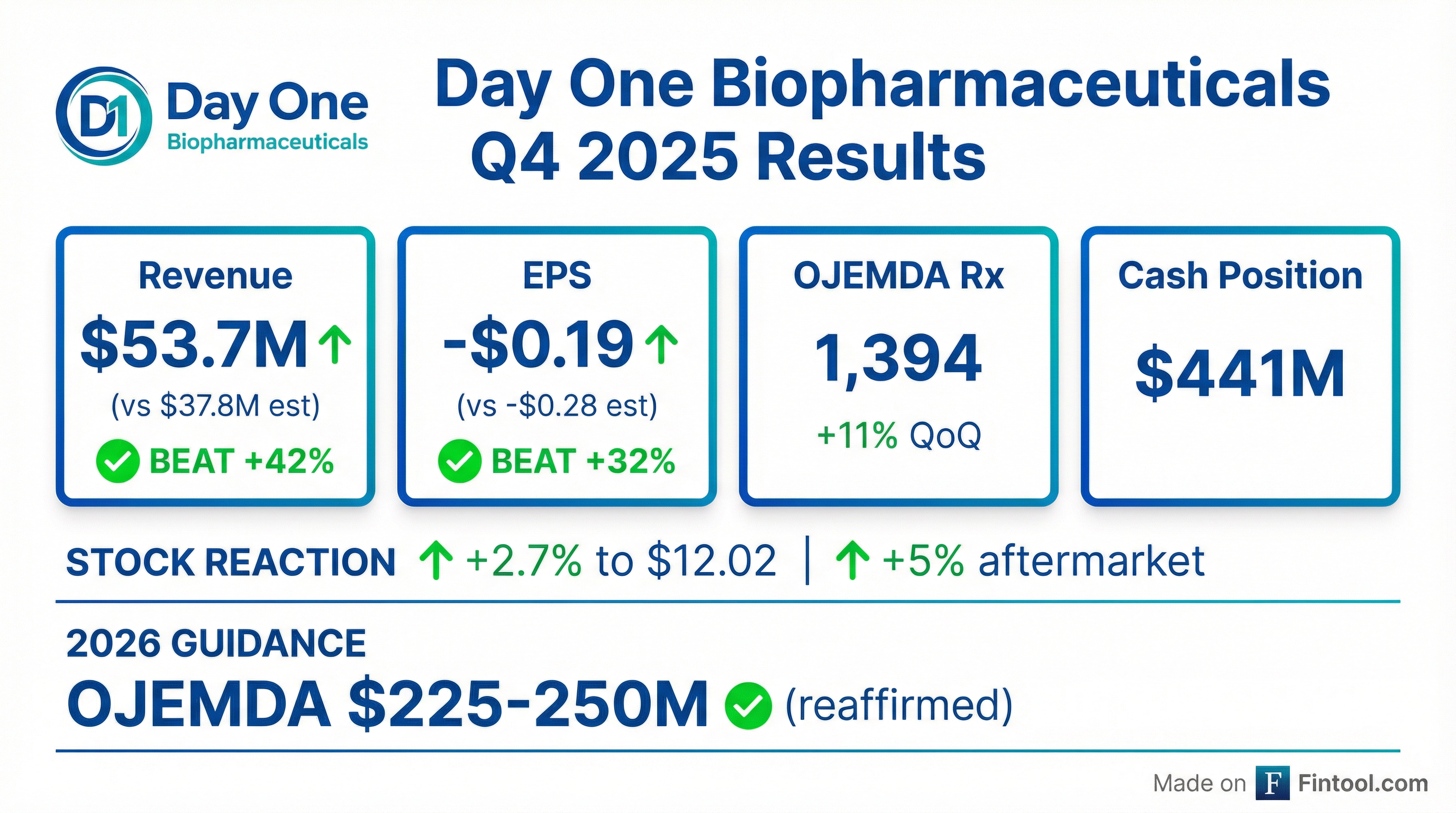

Day One Biopharmaceuticals (NASDAQ: DAWN) delivered a blowout Q4 2025, with OJEMDA net product revenue of $52.8M crushing expectations and full-year product revenue hitting $155.4M (+172% YoY). The commercial-stage biotech beat both revenue and EPS estimates by wide margins, reaffirmed strong 2026 guidance of $225-250M, and announced key pipeline catalysts for the coming year. Shares rose 2.7% during regular trading and added another 2.3% aftermarket to $12.30.

Did Day One Beat Earnings?

Day One delivered a decisive double beat, exceeding analyst expectations across all key metrics:

The revenue beat was driven by accelerating OJEMDA adoption in relapsed/refractory pediatric low-grade glioma (pLGG). Q4 prescriptions reached 1,394 (+11% QoQ), bringing full-year 2025 prescriptions to 4,635—a remarkable 181% increase versus the partial 2024 launch year.

Historical Revenue Performance:

How Did the Stock React?

DAWN shares responded positively to the earnings beat, rising 2.7% to close at $12.02 on elevated volume of ~2M shares. The stock added another 2.3% in aftermarket trading to reach $12.30.

Stock Performance Context:

- 52-week range: $5.64 – $13.20

- Current price: $12.02 (near 52-week high)

- 50-day average: $10.35

- 200-day average: $7.99

- YTD performance: Stock has doubled from 2025 lows

The positive stock reaction reflects confidence in Day One's commercial execution and reaffirmed 2026 guidance.

What Did Management Guide?

Day One reaffirmed its 2026 OJEMDA net product revenue guidance of $225-250 million, representing >50% growth at the midpoint versus 2025's $155.4M.

CEO Jeremy Bender highlighted the transformational year:

"2025 was a seminal year for Day One, marked by significant achievements across every pillar of our organization. By maintaining our strong commercial execution, leveraging our expertise to extend into additional rare cancers, and steadily advancing our early-stage pipeline, we are delivering on our mission to bring new medicines to people of all ages with life-threatening diseases."

Forward Estimates (Consensus):

*Values retrieved from S&P Global

The implied FY 2026 consensus revenue of ~$246M sits near the high end of management's $225-250M guidance range.

What Changed From Last Quarter?

Several significant developments occurred since Q3 2025:

1. Mersana Therapeutics Acquisition (January 2026) Day One completed its acquisition of Mersana Therapeutics, adding Emi-Le (emiltatug ledadotin), a B7-H4-targeted ADC in Phase 1 for adenoid cystic carcinoma (ACC). This represents a potential >$300M revenue opportunity and extends Day One's rare cancer focus.

2. FIREFLY-1 Three-Year Data Updated 3-year follow-up data from the pivotal FIREFLY-1 trial reinforced OJEMDA's durability:

- Median duration of response: 19.4 months

- Median time to next treatment: 42.6 months

- Overall response rate: 53%

- No new safety signals observed

3. Accelerating Commercial Traction Q4 marked Day One's 6th consecutive quarter of double-digit sequential growth since OJEMDA's April 2024 launch. Compound quarterly growth rate has averaged ~36% for revenue and ~34% for prescriptions.

Financial Health and Balance Sheet

Day One ended 2025 with a strong balance sheet:

Operating Expenses (FY 2025 vs FY 2024):

- R&D: $148.1M vs $227.7M (-35%) — lower after FIREFLY-1 completion

- SG&A: $120.6M vs $115.5M (+4%) — modest increase supporting commercial expansion

The significant R&D reduction reflects the transition from clinical development to commercial execution, with the pivotal FIREFLY-1 trial mature and FIREFLY-2 enrollment progressing.

Pipeline Catalysts to Watch

Day One outlined several key 2026 milestones:

Market Opportunity Expansion:

- Current r/r pLGG market: ~$400M+ opportunity

- Frontline pLGG (FIREFLY-2): Doubles addressable market to ~$500M+

- Emi-Le in ACC: Additional $300M+ opportunity

- Total U.S. revenue opportunity: $1B+ across three indications

Key Risks and Concerns

1. Cash Consumption: Despite improving losses, Day One still consumed ~$90M of cash in 2025. Continued execution is critical to reaching profitability.

2. Concentrated Revenue: OJEMDA represents essentially 100% of product revenue. Any competitive or regulatory setbacks would significantly impact the business.

3. FIREFLY-2 Execution: The frontline pLGG trial is the largest growth driver. Enrollment delays or negative data would materially impact the thesis.

4. Pipeline Risk: Both Emi-Le and DAY301 are early-stage programs acquired through M&A. Clinical or regulatory failure would limit the diversification story.

Bottom Line

Day One delivered an exceptional Q4 2025, with OJEMDA revenue crushing estimates by 42% and demonstrating the strongest sequential growth since launch. The reaffirmed $225-250M 2026 guidance, combined with pipeline catalysts across FIREFLY-2, Emi-Le, and DAY301, positions the company for continued momentum. With $441M in cash and narrowing losses, Day One has the runway to execute on its ambitious rare cancer pipeline while the commercial business scales toward profitability.

Related: Day One Company Page | Q4 2025 Earnings Call Transcript | Q3 2025 Earnings Recap