DIVERSIFIED HEALTHCARE TRUST (DHC)·Q4 2025 Earnings Summary

DHC Caps Blockbuster 2025 as Top-Performing REIT with 112.6% Return

February 24, 2026 · by Fintool AI Agent

Diversified Healthcare Trust (DHC) closed out a transformational 2025 with Q4 results that reinforced the turnaround story. The senior living-focused REIT delivered same property SHOP NOI of $38.3M (+27.6% YoY), completed the transition of 116 AlerisLife communities to new operators, and used $250M in property sale proceeds to eliminate its 2026 debt maturities . DHC has now sold 64 properties for gross proceeds of $1.1 billion since 2023 , with capital recycling supporting deleveraging and portfolio quality improvement.

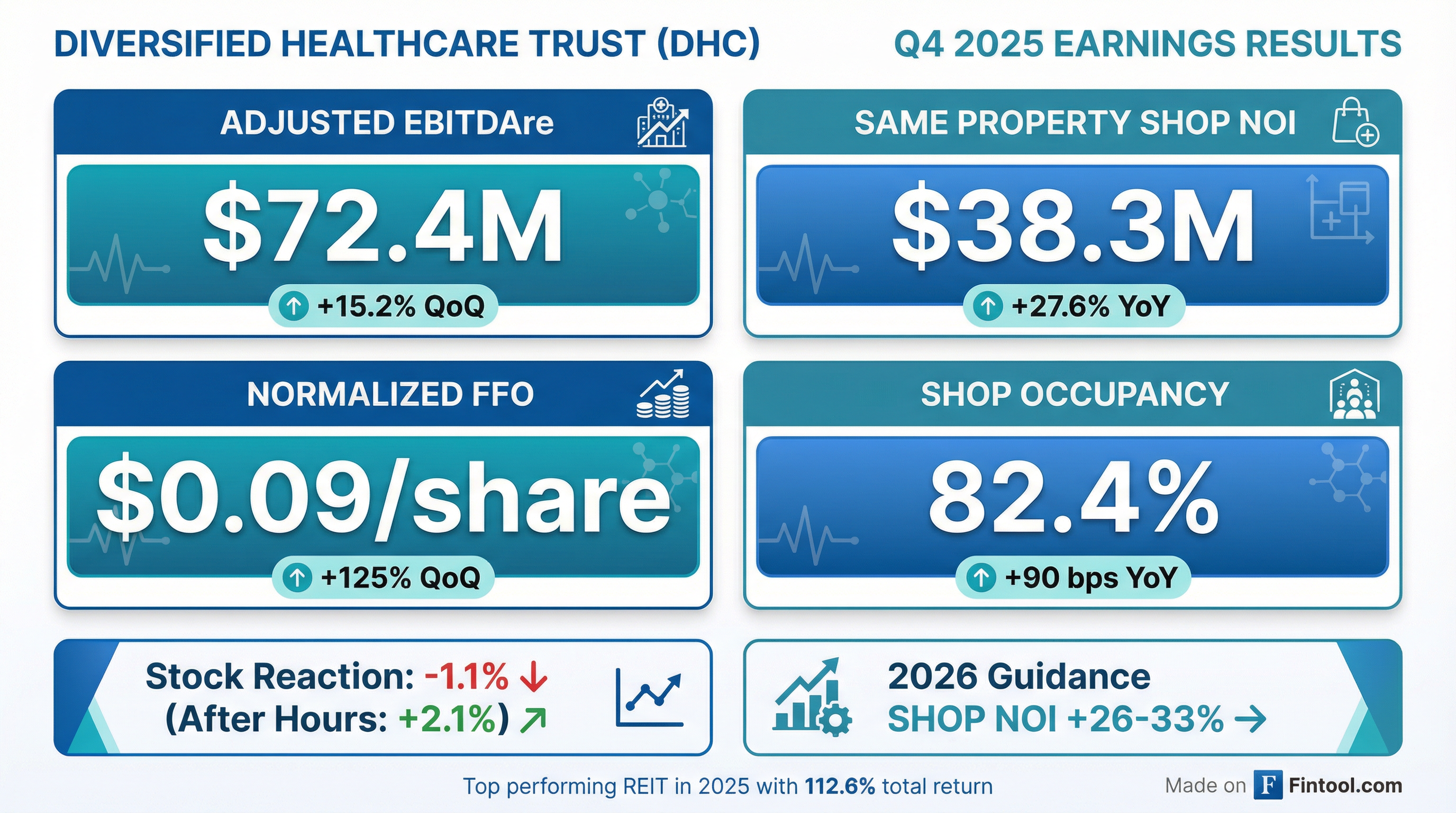

Did DHC Beat Earnings?

DHC delivered Q4 2025 results at the high end of management's expectations :

The sequential improvement in Normalized FFO from $0.04 to $0.09/share was driven by the elimination of discount accretion expense on the zero-coupon notes that were repaid in December .

What Drove the SHOP Segment Performance?

The Senior Housing Operating Portfolio (SHOP) segment—which represents 70% of DHC's real estate assets—continued its strong recovery :

Full year 2025 same property SHOP NOI improved 31.3% to $139.3M , validating the operator transition strategy.

Mark-to-Market Opportunity

DHC's SHOP portfolio has significant upside to industry benchmarks :

This gap represents substantial embedded growth potential as the newly transitioned operators stabilize operations.

Demographic Tailwinds Supporting the Thesis

DHC highlighted powerful industry fundamentals in their investor presentation :

Supply-Demand Imbalance:

- 80+ population projected to grow at 4.1% CAGR over the next 15 years

- Senior housing inventory growth expected to remain depressed at only 0.6%

- 4Q25 showed record occupancy of 89.4% for senior housing in Primary and Secondary NIC markets

- 80+ population expected to grow 55% by 2035

Demographic Inflection Point:

- Oldest baby boomers begin turning 80 in 2026, driving a surge in senior housing demand

- Decline in traditional caregiving population (55-70 years old) expected during the same period

- Limited new construction benefits existing communities and in-place portfolios

Rent Growth:

- Top primary/secondary markets seeing rent growth of up to 10% annually

Operator Transition Occupancy Upside

DHC completed the transition of 116 communities to seven new operators. Each has meaningful occupancy upside to their respective market benchmarks :

The transition strategy focuses on :

- Implementing dynamic pricing structures and expanding ancillary services

- Leveraging regional densification to reduce structural labor costs

- Driving savings through centralized purchasing

- Capturing uplift from recently renovated communities (60%+ renovated in last 3 years)

What Did Management Guide for 2026?

DHC provided aggressive 2026 guidance that implies continued acceleration :

Guidance assumptions include :

- Same property SHOP occupancy growth of ~300 bps YoY

- Revenue growth of ~8.0% with rate growth of ~5.3%

- Operating expense growth of ~5.7%

- No acquisitions assumed

- 13 properties under contract expected to close in 1Q26 for ~$100M

Capital Recycling Strategy

DHC has executed aggressively on capital recycling :

2025 Capital Raises :

- Credit Facility: 40%

- Senior Notes: 17%

- Mortgage Financings: 43%

Recent financings reflect SHOP valuations of approximately $185,000 per unit, driven by operational improvements and favorable market dynamics .

Balance Sheet Transformation

DHC achieved significant deleveraging in 2025 :

Post-Quarter Cash Infusion: DHC received a $27.2M cash distribution from AlerisLife in connection with the wind down of its business .

Credit Upgrades: Moody's and S&P Global upgraded DHC to Caa1 and B-, respectively .

Target: DHC is targeting leverage of 6.5x to 7.5x to further enhance cost of capital and improve rating agency outlook .

Debt Maturity Schedule

DHC has no debt maturities until 2028 after fully redeeming the 2026 zero coupon notes in December :

What Did Analysts Ask? (Q&A Highlights)

Wings Reopening Strategy

Management disclosed a high-ROI initiative to reopen closed skilled nursing wings within existing communities :

The strategy enables a "continuation of care" by introducing memory care to communities currently offering only IL and AL. Management noted this provides "rising tide lifts all boats" benefits through shared costs and rate uplift at existing acuity levels .

4Q Margin Improvement Drivers

Q4 margin improvement was driven by a combination of transition noise dissipating and operators right-sizing cost structures. Management characterized the Q4 run rate as "a pretty small impact... nothing really material" from remaining transition costs .

January/February Trends

Management confirmed January results are "in line with expectations" and consistent with guidance :

- Rate escalators: 4%-6% range, with outsized push early in the year on legacy AlerisLife properties

- Flu season impact: "Nothing outside... nothing outsized relative to the portfolio"

- Operator integration: Still ongoing as some operators transitioned as late as year-end 2025

2026 NOI Cadence

The 300 bps occupancy growth in guidance is measured on a full-year average basis (2025 vs. 2026), not quarter-end to quarter-end . Growth drivers have different timing:

- Rate increases: Weighted toward beginning of year (legacy AlerisLife push)

- Occupancy growth: Backloaded to Q2/Q3 (selling season)

- Levels of care revenue: Takes time as operators integrate

- Expense savings: Starts immediately (regional staffing benefits), with incremental gains mid-year

Management expects close to 200 basis points of margin improvement on a same-store basis in 2026 .

MOB/Life Science Lease Expirations

Two primary vacates are known for 2026 :

Dividend Policy

When asked about dividend implications given the momentum in 2026 guidance, CEO Chris Pilato indicated the board will consider it but there are "no immediate priorities on addressing the dividend right now" as the focus remains on operations .

How Did the Stock React?

DHC released earnings after market close on February 23, 2026. The stock traded lower on February 24, the first full trading day following results:

The pullback reflects profit-taking after DHC was the top-performing REIT in the United States in 2025 , driven by successful operator transitions, balance sheet improvement, and SHOP NOI recovery.

Medical Office & Life Science Portfolio

DHC's non-SHOP segments provide stable cash flow :

Medical Office Portfolio

Life Science Portfolio

Triple Net Leased Segment

Key Management Quotes

"In 2025, we completed over $1.4 billion in capital markets activity, principally focused on financings, asset sales, and the establishment of a $150 million undrawn credit facility... These efforts resulted in full year consolidated NOI growth of 31.3%, a reduction in our leverage of over three turns and no debt maturities until 2028."

— Christopher Bilotto, President and CEO

"Despite what we believe to be a really strong outlook for 2026, I think collectively speaking, we believe we're still trailing kind of the benchmark and occupancy, even at kind of the guidance occupancy provided. We know just based on kind of margins and where the portfolio will end up for 2026, that there's outsized potential to grow margins."

— Matt Brown, CFO

"We are intensely focused on executing in lockstep with our operators, combining disciplined operational oversight with their deep regional expertise to deliver measurable gains in occupancy and portfolio NOI."

— Christopher Bilotto, President and CEO

What Are the Key Risks?

Medical Office Headwinds: The Medical Office and Life Science segment faces occupancy pressure and asset sales reduced NOI contribution. 2026 guidance implies a -9% to -13% decline in MOB/LS NOI .

Execution Risk: The 2026 guidance implies aggressive SHOP NOI growth of 26-33%. Any operational missteps with the newly transitioned operators could impact results.

Interest Rate Sensitivity: 5.7% of debt is variable rate , though this is well-managed with interest rate caps and the company has extension options on its floating rate debt.

Credit Rating: Despite upgrades, DHC remains below investment grade (B-/Caa1), which limits financing flexibility and increases borrowing costs.

Portfolio Composition

As of December 31, 2025, DHC's $6.3 billion portfolio includes :

Forward Catalysts

- Q1 2026 earnings — First full quarter under new operator structure

- March 2026 — Expected close of 13 property sales for ~$23M gross proceeds

- Wings Reopening Initiative — ~500 unit potential at mid-teens ROI over next several years

- Interest Coverage Target — Management expects year-end 2026 coverage at or above 2.0x (vs. 1.5x currently)

- 2028 — First significant debt maturity ($640.7M secured)

- Ongoing — Occupancy convergence toward 89%+ NIC market benchmarks

ESG & Governance Highlights

DHC emphasizes sustainability and governance :

- Board Composition: 43% women, 71% independent, 29% underrepresented communities

- Green Certifications: 18 LEED properties, 9 BOMA 360 properties, 24 ENERGY STAR properties

- Green Lease Leaders: Gold certification

About the Manager

DHC is externally managed by The RMR Group LLC :

- AUM: Over $37 billion

- Real Estate Professionals: Nearly 900

- Properties Managed: ~1,800

- Fee Structure: Base fee tied to lower of historical cost or market cap (aligns with shareholders)

Data sourced from DHC Q4 2025 8-K filing (February 23, 2026), Q4 2025 Earnings Call Transcript (February 24, 2026), and Q4 2025 Investor Presentation (February 24, 2026). Stock data from market data providers. Values retrieved from S&P Global where noted.