Earnings summaries and quarterly performance for Elanco Animal Health.

Executive leadership at Elanco Animal Health.

Jeffrey Simmons

Chief Executive Officer

David Kinard

Executive Vice President, Human Resources, Corporate Communications and Administration

Ellen de Brabander

Executive Vice President, Innovation and Regulatory Affairs

Grace McArdle

Executive Vice President, Manufacturing and Quality

James Meer

Senior Vice President, Chief Accounting Officer

José Manuel Correia de Simas

Executive Vice President, U.S. Farm Animal Business

Rajeev Modi

Executive Vice President, U.S. Pet Health and Global Digital Transformation

Ramiro Cabral

Executive Vice President and President, Elanco International

Robert VanHimbergen

Chief Financial Officer

Shiv O'Neill

Executive Vice President, General Counsel and Corporate Secretary

Timothy Bettington

Executive Vice President, Corporate Strategy and Market Development

Board of directors at Elanco Animal Health.

Art Garcia

Director

Deborah Kochevar

Director

Denise Scots-Knight

Director

Kapila Anand

Director

Kirk McDonald

Director

Lawrence Kurzius

Chairman of the Board

Michael Harrington

Director

Paul Herendeen

Director

R. David Hoover

Director

Stacey Ma

Director

Research analysts who have asked questions during Elanco Animal Health earnings calls.

Michael Ryskin

Bank of America Merrill Lynch

8 questions for ELAN

Brandon Vazquez

William Blair & Company, L.L.C.

6 questions for ELAN

Daniel Clark

Leerink Partners

6 questions for ELAN

Erin Wright

Morgan Stanley

6 questions for ELAN

Jonathan Block

Stifel Financial Corp.

6 questions for ELAN

Navann Ty

BNP Paribas S.A.

5 questions for ELAN

Umer Raffat

Evercore ISI

4 questions for ELAN

Andrea Zayco Narvaez Alfonso

UBS

3 questions for ELAN

Michael DiFiore

Evercore ISI

3 questions for ELAN

Andrea Alfonso

UBS

2 questions for ELAN

Andrew Dusing

Cleveland Research

2 questions for ELAN

Balaji Prasad

Barclays

2 questions for ELAN

Chris Schott

JPMorgan Chase & Company

2 questions for ELAN

Christopher Schott

JPMorgan Chase & Co.

2 questions for ELAN

David Westenberg

Piper Sandler

2 questions for ELAN

Ekaterina Pirogova

JPMorgan Chase & Co.

2 questions for ELAN

Jon Block

Stifel, Nicolaus & Company, Incorporated

2 questions for ELAN

Linda Bolduc

Morgan Stanley

2 questions for ELAN

Navann Ty Dietschi

BNP Paribas

2 questions for ELAN

Ekaterina Knyazkova

Cantor Fitzgerald

1 question for ELAN

Mike Curry

Evercore ISI

1 question for ELAN

Ross Sparenblek

William Blair & Company

1 question for ELAN

Recent press releases and 8-K filings for ELAN.

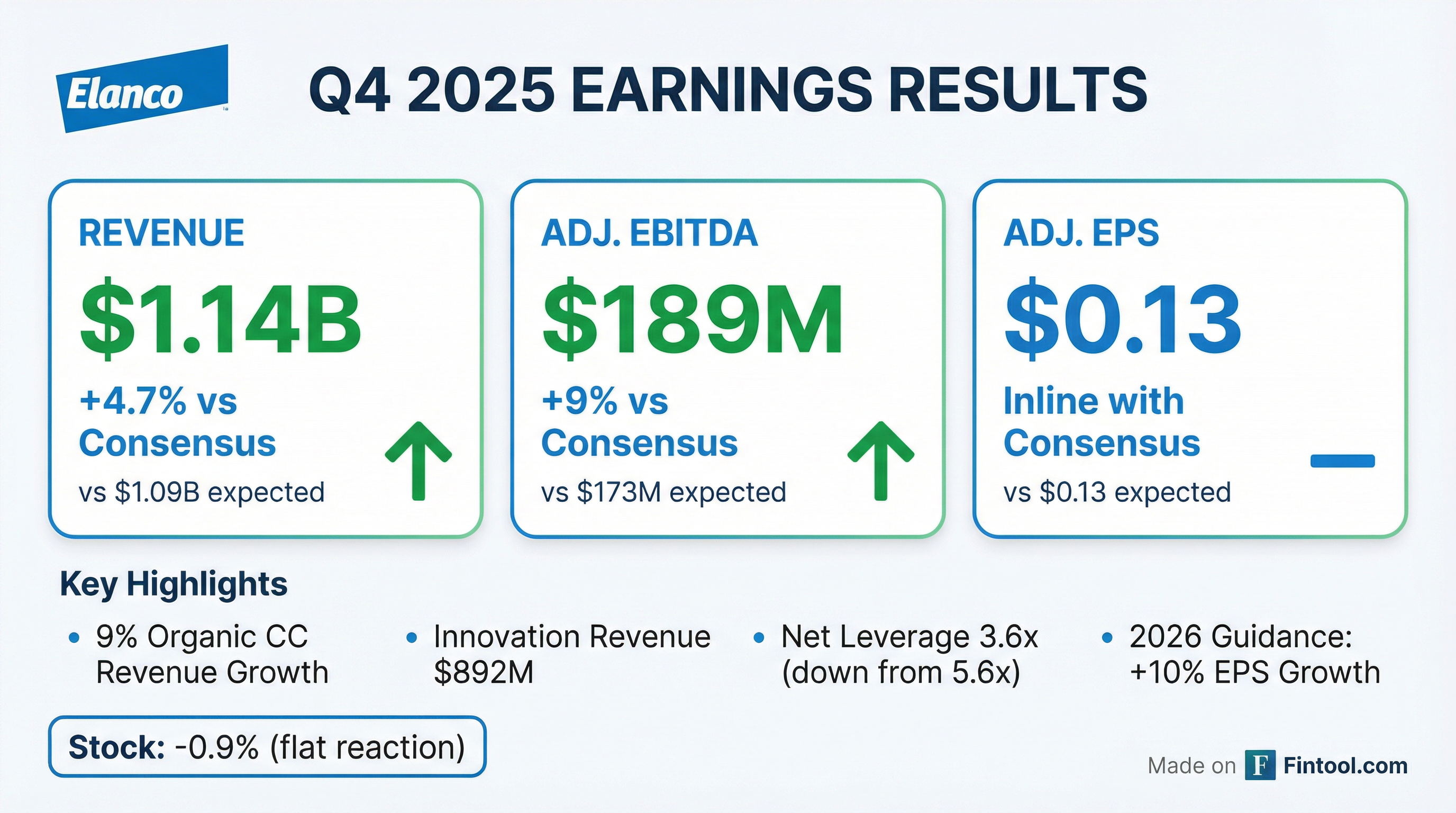

- Elanco reported strong Q4 2025 performance, exceeding guidance across revenue, earnings, EPS, and cash flow. The company's innovation basket generated $892 million in revenue in 2025, surpassing guidance, and is projected to reach $1.15 billion in 2026.

- The company reiterated its 2026 guidance for mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth.

- Elanco expects to achieve leverage in the low 3s by the end of 2026 and below 3 in 2027, with a long-term target of 2-2.5x. This deleveraging will open up optionality for shareholder returns.

- The Elanco Ascend program is projected to deliver $200 million to $250 million of EBIT improvement, net of inflation and investment. This includes $25 million in restructuring savings in 2026, increasing to a full run rate benefit of $60 million in 2027.

- Key product updates include Experior reaching $200 million in sales in 2025 with 80% growth , and Zenrelia showing strong momentum with an updated label and presence in over 50% of U.S. clinics. Befrena is set for a two-stage launch in 2026.

- Elanco reported a strong Q4 performance, exceeding guidance on revenue, earnings, EPS, and cash flow, with its innovation basket revenue reaching $892 million.

- The company raised its 2026 innovation basket revenue expectation to $1.15 billion and reiterated its 2026 guidance for mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth.

- Key growth drivers include expanding market penetration for Credelio Quattro and Zenrelia, with Zenrelia now in over 50% of U.S. clinics and adding 600-700 new clinics monthly. The two-stage launch of Befrena in 2026 is also a significant upcoming event.

- The Elanco Ascend program is projected to yield $200-$250 million in EBIT improvement, including $25 million in restructuring savings for 2026, with a full run rate of $60 million starting 2027.

- Elanco anticipates reducing leverage to the low 3s in 2026 and below 3 in 2027, which will provide flexibility for shareholder returns.

- Elanco reported strong Q4 performance, exceeding guidance for revenue, earnings, and EPS, and achieved better-than-anticipated deleveraging. The company's innovation basket generated $892 million in revenue, surpassing guidance, with 2026 expectations for this basket raised to $1.15 billion.

- Elanco reaffirmed its 2026 guidance, projecting mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth. Leverage is expected to reach the low 3s in 2026 and below 3 in 2027.

- The Elanco Ascend program is anticipated to deliver $200 million-$250 million in EBIT improvement, complemented by $25 million in restructuring savings in 2026, growing to a $60 million full run rate in 2027.

- Key product updates include Experior's annual revenue exceeding $200 million with 80% growth in 2025, and Zenrelia's increased penetration to over 50% of US clinics after a label update in October 2025.

- Elanco reported a strong Q4 2025, beating guidance across revenue, earnings, and cash flow, with 9% organic growth overall, 10% in U.S. Pet Health, and 17% in U.S. Farm, and reduced its debt leverage to 3.6 times.

- The company issued strong initial fiscal 2026 guidance, projecting mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth, with a goal to delever below 3x by 2027.

- Growth is significantly fueled by its innovation basket, which grew by $400 million in 2025 and is expected to add another $250 million in 2026, with the total basket guide increased to $1.15 billion.

- Pricing is expected to accelerate in 2026, building on 2% price and 5% volume growth in 2025, contributing to anticipated margin expansion alongside fixed cost leverage and the Elanco Ascend program targeting $200-$250 million net EBITDA improvement by 2030.

- Elanco reported a strong Q4 2025, exceeding guidance across revenue, earnings, and cash flow, with 9% organic growth driven by 10% in U.S. Pet Health and 17% in U.S. farm business.

- The company issued robust fiscal 2026 guidance, forecasting mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS, in line with its Investor Day algorithm.

- Innovation is a key growth driver, with the innovation basket's 2026 guide increased to $1.15 billion, having grown $400 million in 2025 and projected to grow another $250 million in 2026, contributing higher margins than the corporate average.

- Elanco is focused on debt reduction, achieving 3.6x leverage in 2025 and targeting below 3x in 2027, while also implementing the Elanco Ascend program for $200-$250 million net EBITDA improvement by 2030.

- Elanco reported a strong Q4 2025, exceeding guidance for revenue, earnings, and cash flow, with 9% organic growth overall, 10% in U.S. Pet Health, and 17% in U.S. Farm, and deleveraging to 3.6 times.

- The company issued strong initial fiscal 2026 guidance, forecasting mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth, with a target to delever below 3 times in 2027.

- Elanco's innovation basket is a significant growth driver, with its 2026 guide increased to $1.15 billion, having grown $400 million in 2025 and projected to grow another $250 million in 2026. These products contribute higher margins than the corporate average.

- Key product successes include Credelio Quattro, which is expanding U.S. clinic penetration by approximately 500 clinics monthly, and Zenrelia, which has achieved significant international market shares (e.g., 40% in Brazil, 30% in Japan) and is accelerating in the U.S..

- The Elanco Ascend initiative is expected to generate $200-$250 million of net EBITDA improvement by 2030, with $25 million in savings anticipated in 2026 from restructuring efforts.

- Elanco reported 9% growth in Q4 2025, with innovation revenue reaching $892 million in 2025, and provided 2026 guidance for mid-single-digit top-line growth, high-single-digit EBITDA growth, and low-double-digit EPS growth.

- The company increased its 2026 revenue expectation from its basket of innovation to $1.15 billion, up from $1.1 billion, highlighting the strong performance of products like Quattro, which achieved blockbuster status in 8 months.

- Elanco is in active discussions with the FDA for Zenrelia label enhancements, noting its use in 40 countries with a clean label and by over 1 million dogs worldwide.

- Strategic initiatives include Elanco Ascend, expected to deliver $200 million-$250 million in EBITDA improvement by 2030, with 75% from gross margin and 25% from OpEx, and leveraging AI for cost savings and R&D.

- The company plans to reduce leverage to the low 3s by end of 2026 and below 3x in 2027, with a long-term target of 2.0 to 2.5x, which is expected to enable future shareholder returns.

- Elanco reported 9% growth in Q4 2025, with its innovation basket generating $892 million in revenue for the year, and ended 2025 with leverage at 3.6 times.

- For 2026, the company projects mid-single-digit top line growth, high-single-digit EBITDA growth, and low-double-digit EPS growth, aiming to reduce leverage to the low 3s. The innovation basket revenue target for 2026 was raised to $1.15 billion.

- Key products like Credelio Quattro achieved blockbuster status in 8 months, the fastest for an Elanco pet health product, while Zenrelia shows reorder rates north of 80% in approximately half of US vet clinics. The company expects limited impact from generic competition on its Seresto brand, whose US patent extends through Q3 2027.

- The Elanco Ascend program is anticipated to contribute $200 million-$250 million of EBITDA improvement by 2030, with 75% from gross margin and 25% from OpEx. The company targets a long-term leverage of 2.0 to 2.5x, expecting to achieve below 3x in 2027.

- Elanco reported 9% growth in Q4 2025, with its innovation basket contributing $892 million in revenue for the year, and ended 2025 with leverage at 3.6 times.

- For 2026, the company provided guidance for mid-single-digit top-line growth, high-single-digit EBITDA growth, and low-double-digit EPS growth, with plans to reduce leverage to the low 3s.

- The innovation basket, featuring products like Quattro and Zenrelia, is now projected to generate $1.15 billion in revenue for 2026, an increase from previous expectations, and carries a higher margin profile.

- Elanco's Seresto brand, with sales split 50% US and 50% OUS, has US patent protection until Q3 2027, and the company anticipates limited generic impact, which is factored into its 2026 guidance.

- The Elanco Ascend program is expected to deliver $200 million-$250 million in EBITDA improvement by 2030, with 75% of savings from gross margin and 25% from OpEx.

- Elanco reported above-expectation Q4 2025 results for adjusted EBITDA, revenue, and EPS. The company provided initial fiscal 2026 guidance in line with Investor Day targets, projecting mid-single-digit top-line growth, high single-digit EBITDA growth, and low double-digit EPS growth, with an expectation to delever to the low threes by year-end 2026.

- The company highlighted strong performance from its innovation basket, including Zenrelia which is exceeding international launch expectations with 40% market share in Brazil and 30% in Japan, and Credelio Quatro which achieved $358 million in revenue in 2025. A Q2 2026 phased launch is planned for Befrena.

- Elanco anticipates price acceleration in 2026 from the 2% seen in 2025, driven by new product launches and a strategy to price for value based on efficacy.

- The company expects EBITDA margins to improve 200 to 350 basis points by 2028, supported by the Elanco Ascend program, which is projected to generate $200 million-$250 million of net EBITDA improvement over five years, with 75% from gross margin and 25% from OpEx.

Quarterly earnings call transcripts for Elanco Animal Health.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more