DOVER (DOV)·Q4 2025 Earnings Summary

Dover Q4 2025: Double Beat Extends Streak to 9 Quarters, Guidance In-Line

January 29, 2026 · by Fintool AI Agent

Dover Corporation (NYSE: DOV) delivered a double beat in Q4 2025, reporting adjusted EPS of $2.51 (vs. $2.48 consensus) and revenue of $2.10 billion (vs. $2.07 billion consensus). The quarter marked the strongest organic growth of the year at +5%, driven by robust demand across the company's secular growth-exposed markets. Shares traded down ~0.6% on the day as investors digested guidance that came in roughly in-line with expectations.

Did Dover Beat Earnings?

Yes—Dover extended its earnings beat streak to nine consecutive quarters.

Sources:

For the full year 2025, Dover generated $8.09 billion in revenue (+4% YoY, +2% organic) and adjusted EPS of $9.61 (+16% YoY). GAAP EPS of $7.97 was down 21% year-over-year, but this reflects the prior-year gain on the De-Sta-Co disposition rather than operational weakness.

What Did Management Guide?

Dover's 2026 guidance came in essentially in-line with consensus:

Source:

The midpoint of adjusted EPS guidance ($10.55) implies 10% growth from FY 2025's $9.61, reflecting volume leverage, acquisitions, and restructuring savings.

CEO Richard Tobin struck a confident tone: "We have a constructive outlook for 2026. Demand trends are solid and broad-based across the portfolio, and are supported by our order book, with no individual end market presenting a material headwind."

On the earnings call, Tobin emphasized balance sheet flexibility: "Our dry powder in 2026 remains almost identical to the starting position from the previous year, as we have self-funded our CapEx, M&A, and share repurchases in 2025. We are in an advantageous position, and I would expect that we will be active in 2026."

What Changed From Last Quarter?

Several notable shifts emerged in Q4:

1. Organic growth accelerated. Q4's +5% organic growth was the highest of 2025, up from +0.5% in Q3 and +0.9% in Q2. Management attributed this to improving conditions in retail fueling and refrigerated door cases.

2. Bookings momentum strengthened. Q4 bookings of $2.14 billion were up 10% YoY, with a book-to-bill ratio above 1.0. Climate & Sustainability Technologies saw particularly strong booking activity (+24% YoY) as refrigeration markets recover.

3. Accelerated share repurchase initiated. Dover launched a $500 million ASR program in November, initially receiving 2.3 million shares. The program is expected to complete in Q2 2026.

4. Restructuring benefits quantified. Management specified ~$40 million of carryover profit from prior-period productivity actions in 2026. Clean Energy & Fueling sees the largest impact, though benefits are back-end weighted as rooftop consolidations complete.

5. Secular growth markets outperforming. The ~20% of the portfolio exposed to secular growth markets (AI, clean energy, biopharma) continues to grow double-digits and is expected to sustain that trajectory into 2026.

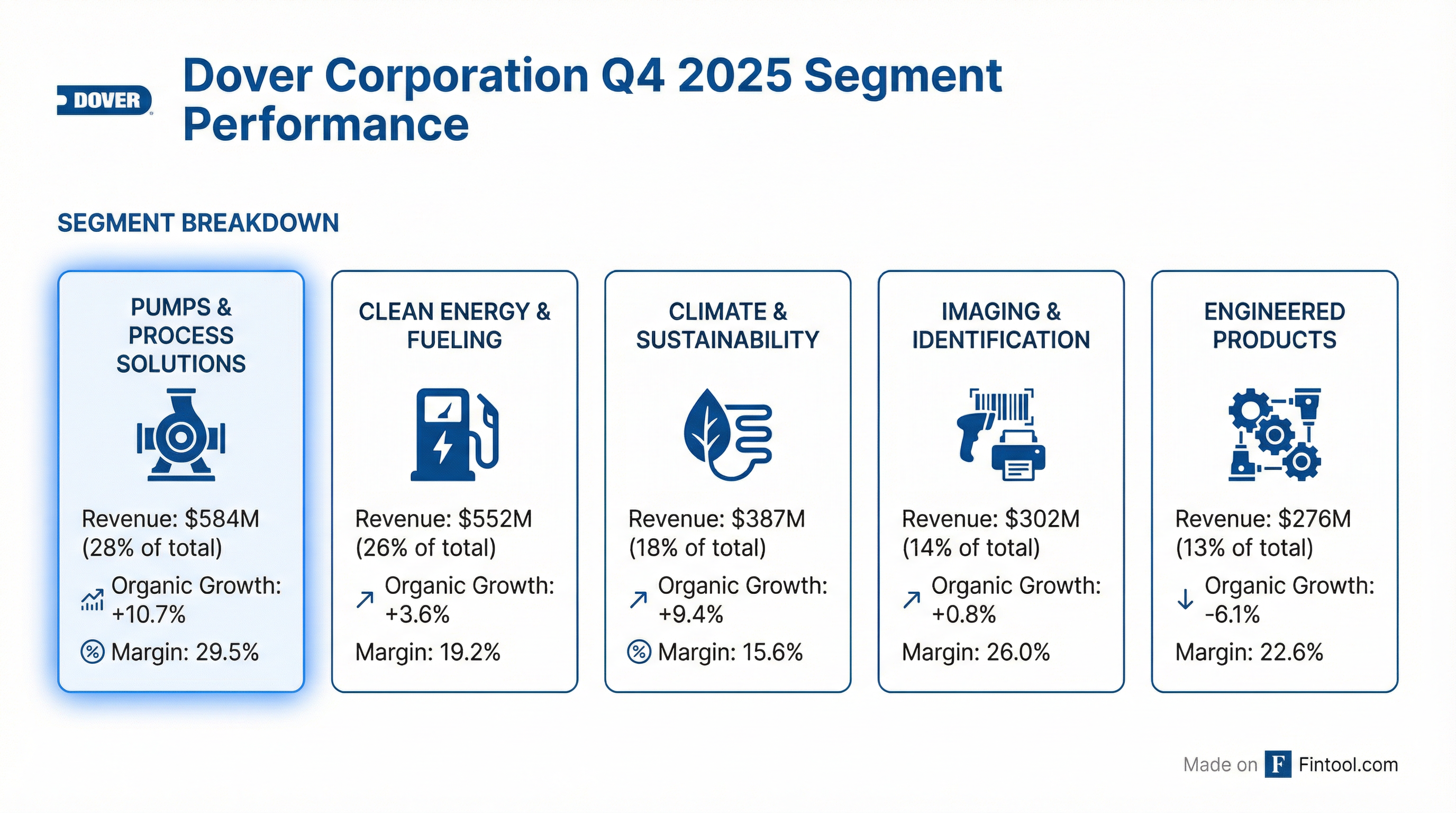

How Did Each Segment Perform?

Source:

Pumps & Process Solutions was the standout, delivering +10.7% organic growth on strong demand in single-use biopharma, AI/energy infrastructure, and notably the first quarterly growth in polymer processing since Q1 2024. This segment now represents 28% of revenue and carries the highest margin profile at 32%.

Climate & Sustainability Technologies rebounded sharply (+9.4% organic) after several quarters of negative growth, driven by solid shipment and order rates in refrigerated door cases, CO2 systems, and record shipments in North American heat exchangers. Margin expanded 250 bps YoY on volume leverage, operational execution, and positive mix from CO2 systems.

Engineered Products continued to face headwinds (-6.1% organic), impacted by weaker industrial vehicle markets and the prior-year De-Sta-Co divestiture anniversary.

2026 Segment Outlook

Management provided segment-level organic growth expectations for 2026:

Climate & Sustainability Technologies is expected to lead growth in 2026, a notable reversal after being a drag for much of 2025. The segment posted a book-to-bill of 1.21 in Q4, with management noting record quarterly heat exchanger shipments in the U.S. tied to data center liquid cooling.

Pumps & Process Solutions faces near-term headwinds in polymer processing equipment (Maag), though management noted: "Maag's orders are so high in dollar value, you'll know when it's coming... right now, the European chemical market is not doing well." The biopharma business had a tough comp in Q1 due to heavy restocking in early 2025, but the Q4 exit run rate should hold for 2026.

How Did the Stock React?

Dover shares traded down ~0.6% to $206 following the release, despite the double beat. The muted reaction likely reflects:

- Guidance in-line, not raised. Investors may have hoped for a guidance raise given the strong Q4 momentum.

- High expectations already priced in. DOV entered earnings up 44% over the trailing 12 months, trading at 19.6x forward P/E.

- Mixed segment performance. Engineered Products weakness offset strength elsewhere.

Capital Allocation Update

Dover's balance sheet remains flexible for continued M&A and shareholder returns:

Source:

The company completed four acquisitions in 2025 for total consideration of $665 million, focused on the Pumps & Process Solutions and Clean Energy & Fueling segments. These deals are reportedly "performing above their deal models."

Net debt to net capitalization rose to 18.2% from 13.5% a year ago, reflecting acquisition activity and share repurchases.

Q&A Highlights

Key themes from the analyst Q&A:

Price/Cost & Tariffs: Management expects 1.5-2% price embedded in 2026 guidance, with 1-1.5% price over cost. On tariff exposure, CEO Tobin noted: "We're cognizant about input costs moving up, and if we have to take pricing action, that will actually drive some top-line growth also." Climate & Sustainability is most commodity-exposed, particularly copper.

Restructuring Benefits: Dover expects ~$40 million of carryover profit from prior-period productivity actions in 2026. Clean Energy & Fueling will see the biggest impact, though benefits are back-end loaded as rooftop consolidations complete. Refrigeration will carry extra fixed costs in H1 as one facility closes and another is built.

Seasonality Warning: Management repeatedly cautioned on Q1 expectations: "Consensus for the year was oddly high for Q1, despite the fact that we've been saying over and over again, be careful about the biopharma mix in Q1." Expect normal seasonality with Q1 as a production month, ramping into peak delivery in Q2-Q3.

Refrigeration Recovery: "We're sold out for Q1. We're booking well into Q2. So far, so good." Management confirmed the refrigeration business is recovering strongly, with short-cycle order visibility supporting the outlook.

Retail Fueling Cycle: Tobin highlighted a new CapEx cycle in North American retail fueling: "Since 2001-ish, EVs were taking over the world, so there was not a lot of CapEx spent in retail fueling... that's kind of turned the corner here. Spreads at the retail are as high as they've ever been. That's going to drive returns on projects."

M&A Appetite: On transformational deals: "We have a very keen eye about execution risk... If we were to consider something transformational, it would have to be shareholder-friendly to Dover. We're not required to do anything." Bolt-on acquisitions remain the focus, with a "very interesting" pipeline dominated by proprietary opportunities.

Through-Cycle Growth: Management pegged entitlement growth at 3-6% depending on GDP, noting the portfolio "can clearly do 5%."

Clean Energy Margin Path: The segment should reach low 20s margins in 2026, walking up to the 25% target over time as restructuring benefits flow through and volume leverage improves.

Guidance Assumptions & Drivers

What Should Investors Watch?

Near-term catalysts:

- ASR program completion (Q2 2026)

- Continued refrigeration market recovery (sold out through Q1)

- Restructuring benefits realization (H2-weighted)

- North Carolina greenfield facility progress

Key risks flagged by management:

- Tariff and trade policy uncertainty—management noted learning from 2025 tumult

- Copper and commodity cost inflation, particularly in Climate & Sustainability

- Biopharma tough comp in Q1 from heavy restocking in early 2025

- European weakness in Vehicle Service Group (year 3 of downturn)

- Maag/polymer processing dependent on European chemical market recovery

Areas of strength:

- Secular growth markets (20% of portfolio) growing double-digits and expected to continue

- AI/energy infrastructure demand robust (thermal connectors, precision components)

- Natural gas power generation exposure across large turbines, midstream, and reciprocating compressors

- Backlog supports confidence: Q4 book-to-bill 1.02, Climate & Sustainability 1.21

Data sources: Dover Corporation 8-K filed January 29, 2026; Dover Q4 2025 Earnings Call Transcript; S&P Global Market Intelligence; Zacks Investment Research; StreetInsider.